Stephen Anthony – chief economist at Industry Super Australia (ISA) – clearly has a vested interest in raising the superannuation guarantee from 9.5% to 12%. Because more money compulsorily flowing into superannuation means more funds under management and bigger fees for ISA and its industry peers.

This vested interest helps to explain Anthony’s flimsy arguments in favour of raising the superannuation guarantee:

The SG plays a different role in a world where labour productivity is no longer being translated into real wages (as it once was) – employers have a capacity to pay the extra super without reducing wage growth…

Industry Super Australia SG analysis conducted by the doyen of Australia’s superannuation modellers, former Treasury executive Phil Gallagher, demonstrates that low-paid (and all other) workers would be better off with the SG increase.

According to ISA estimates, moving the SG to 12 per cent will mean a gain of 3.6 per cent annually in retirement, achieved by reducing disposable incomes by 0.6 per cent. In other terms, $1 of disposable income traded today buys you $5.25 of extra spending in retirement…

From the macroeconomic perspective, there must be a theoretical upper limit for SG contributions, but it certainly isn’t 9.5 per cent. John Hewson, an econometrician with a PhD from Johns Hopkins University, thinks that number is closer to 15 per cent. We agree…

It is worth considering that our nation, with its ageing population, faces fiscal deficits at both the Commonwealth and state level by the late 2020s, so surely self-provision should be encouraged.

Given its vested interest, it’s no surprise that ISA’s ‘modelling’ has found that the gain in retirement incomes from raising the superannuation guarantee far outweighs the loss of take-home pay over one’s working lives.

Advertisement

However, it is at odds with the findings of the independent Henry Tax Review, which explicitly recommended against lifting the superannuation guarantee because of its pernicious impacts on lower-income workers:

“Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners”.

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

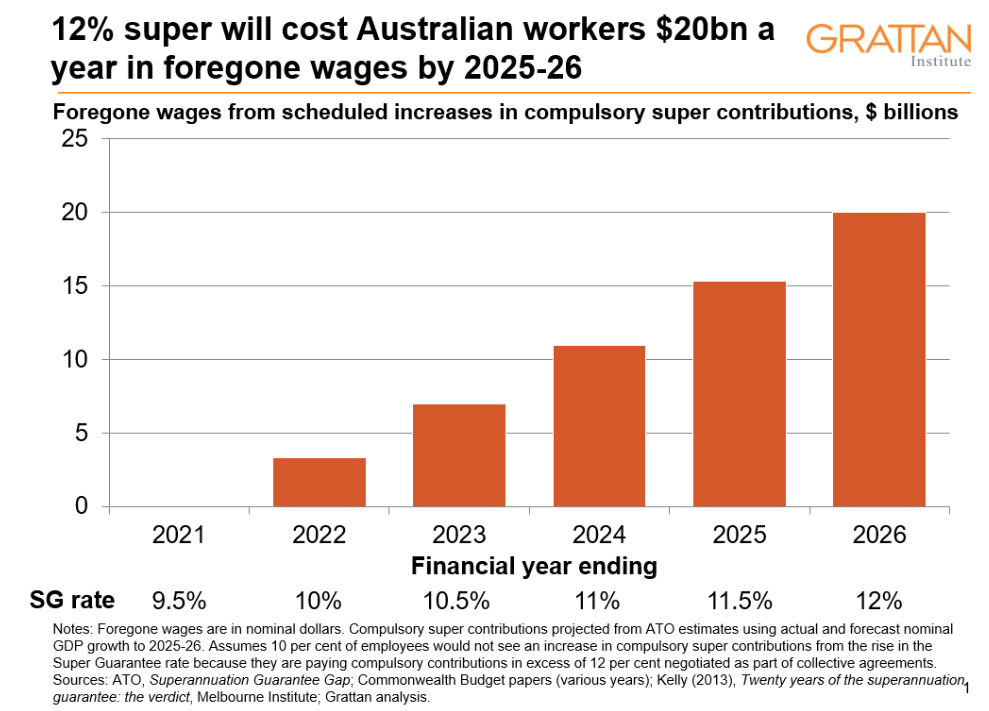

If compulsory super contributions go up, wages will be lower than they otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP…

ISA’s vested interest claim that raising the superannuation guarantee would relieve the federal budget is also at odds with the independent Henry Tax Review:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

…both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

Seriously, which claims about the superannuation guarantee should we believe? Those from an industry rent-seeker that benefits financially from the policy in question, or independent analysis that does not stand to benefit financially?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.