The Australian’s Judith Sloan is the latest commentator to lambast Australia’s compulsory superannuation system. Sloan notes that various reports from the Productivity Commission have outlined the key problems with the system, including its unclear purpose, excessive fees, and unaccountable governance. However, the biggest issue remains the legislated increase in the contribution rate to 12% by mid-2025, which will cost taxpayers many billions, rob workers of disposable income, and accentuate the problems already present:

The hottest topic in superannuation remains the fate of the legislated increase in the superannuation contribution rate. Unless the statute is changed, this rate will be ratcheted up by 0.5 percentage points every year from July 1, 2021. A rate of 12 per cent will apply from July 1, 2025.

Every annual increase will cost the government about $2bn a year in forgone revenue given the cost of the tax concessions…

The superannuation industry is highly committed to these legislated increases going ahead. Some absurd pieces of research have been released to suggest that higher superannuation contribution rates do not involve any reduction to wage growth, something that is contradicted by the theory and actual practice, including on the part of the Fair Work Commission.

In the context of low wage growth, it will be a big call by the government to ask workers to forgo current pay rises in exchange for higher superannuation balances in several decades.

Moreover, for many workers, these higher superannuation balances will simply have the effect of knocking off their entitlement to the full age pension…

The bottom line is that superannuation remains a dog’s breakfast from a policy point of view…

Far from being the envy of the world, it has become apparent that our system of compulsory superannuation was a serious policy error enacted for short-term reasons to fend off a wages explosion. It may be too late to turn back but thought needs to be given to significantly reforming the system in ways that reflect the preferences of workers as well as generating a better deal for taxpayers.

Nobody can deny that Australia’s superannuation industry is a bloated parasite.

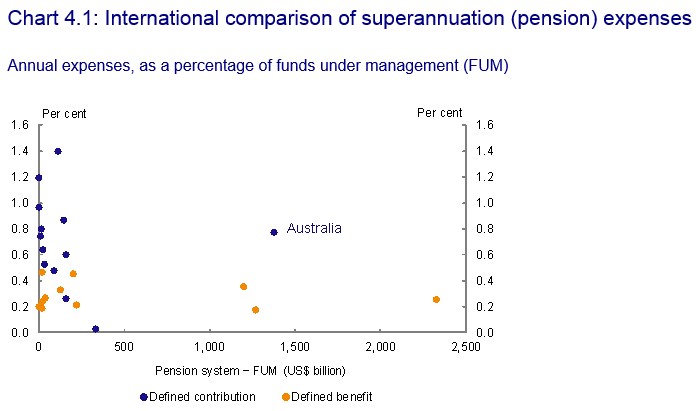

The Murray Financial System Inquiry found that despite the huge explosion of superannuation balances since the superannuation guarantee (compulsory super) was introduced in 1993, average fees and expenses have barely changed and are way above the OECD average:

Advertisement

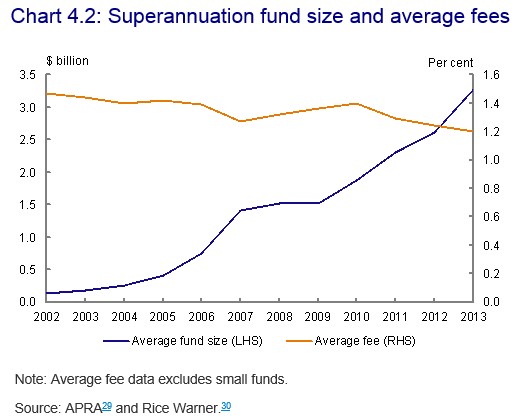

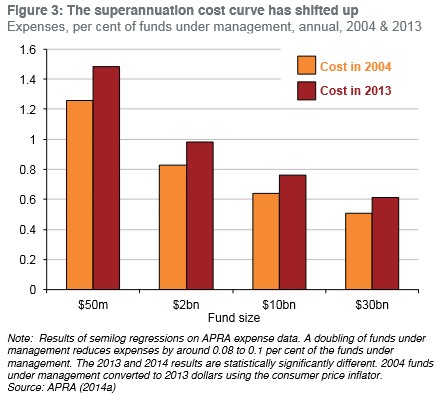

Whereas the Grattan Institute found that the superannuation system has actually become less efficient as it has grown:

Advertisement

A larger system of larger funds should have incurred lower costs and charge lower fees, because big funds have lower costs…

Australian funds charge fees that are three times the median OECD rate, on average… Many countries have superannuation pools much smaller than Australia’s, yet their funds charge customers much less.

Meanwhile, the Henry Tax Review found that compulsory superannuation concessions costs taxpayers more than it saves in Aged Pension costs:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

…both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

Given these major short comings, there is zero justification in raising the superannuation guarantee from 9.5% to 12%. All this would do is rob workers of much-needed disposable income, worsen the long-term sustainability of the federal budget, and worsen inequality.

Advertisement

About the only winners would be Australia’s bloated superannuation industry, which would get to ‘clip the ticket’ on more funds under management and earn fatter fees.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.