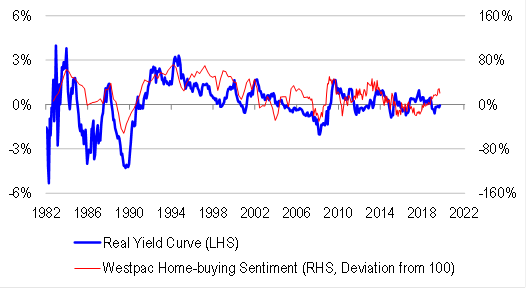

We model the slope of the real yield curve – the spread between 10-year inflation-indexed bond yields, and real 3-month interbank rates. We have demonstrated previously that the slope of the real yield curve can be reliably modelled as a function of four factors:

Home-buying sentiment.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.