In 2017, MB coined the phrase “shrinkflation” to describe the unusual phenomenon where housing transaction volumes fall at the same time as dwelling values rise strongly.

It appears that the Australian housing market is experiencing another episode of housing shrinkflation, with prices escalating at the same time as listings and transaction volumes have shrunk.

The below charts from CoreLogic’s October chart pack tell the tale.

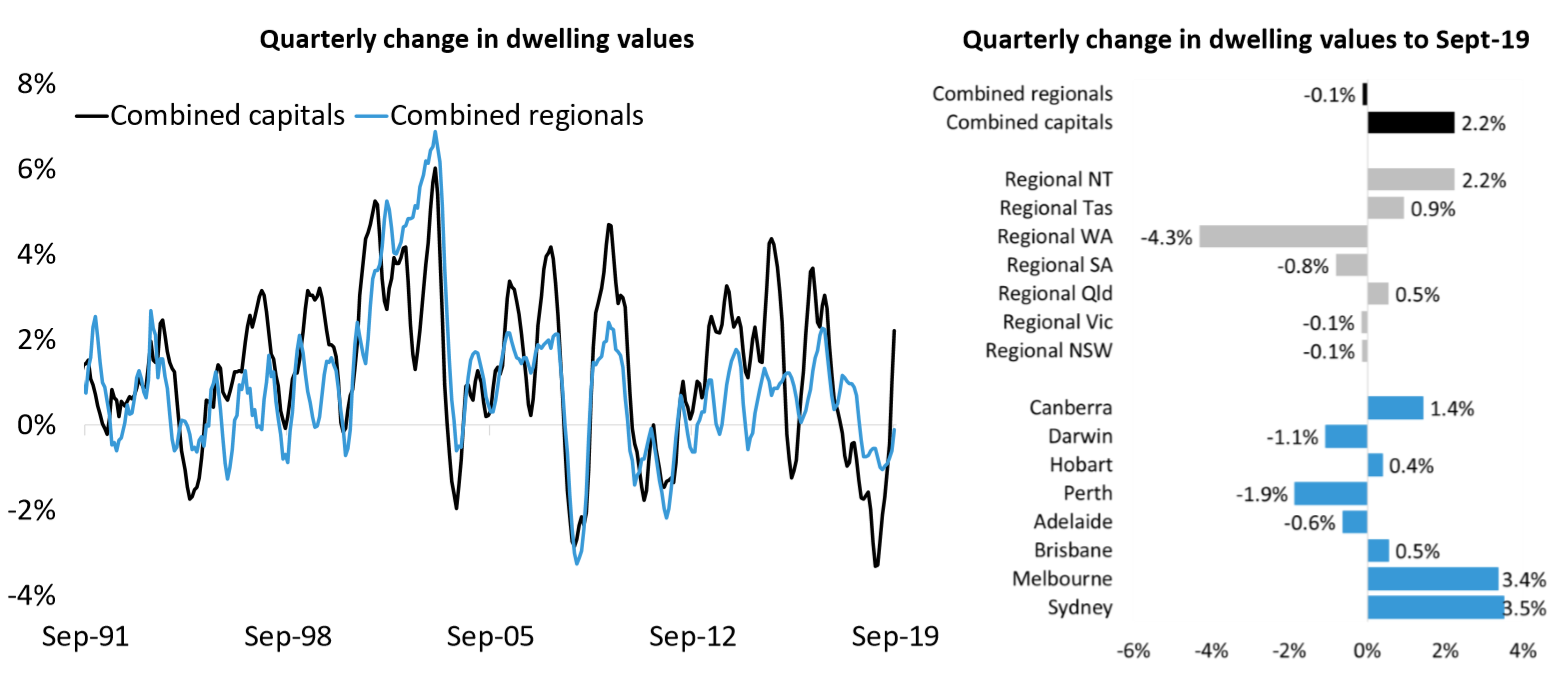

First, quarterly growth in dwelling values has surged, driven by Sydney and Melbourne:

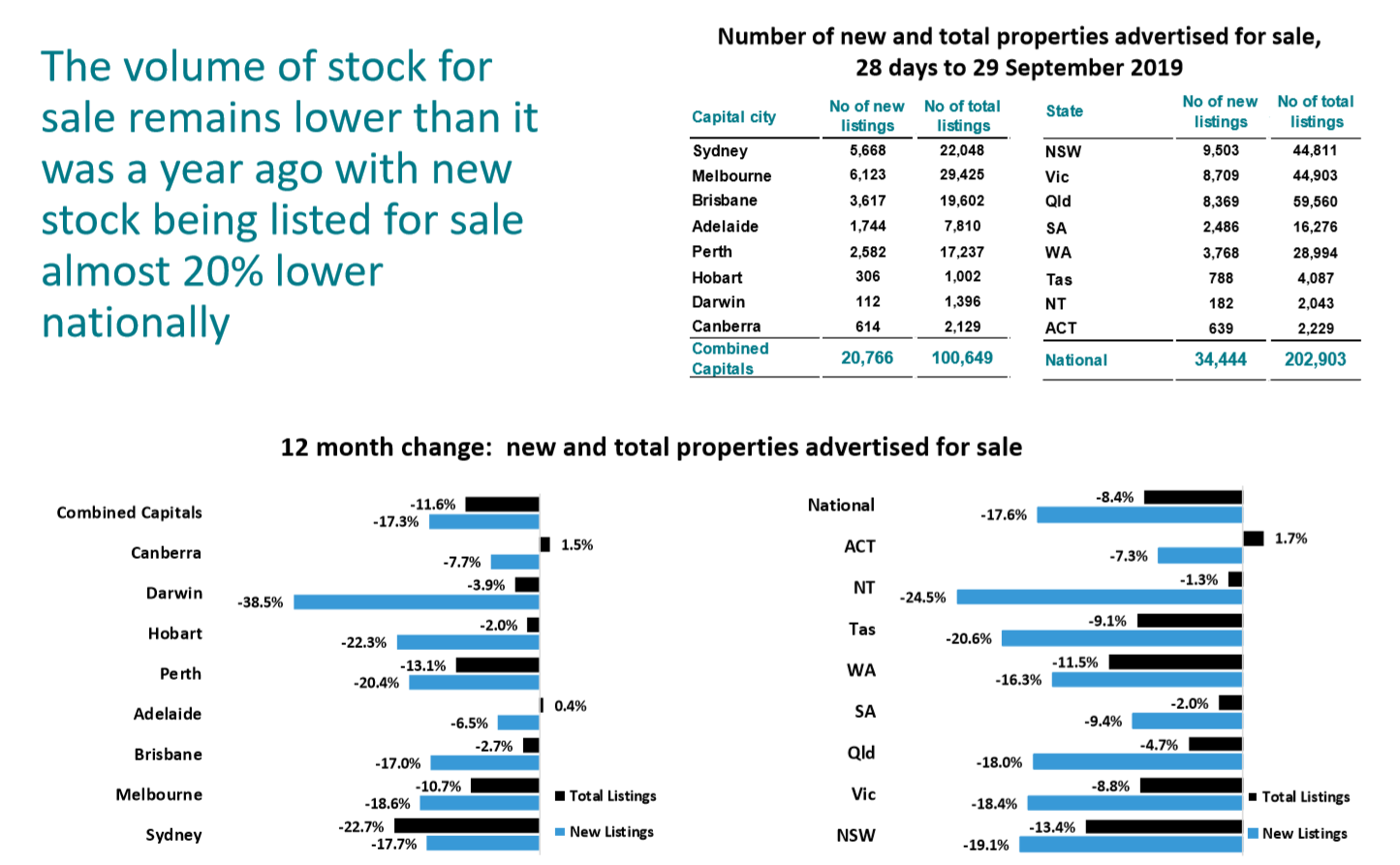

But the number of homes listed for sale has plummeted across almost all markets:

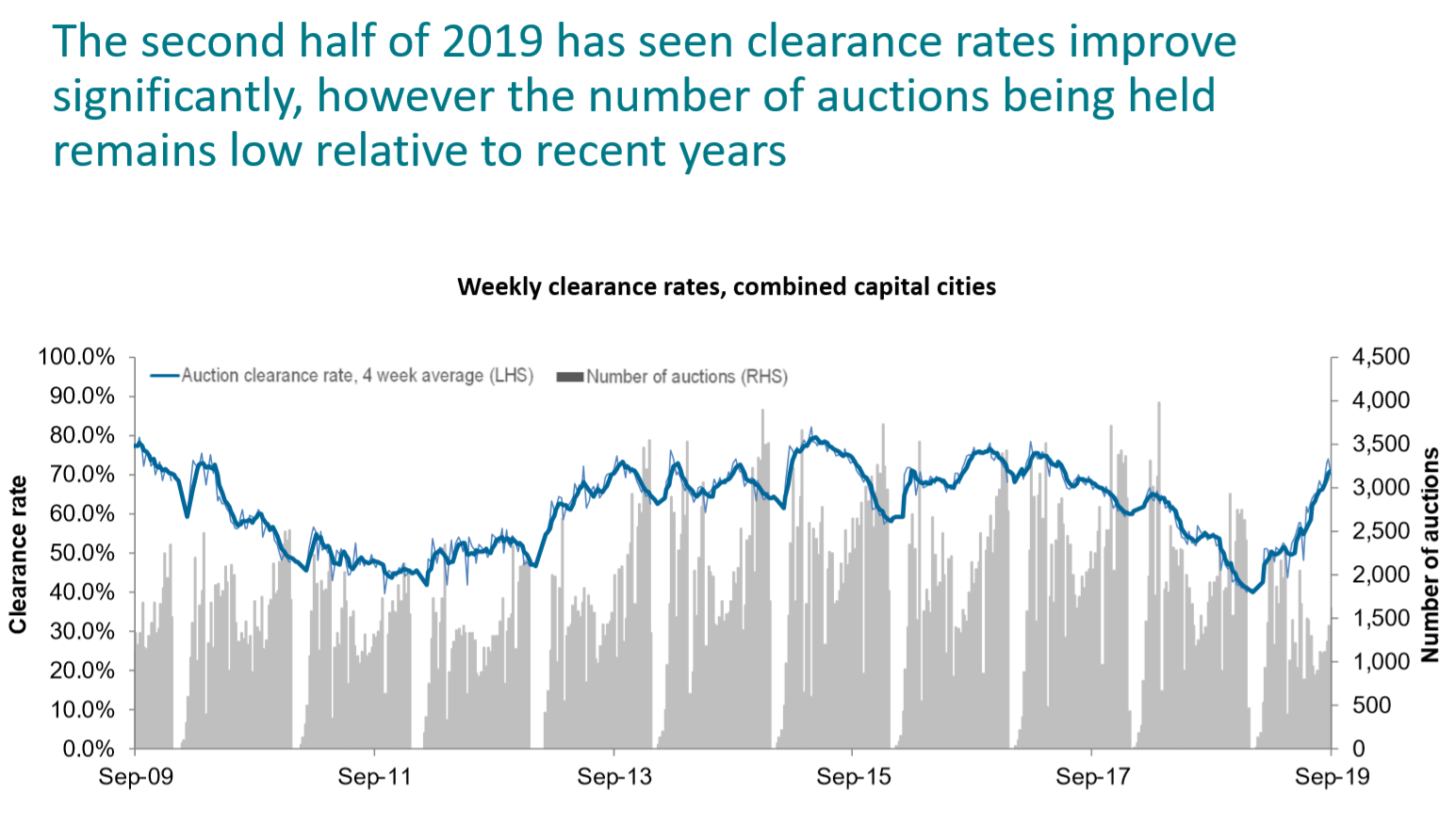

And while auction clearances are running at 2017 ‘boom time’ levels, auction volumes have gone bust:

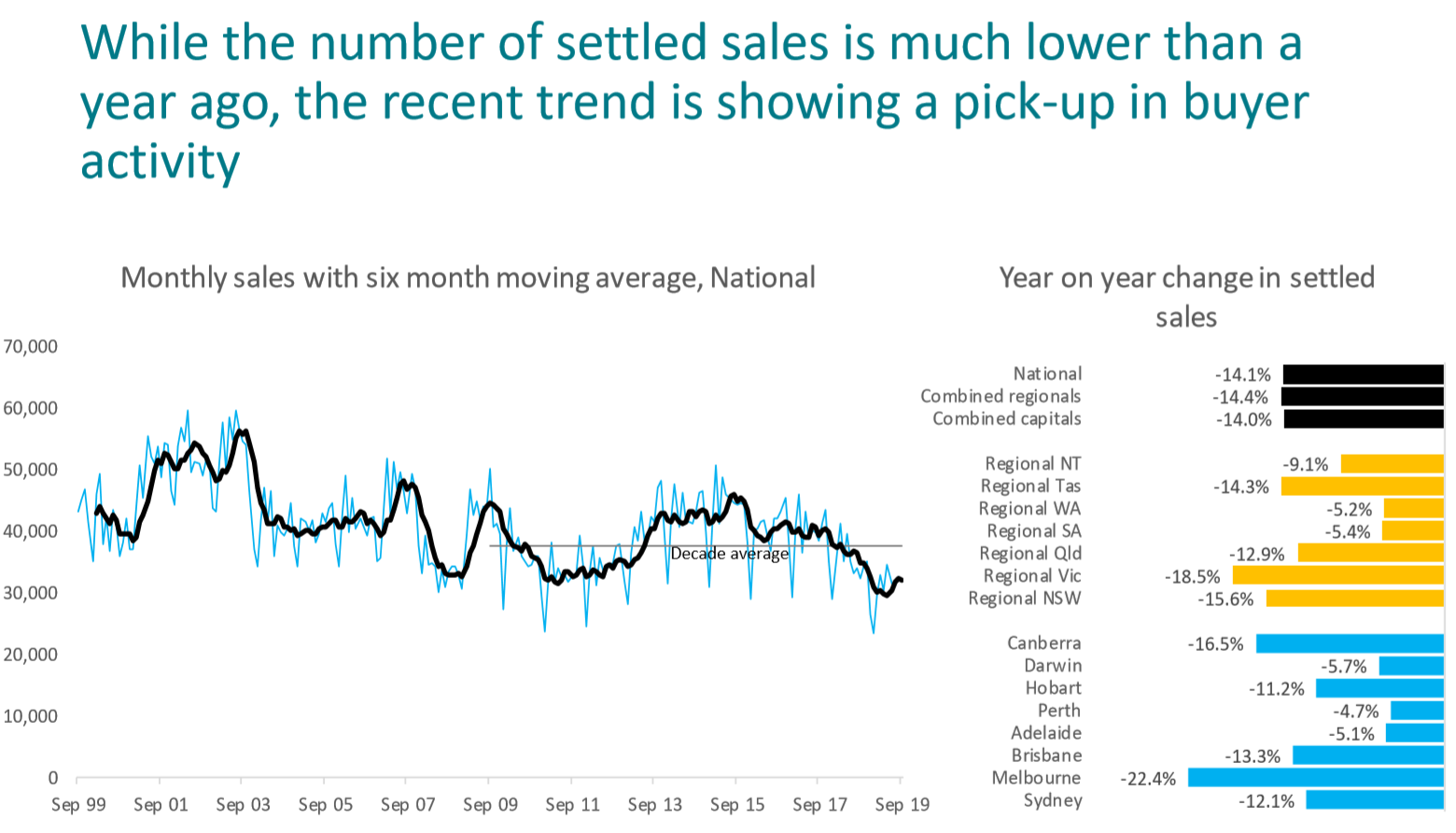

Finally, transaction volumes have crashed to levels way below the decade average; although they have shown some marginal improvement recently:

Basically, it is a very ‘thin’ market at the moment, and while dwelling values are rising strongly, the housing market is not exactly healthy.

We discussed these issues more deeply in our Q3 Subscriber’s report, which was released last week.