DXY slumped last night:

But so did the Australian dollar:

Gold firmed:

With oil:

Copper is trying:

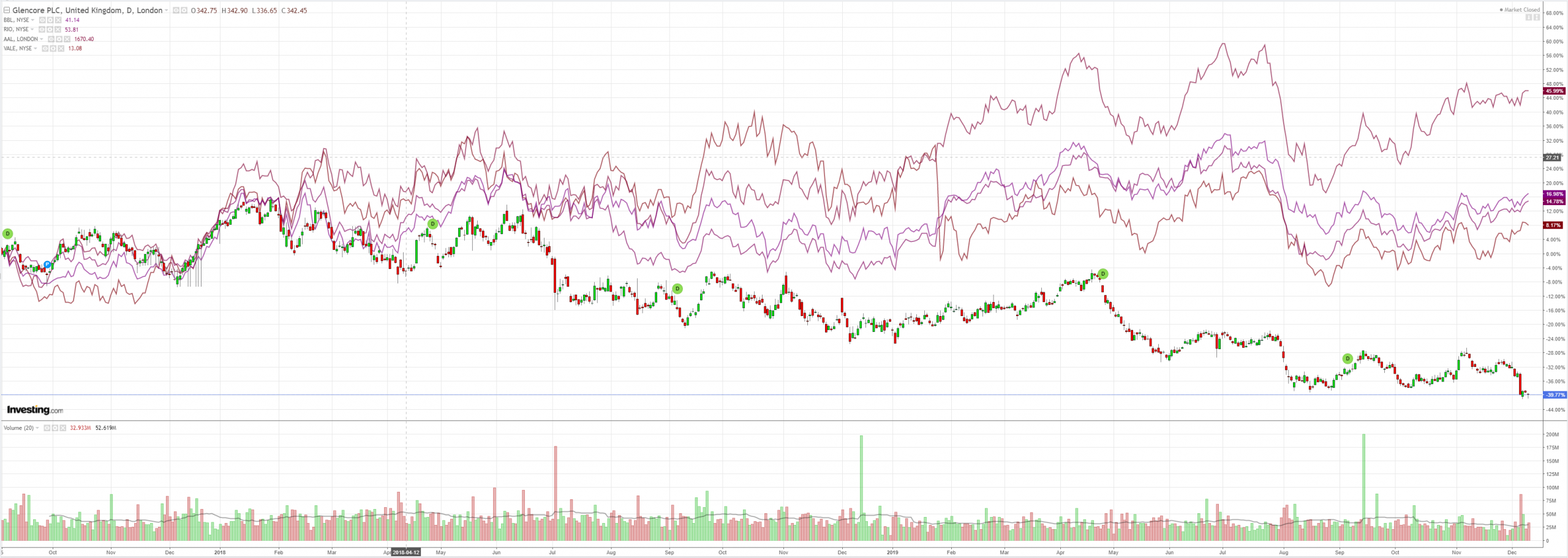

Miners firmed:

With EM stocks:

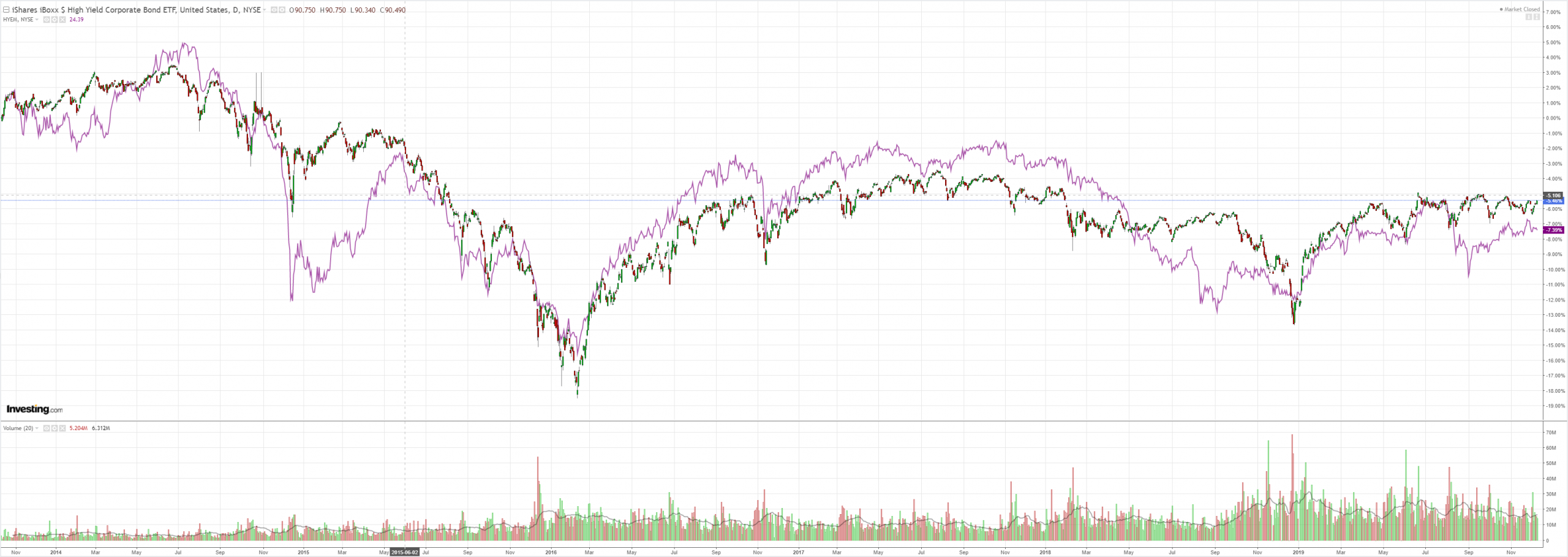

And junk:

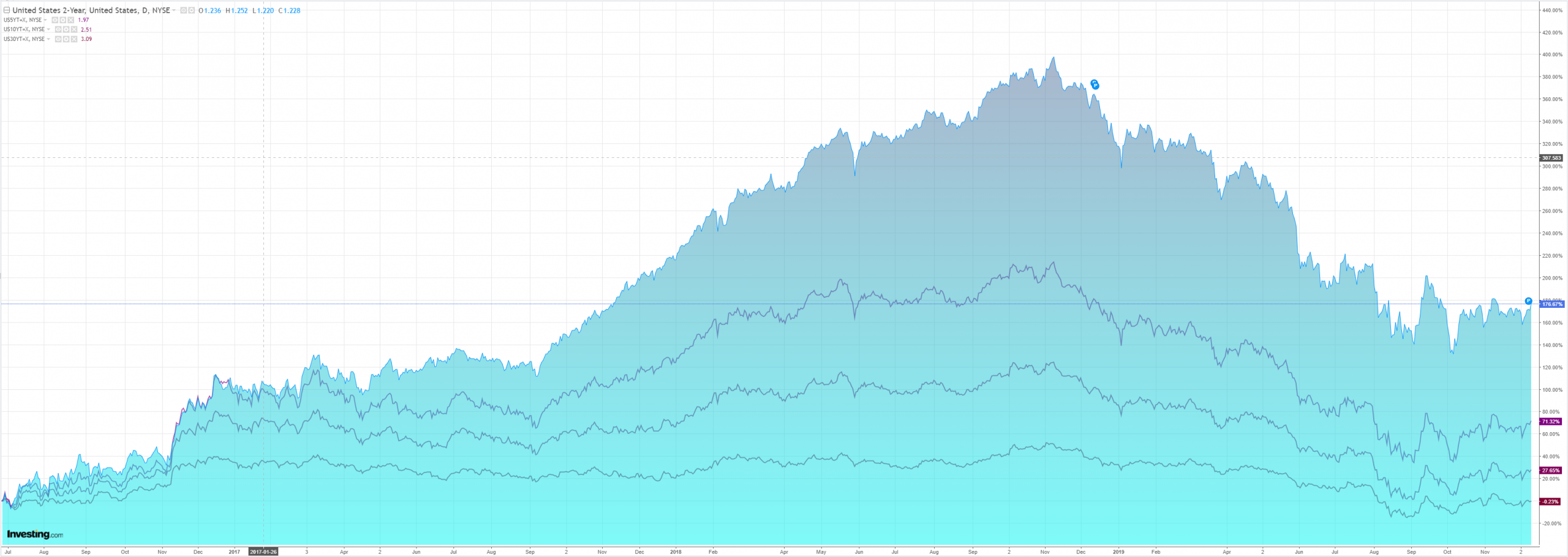

Treasury curves flattened:

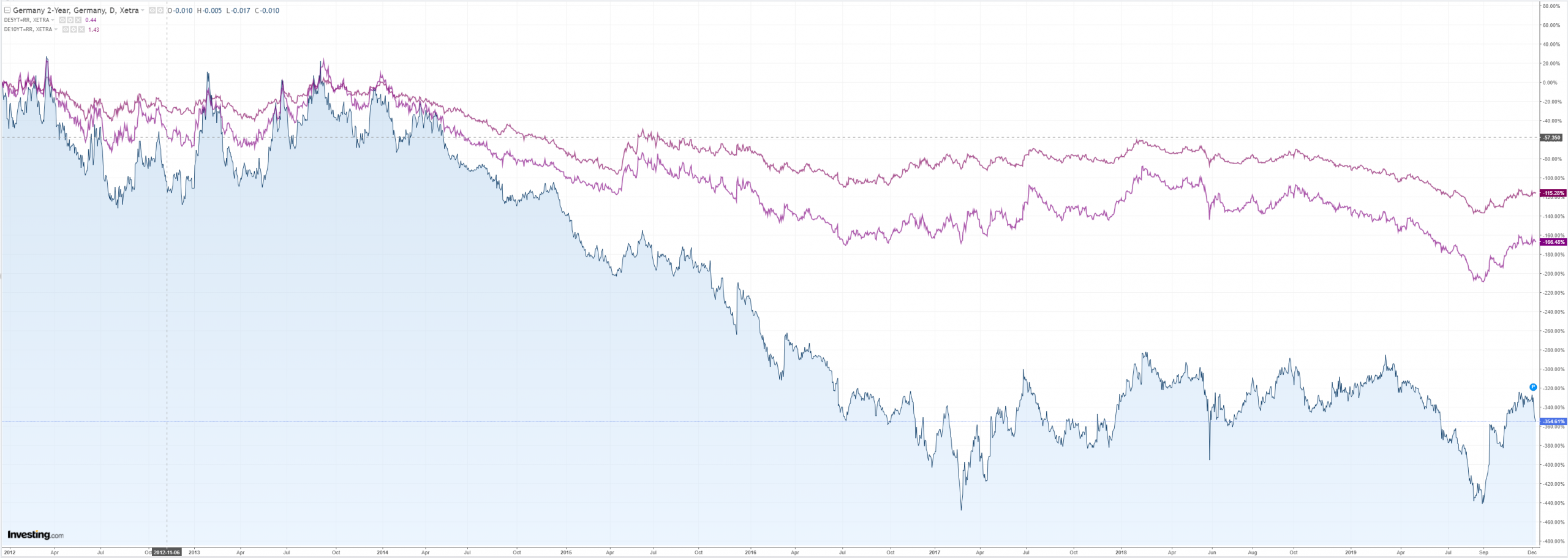

Bunds steepened:

Aussie split the difference:

Stocks are stuck:

Westpac has the wrap:

Event Wrap

US NFIB small business survey rebounded more strongly than expected to 104.7 (est. 103.0, prior 102.4) and remains firmly above its long-term average. Earnings were the main factor (second highest on record).

ZEW expectations surveys for Germany and Eurozone rebounded more than expected, to 10.7 (est. +0.3, prior -2.1) and 11.2 (prior -1.0) respectively, following -40 readings in August.

US officials Ross and Mulvaney said that US-China Phase 1 trade negotiations were progressing well, that meeting the 15 Dec. deadline was dependent on further progress, but suggested that further tariffs were unlikely (mirroring comments in the Asian media), without ruling them out.

US officials said that the USMCA was extremely close to being signed (if not today, then during this week). US Democrats Pelosi and Cuellar said that it should be voted on in the House next week.

US Democrats announced that the Presidential Impeachment process would continue on the counts of “Abuse of Power” and “Obstruction of Congress”. The White House said that Trump would address the charges in Senate.

Event Outlook

NZ: The half-year fiscal update (HYEFU) will be released at 1pm today. We expect an increase in spending to be announced, while respecting its Budget Responsibility Rules.

Australia: Dec Westpac-MI Consumer Sentiment is released.

US: the FOMC policy decision is universally expected to be on hold. After the October meeting cut, guidance is now that they will “assess the appropriate path” whereas previously would “act as appropriate”. This indicates the FOMC are in monitoring mode and December’s updated forecasts should reflect that stance. Nov CPI is anticipated to show annual headline inflation increasing to 2.0%yr form 1.8%yr while core inflation holds at 2.3%yr.

I am at a loss to explain the AUD dump versus falling USD. I guess it’s the sum total of trade rumours though they did not seem too bad.

The ZEW is worth a look:

If that persists it could lead to a stronger EUR and AUD next year than I currently expect. That is not my base case but it is a risk very much worth bearing in mind. Some see that outcome, via Bloomie:

Rabobank and Nomura Holdings Inc. see the Aussie dropping about 5% to 65 U.S. cents by December, wrenched lower by cooling economic growth and a dovish central bank. Others disagree: the currency may jump 14% to 78 U.S. cents in the same period on easing U.S.-China trade tensions, according to Monex Europe Ltd.

…Not everyone is bearish. Morgan Stanley says the Aussie may rise to 71 U.S. cents by the fourth quarter as an improving Chinese economy fuels demand for the currency. Bank of America Merrill Lynch tips the Aussie to rise to 73 U.S. cents by the end of 2020 amid a recovery in global growth.

…Rabobank strategists see the RBA potentially embarking on QE in 2020 as the Federal Reserve resumes cutting U.S. interest rates.

Rabo is right. The base case is for an ongoing weak domestic economy as construction busts, the consumer remains in her shell and the terms of trade fall.

That’s good insurance for AUD bears even if the global economy lifts more than expected.