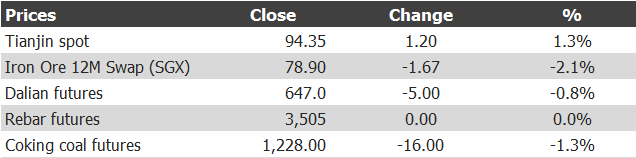

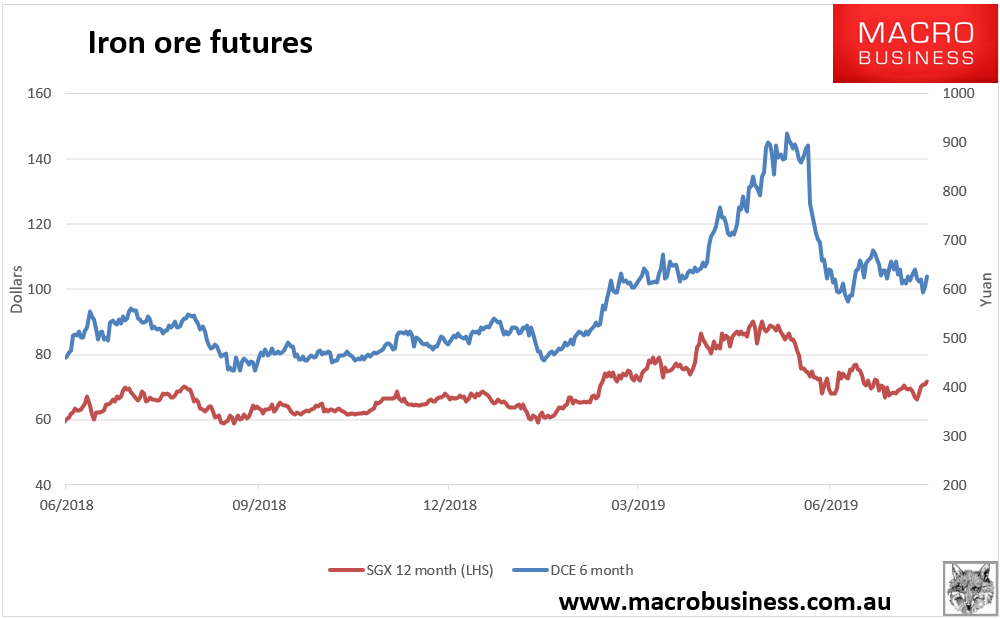

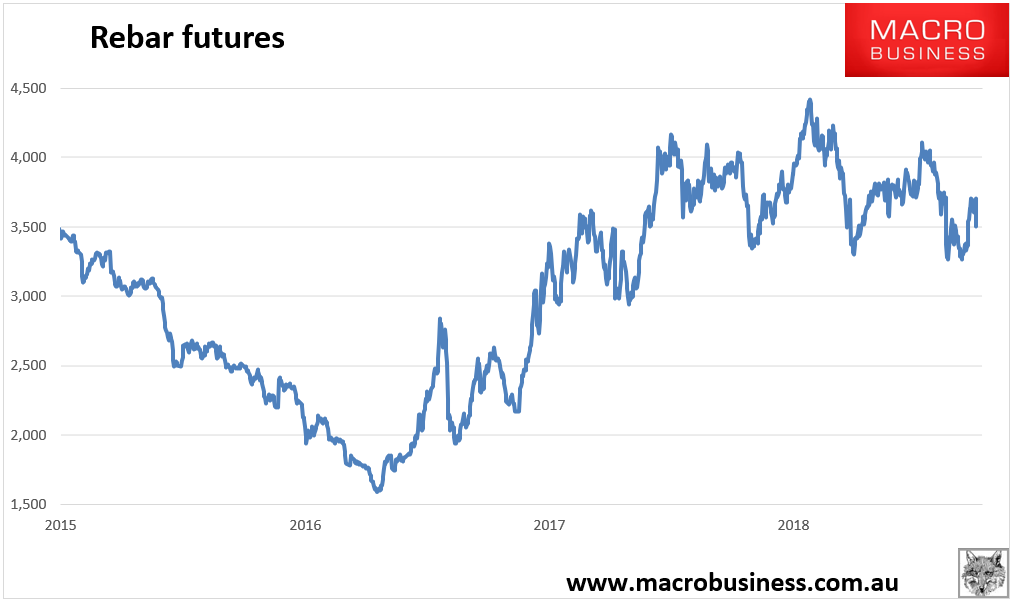

Iron ore charts for December 11, 2019:

Advertisement

Spot up. Paper down. Steel has not updated.

Westpac has a nice summry for 2020:

Iron ore charts for December 11, 2019:

Spot up. Paper down. Steel has not updated.

Westpac has a nice summry for 2020:

The full text of this article is available to MacroBusiness subscribers