We have just published an article on the drivers of the Sydney housing market recovery. Key points are as follows:

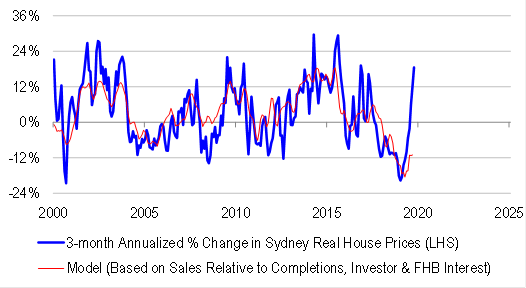

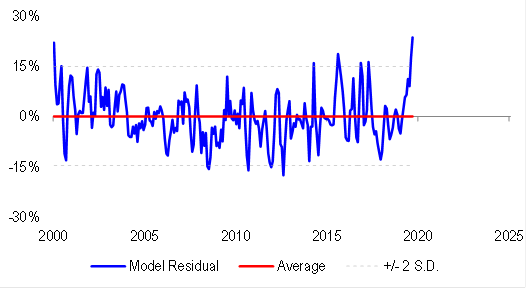

Sydney house prices are rising at a 22% quarter-annualized pace – but the speed of the recovery cannot be explained by local demand and supply factors. Our model of house prices based on home sales, net new buyer (investor and first home-buyer) participation, and supply from new construction and foreclosures, registers an improvement in the housing demand-to-supply balance – but not to levels consistent with an outright shortage in the market, and rising prices. Our model error as it were, is currently at all-time highs.

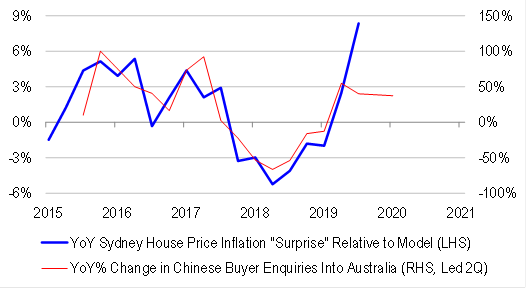

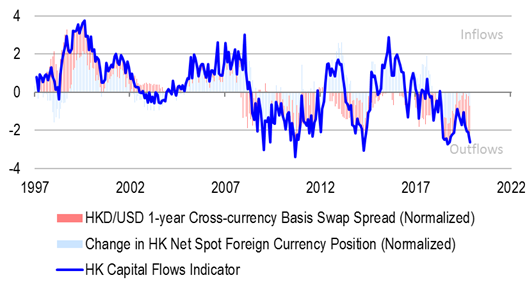

What local factors cannot explain, global factors can. Juwai Chinese buyer enquiries into Australian property predict and explain house price inflation “surprises” relative to our model. In the year-to-September, buyer enquiries rose by 37.3% nation-wide, and by almost 90% in Sydney alone. Also, we note that Hong Kong buying interest has risen by around 50% since civil unrest broke out, with our proprietary capital flows measure registering large outflows from the city.

What goes on in Hong Kong does not stay in Hong Kong. Surprisingly, large inflows into Hong Kong have correlated with outsized gains in Sydney house prices in the past. The correlation is completely the opposite of what we would expect. Essentially, history is telling us that when global credit creation has been strong, more money has flowed into emerging market gateways like Hong Kong, with “crowding in” effects. Central bankers have chosen to accommodate capital inflow through deposit and reserve expansion, rather than exchange rate appreciation. And the resulting excess liquidity has helped to fuel local credit and economic growth, as well as asset price inflation. As residents have grown in wealth and income, they have been able to export more capital abroad, supporting foreign property markets, like Sydney.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.