The jig is up for Aussie household debt. There is gthering evience that the change is structural and that has huge implications for everything from the economy through politics and society.

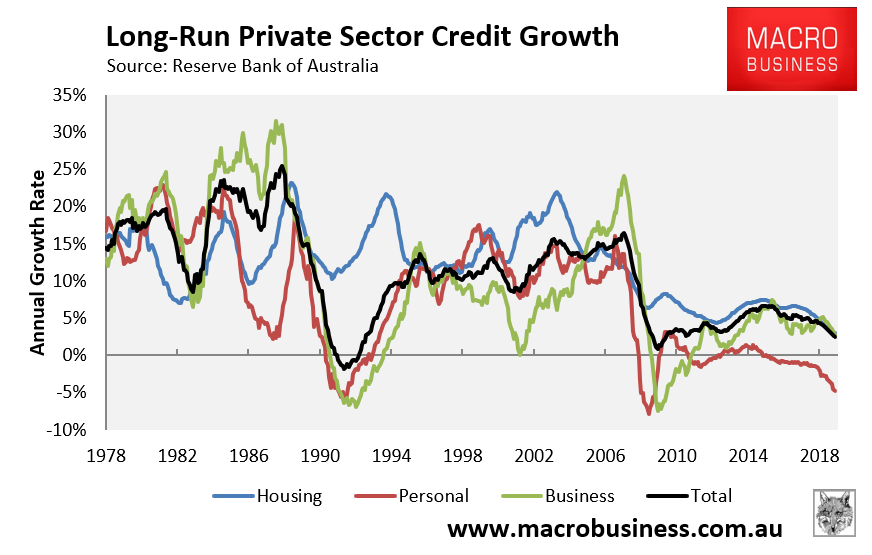

Total private sector debt growth has been lower than it is today before:

And it will rebound a little from current levels, all things equal. But credit growth has never been so low during a period of sustained and extreme monetary stimulus. The two previous episodes of deleveraging occurred in the 1991 recession and the GFC, the two greatest periods of economic shock in modern Australia. Today it’s happening as asset prices rip higher and after 27 years of continuous growth.

Ther are three drivers that argue this is structural.

First, income and wages growth is so slow, and has been so for so long, that households are bunkering down for a long slog with huge debts. They have realised that there is no chance of them inflating their way out it. We can see this in cratered inflation expectations.

Second, the Coalition Government is a major flop. Its surplus obsession is startlingly dated and has actually deepened as the need for it to turn towards a new paradigm of fiscal investment has increased. It has literally no reform agenda to lift incomes and is preoccupied exclusively with mortgage debt and house prices, the very revulsion entrenching in households, not least owing to the recent substantial correction.

Third, the imminence of zero interest rate policy has underlined the first two. Households know that there is now NO central bank insurance policy to fall back upon, no RBA ‘put’ to ensure the next downturn lifts income for the majority to help them service the huge debts.

These three factors have combined to acclerate mortgage debt repayments. Households might continue to borrow to invest, but they appear no longer willing to do so to consume, preferring to pay down loans much faster than in the past, a new form of saving. Weak bank mortgage flow is insufficient to keep the debt stock rising at anything above stall speed.

The economic and investment implications of this are large. It means chronically weak consumption and domestic demand, much diminished wealth effects hitherto assumed to boost economic activity, and all kinds of debt deflation taking hold across the consumption ecconomy for the foreseeable future.

That, in turn, means an ongoing weak labour market and even worse wages growth, gathering into an unbreakable feedback loop with weak domestic demand.

It will be made much worse as the terms of trade fall away over the next few years, dragged down by China going ex-growth.

The policy implications are equally big. The correct response is to embark on a wholesale reform project to boost incomes while undetaking major fiscal spending to support demand via infrastructure investment. Ratings agencies should be ignored. If Australia were downgraded, its 10 year yield might only fall to 55bps versus the 50bps that it is presently headed to. It’s absurd worrying about public debt when private has exceeded its tolerances everywhere and the federal government can issue bills at the cheapest prices in 600 years. It can significantly boost productivity with quality investment into the huge infrastructure deficit as well.

Regardless, the RBA will be cutting to 25bps in a jiffy and will be forced into QE before long. This is entirely appropriate if done right, aimed at boosting fiscal spending and lowering the currency which, longer term, is the only way out.

The third lever of Australian macro managemwent, mass immigration, will be a deepening disaster in this scenario. If private sector borrowing growth remains subdued then the housing and consumption spillovers will be curtailed. The extra warm bodies will simply crush per capita incomes ever more.

The political fallout is also big. The Coalition appears oblivious to the earthquake shaking its post-Howard economic assumptions, leaving it unwittingly crashing domestic demand. This opens an enormous opportunity for Labor if it can position itself as the new party of growth. Alas it has so far tacked towards Coalition idiocy but it should not go far that way. It need not overly expose itself to policy ideas in opposition to make the argument for real fiscal spending and reform to boost growth.

For asset markets, this change also represents a seismic shift. Australian banks are verging on univestible. For all intents and purposes they are now zombies. If their mortgage back books can’t grow then profits will structurally decline. For that matter, all Australian stocks exposed to anaemic domestic demand are in the same sinking boat.

Yields in the Australian bond market are yet to bottom. The cash rate at 25bps plus QE sees the 10 year and 15 year bonds at 50bps and probably lower.

The ‘bull trap’ thesis for house prices is strengthening given there will be no econony to support much higher prices. For owner occupiers the case for getting into the market is still reasonable given the emotional price for waiting is very high and the government will always offer support. But for investors it is a case of sell into strength.

The Australian dollar has far yet to fall. Offshore investments therefore present themselves as the local investor’s savior as Australia plods into a second, even worse, lost decade.

David Llewellyn-Smith is Chief Strategist at the MB fund and MB Super which is overweight international shares that will benefit from a falling Australian dollar.