Paul Keating continues to spin lies about Australia’s superannuation guarantee (compulsory superannuation), claiming the following on Alan Jones yesterday (audio above):

Paul Keating: “Superannuation dramatically reduced the call by the Aged Pension on the federal budget. It was forecast to the 4.6% of GDP in 2030. This year, it’s 2.7% of GDP heading to 2.4%. In other words, superannuation has wiped-out the call by the pension system on the Budget…

Unless we have self provision in super, there’s just no way the Budget can carry the burden of the aged..”

This would have to rank as one of the most misleading statements I have heard.

Advertisement

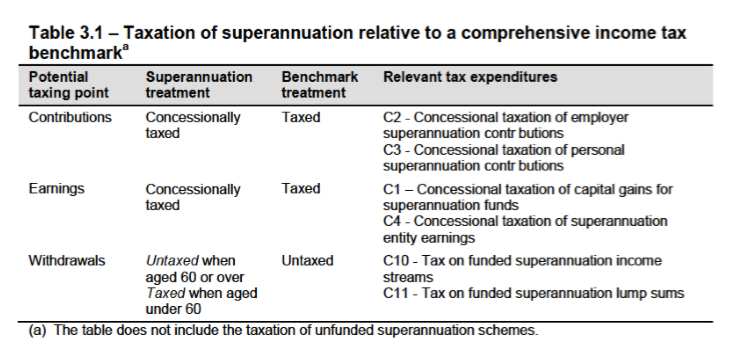

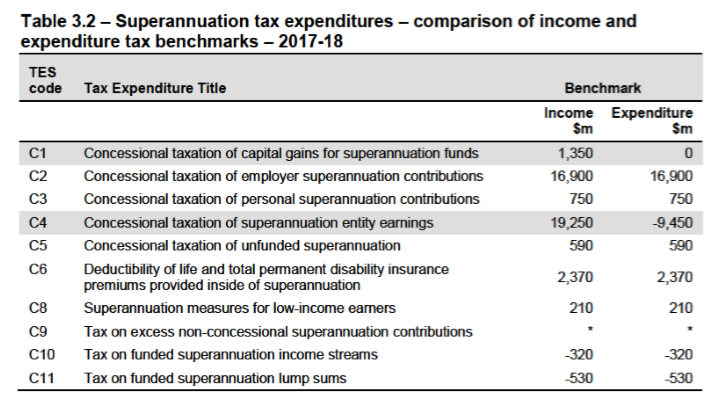

While it is true that compulsory superannuation has reduced the Aged Pension’s call on the federal budget, these Budget savings are outweighed by the enormous cost of superannuation concessions:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

The Grattan Institute has also shown that over “both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments”:

Advertisement

Back to Paul Keating:

Alan Jones: “What about the arguments that the high cost of superannuation reduces the prospect of a wage increase”?

Paul Keating: “Well it’s just a fib. It’s a lie. In the last six years, there has been no increase in superannuation contributions. And so the argument would run that the 2.5% that people are due [from not raising the superannuation guarantee to 12%] would come in wages of 2.5%. Well of course, there’s been no wage increases in six years. So, it’s demonstrably untrue that if you take super you lose wages. It’s demonstrably untrue”.

More bald faced lies.

Nominal wages have risen by 14% over the past six years. Raising the superannuation guarantee would simply ensure that nominal wages grow by less than they otherwise would, with the difference going into workers’ superannuation accounts.

If you don’t believe me, here’s what Paul Keating said in 2007, when he point blank admitted that the superannuation guarantee is paid for by workers through lower wage growth:

Advertisement

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost. Indeed, in each year of the SGC growth between 1992 and 2002, the profit share in the economy rose…

In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages…

When you hear conservatives these days speak of superannuation as a tax on employers they are either ill-informed or they are lying. The fall in unit labour costs and the upward shift in the profit share during the period of the SGC is simply a matter of statistical record. It is not a matter of argument…

Again, does Paul Keating suffer from amnesia? How is it that in 2007, compulsory superannuation was unambiguously paid for by workers through lower wage growth. But in 2019, it no longer is?

The Australian Treasury has also admitted that compulsory superannuation is paid for by workers via lower take-home wages:

Advertisement

Though compulsory SG contributions are paid by employees, wage setting generally takes into account all labour costs. It is widely accepted that employees bear the cost of higher SG in the form of lower take-home pay. This means there will be a trade-off between people’s income during their working lives and their income during their retirement.

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

The increase in the superannuation guarantee to 12 per cent will likely lead to lower wage increases, shifting a greater proportion of earnings into the superannuation system.

A major challenge for retirement incomes policy is the need for current consumption to be deferred in favour of future income in retirement…

No loss of remuneration is involved in meeting this national challenge. What is involved, rather, is forgoing a faster increase in real take‑home pay in return for a higher standard of living in retirement.

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

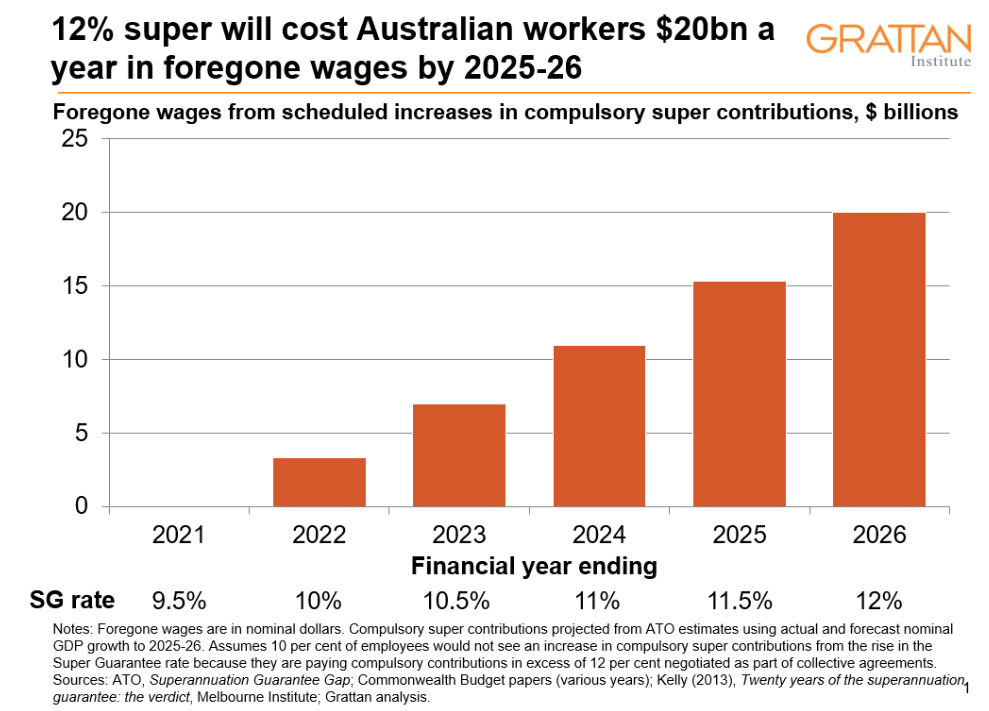

If compulsory super contributions go up, wages will be lower than they would otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP..

Advertisement

The only one telling “fibs” and “lies” is Paul Keating.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.