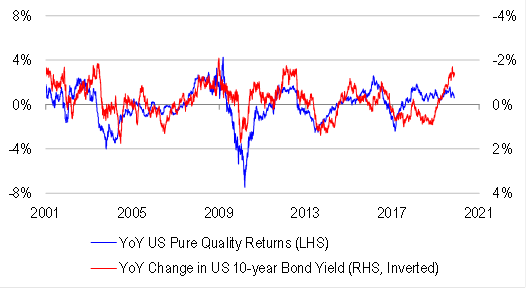

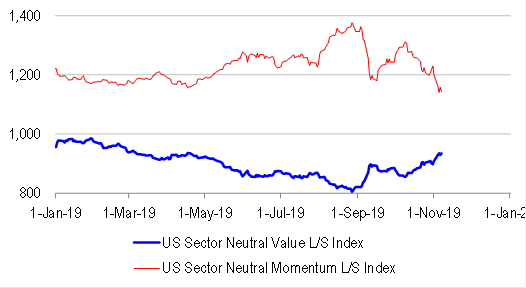

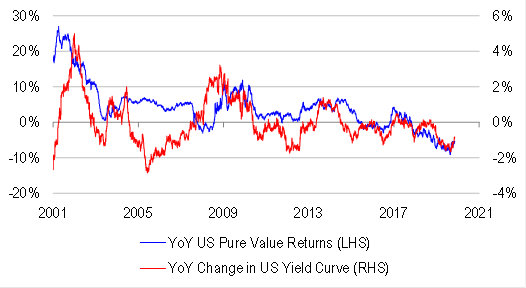

Another day, another set of US President Trump and China headlines. Overnight, we heard reports from Chinese officials that US officials were prepared to rollback existing tariffs as each phase of trade negotiations progressed. We later heard US officials confirm these reports from their perspective, although there has been some suggestion of strong internal opposition to rollbacks within the US delegation. In response to the constructive news, bonds sold off sharply, the yield curve steepened and equities rallied. Within equities, value factors outperformed, while momentum and defensive factors underperformed. Essentially, the rotation story from the past few months has continued.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.