Australian dollar smashed to 10 year lows as WHO declares pandemic

DXY softened last night as EUR bounced:

The Australiand ollar was poleaxed back to 10 years lows:

But EMs were even weaker:

Gold was mixed:

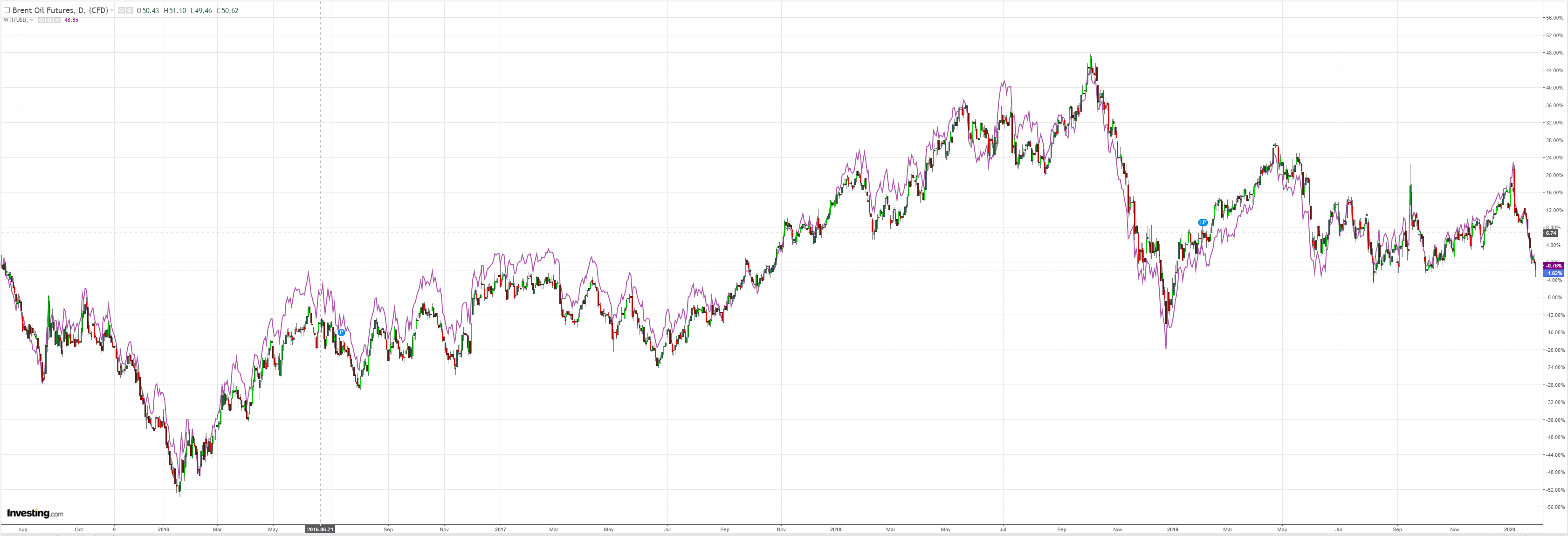

Oil down:

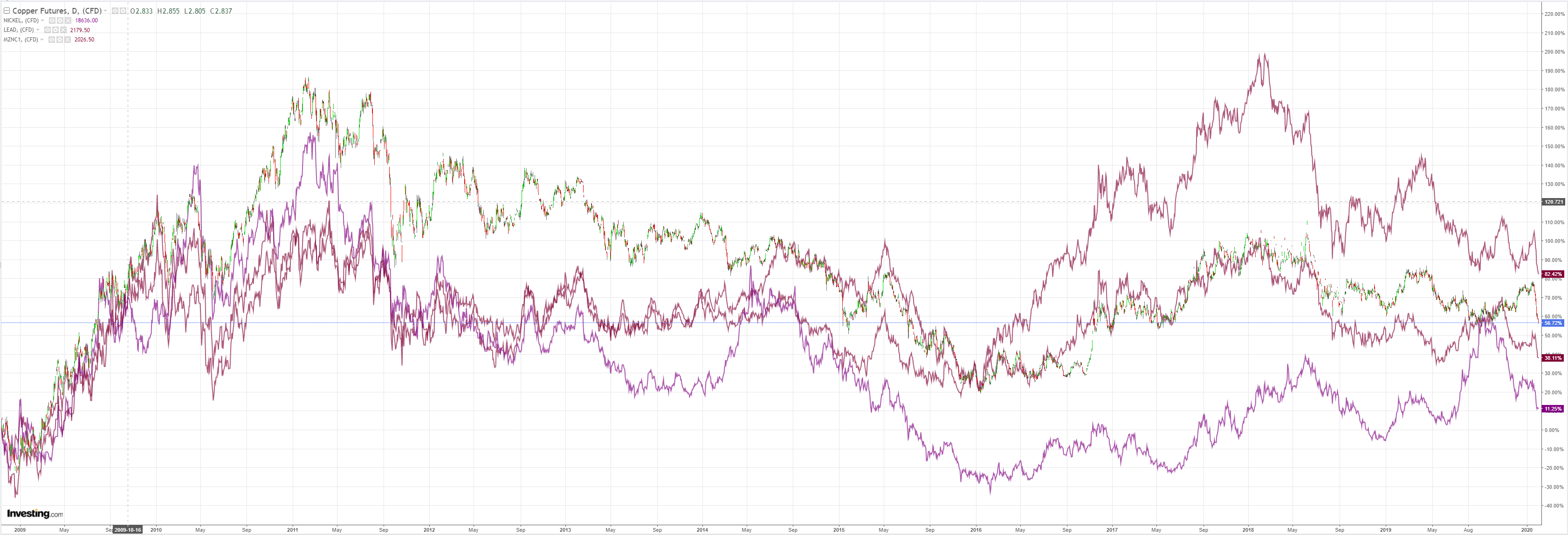

Metals are in all sorts:

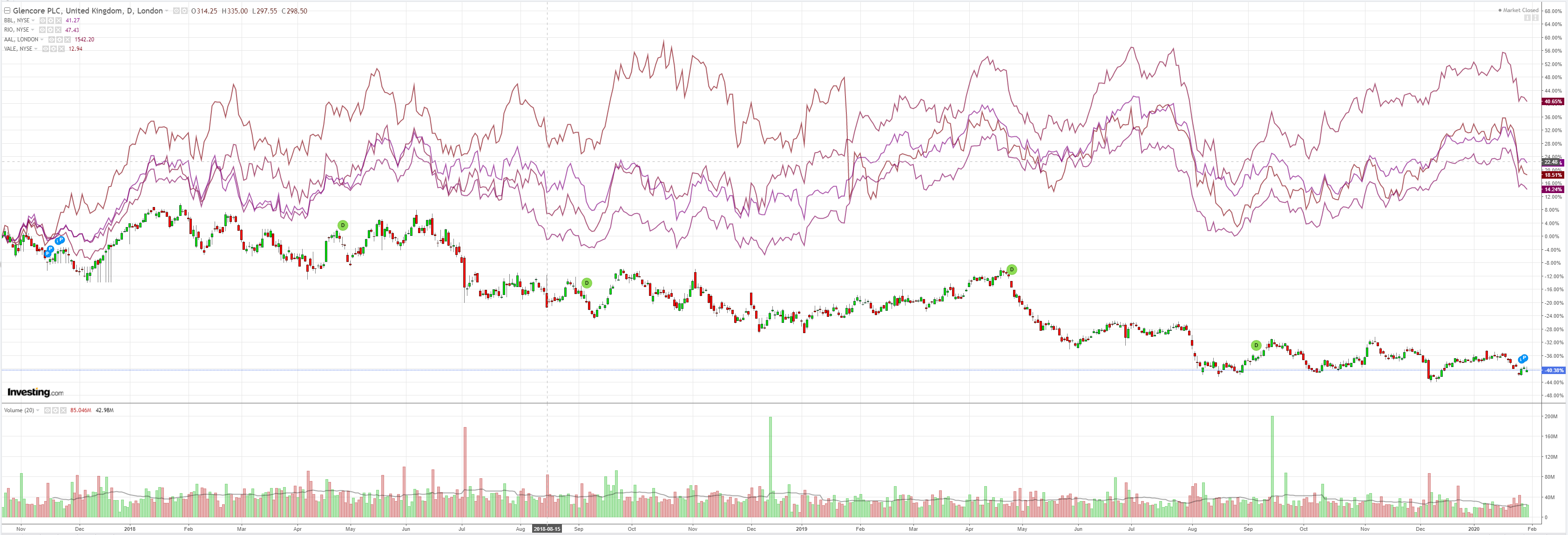

Miners rolled lower:

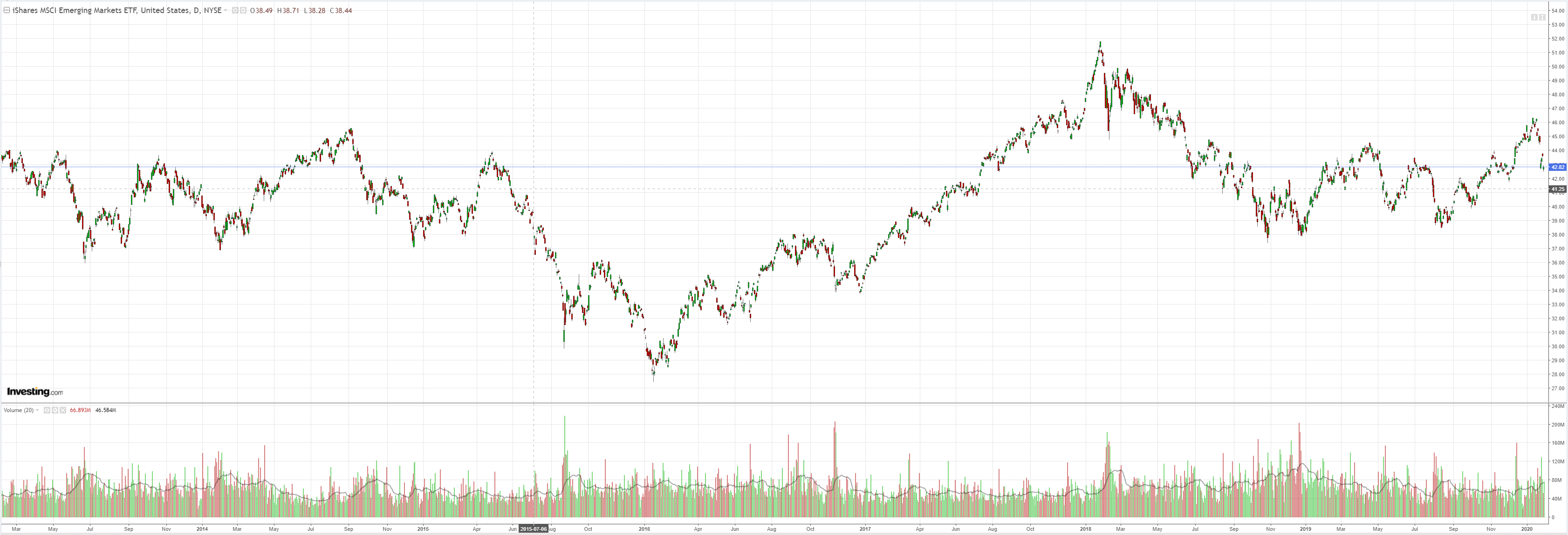

EM stocks did OK:

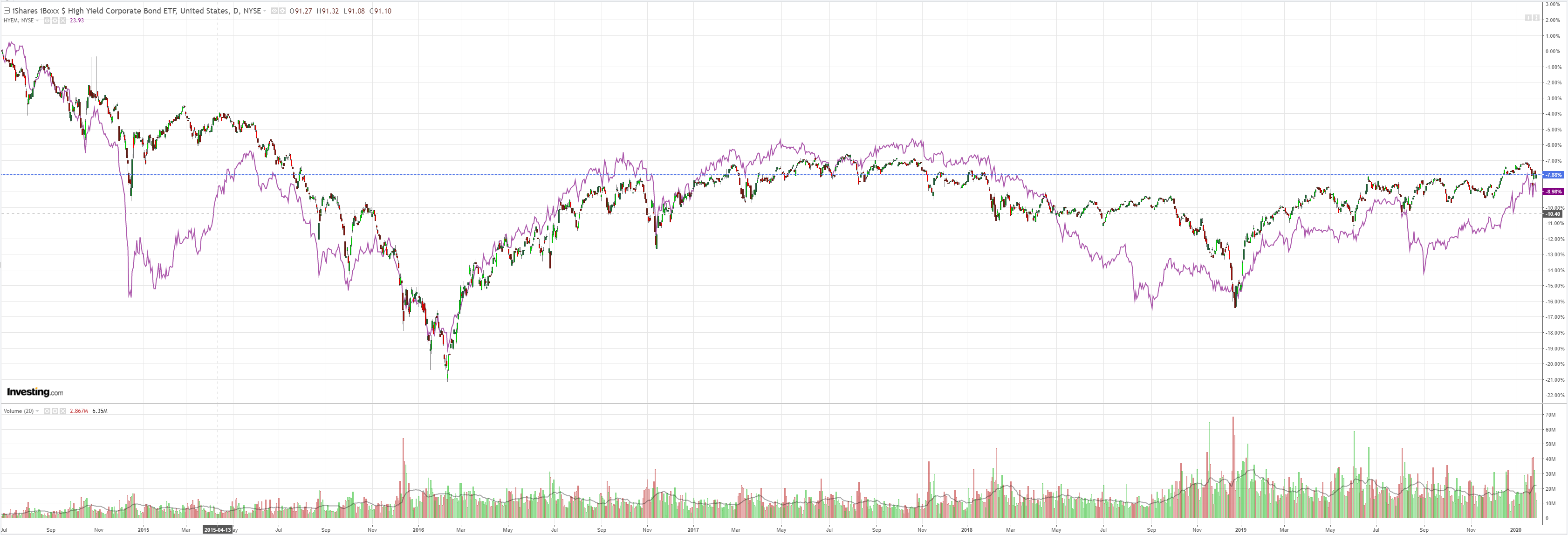

Junk fell:

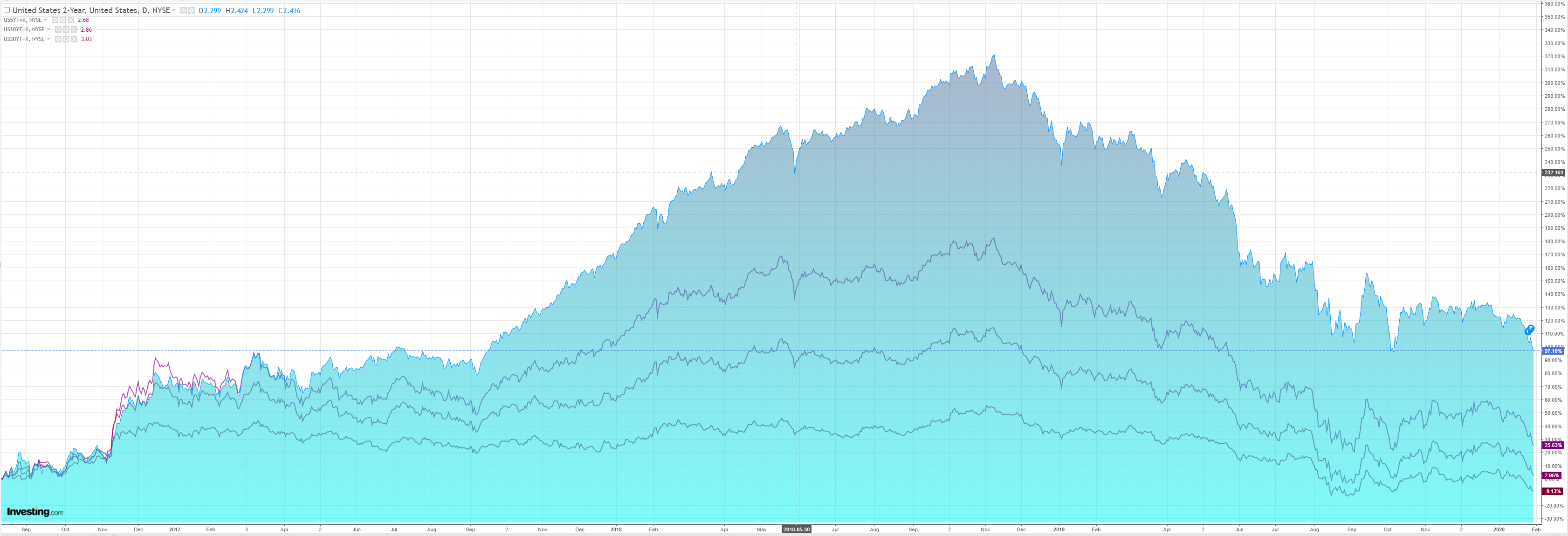

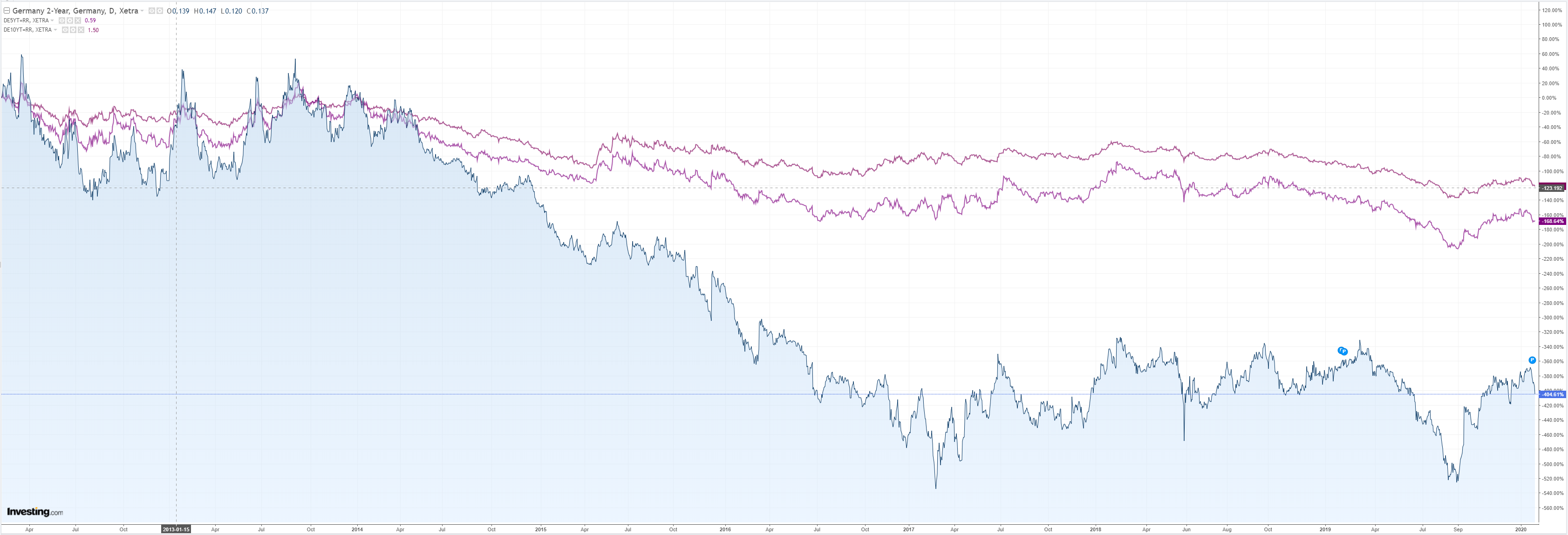

Bonds are booming:

Stocks were deranged but are down a little as a I write:

Westpac has the data wrap:

Event Wrap

US 4Q GDP rose 2.1% annualised (vs. est. 2.0%), but personal consumption disappointed (1.8%, est. 2.0%) as did low core PCE of 1.3% (est. 1.6%, prior 2.1%).

BoE voted 7-2 to keep policy on hold, against market expectations of a 50% chance of a cut.

There was debate over whether rebounds in expectations and intentions would be realised as well as how expansionary the coming Budget (11th March) would be. Any potential easing would be on the proviso that these would not develop. The tone of the statement, MPR and Press conference (the last for Carney) was not as dovish than markets had expected.German Jan. CPI of 1.7%y/y met expectations, although the Harmonised version disappointed at 1.6%y/y (est. +1.7%y/y).

Eurozone Dec. unemployment dipped to 7.4% (est. unchanged at 7.5%), edging closer to the pre-crisis lows of 7.3% in early 2008. German unemployment fell -2k (est. +5k) but remained unchanged at 5.0% (as est.).

EC Eurozone Jan. business and consumer confidence were mixed but broadly in line with estimates. Economic confidence lifted to 102.8 (est. 101.8, prior 101.3) but service confidence stuttered at 11.0 (prior 11.3) and consumer confidence remained at its initial release of -8.1.

Event Outlook

Australian private credit is expected to remain soft in December at 0.2%. Business investment weakened materially in 2019 given patchy investment and as confidence fell away. New lending for housing is rebounding, but is being partly offset by existing borrower pre-payment.

NZ consumer confidence (ANZ) rose for a third consecutive month in December, January expected to see a continuation.

China PMIs for January are likely to point to a continued stabilisation of growth. The impact of coronavirus will be closely assessed in coming months following the end of lunar new year holidays.

In Europe meanwhile, Q4 GDP and the December CPI will both highlight sub-par momentum in the Continent’s economy.

The big news was the WHO:

The WHO has declared a public health emergency because of the spread of the virus outside of China, describing it as an “unprecedented outbreak”.

The total number of cases outside of China has reached 98 across 18 countries, Tedros Adhanom, director general of the WHO, has just told a press conference.

Eight cases outside China have spread via human to human contact, in Germany, Japan, Vietnam and the US. There are currently no deaths outside of China.

The organisation congratulated China, saying the declaration was not a vote of no confidence in the country, on the contrary, “the WHO continues to have confidence in China’s capacity to control the outbreak”.

The organised praised the “extraordinary measures taken” despite the social and economic impact on Chinese people. “We would have seen many more cases outside China, and probably deaths,” Adhanom said, if not for the work

However, Adhanom expressed concern for countries with weaker health systems, saying that we “must all act together now to limit further spread”. He said the WHO were willing to support those countries in any possible way.

Seems it’s everybody but China’s fault.

No end in sight to either the virus or the Australian dollar plunge.

David Llewellyn-Smith is Chief Strategist at the MB fund and MB Super which is overweight international shares that will benefit from a falling Australian dollar.