Like Groundhog Day, Paul Keating has hit out at those seeking to freeze Australia’s superannuation guarantee (‘compulsory superannuation’) at the current level of 9.5%:

Ordinary working men and women have been jammed by the Liberal party at 9.5% of wages going to super, while parliamentarians, without a hint of reflection or embarrassment, pocket 15.4% into their own super accounts.

And even though the parliament, and I emphasise the parliament, has legislated to compulsorily provide 12% of wages to the super accounts of the great body of the Australian workforce, the Liberal party wants to take it away. They want to kill the last two-and-a-half percentage points…

The government has repeatedly relied upon the discredited analysis of the Grattan Institute, which claims that if employees take extra income as superannuation they will lose the equivalent in wages.

This, of course, is a demonstrable lie. There has been absolutely no addition to compulsory superannuation contributions over the last five years, yet there has not been a jot of increase in real wages over the same period.

For the Grattan analysis to have been correct, we would have seen real wages rise by at least 2.5%, where, in fact, they have not risen at all. And what’s more, given the current international division of labour, the likelihood is, will not be rising.

So, were the government to convince the Senate to undo the current legislated 2.5% increase in super from 2021, Australian workers will simply lose 2.5% of personal income for the rest of their working lives.

Making this simple – working people will either get the 2.5% extra super or they get nothing.

Now compare this testimony to what Paul Keating said in 2007, when he admitted point blank that the superannuation guarantee is paid for by workers through lower wage growth:

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost. Indeed, in each year of the SGC growth between 1992 and 2002, the profit share in the economy rose…

In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages…

When you hear conservatives these days speak of superannuation as a tax on employers they are either ill-informed or they are lying. The fall in unit labour costs and the upward shift in the profit share during the period of the SGC is simply a matter of statistical record. It is not a matter of argument…

Advertisement

I mean seriously, does Paul Keating suffer from amnesia? How is it that in 2007, compulsory superannuation was unambiguously paid for by workers through lower wage growth. But in 2019, it no longer is?

Keating’s argument that because real wages have failed to grow over the past five years, this somehow justifies his position, is laughable.

Nominal wages have risen by 11% over that same five year period. Raising the superannuation guarantee would simply ensure that nominal wages grow by less than they otherwise would, with the difference going into workers’ superannuation accounts.

Advertisement

This is also the view of the Australian Treasury, who recently stated the following via FOI:

Though compulsory SG contributions are paid by employees, wage setting generally takes into account all labour costs. It is widely accepted that employees bear the cost of higher SG in the form of lower take-home pay. This means there will be a trade-off between people’s income during their working lives and their income during their retirement.

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

The increase in the superannuation guarantee to 12 per cent will likely lead to lower wage increases, shifting a greater proportion of earnings into the superannuation system.

A major challenge for retirement incomes policy is the need for current consumption to be deferred in favour of future income in retirement…

No loss of remuneration is involved in meeting this national challenge. What is involved, rather, is forgoing a faster increase in real take‑home pay in return for a higher standard of living in retirement.

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

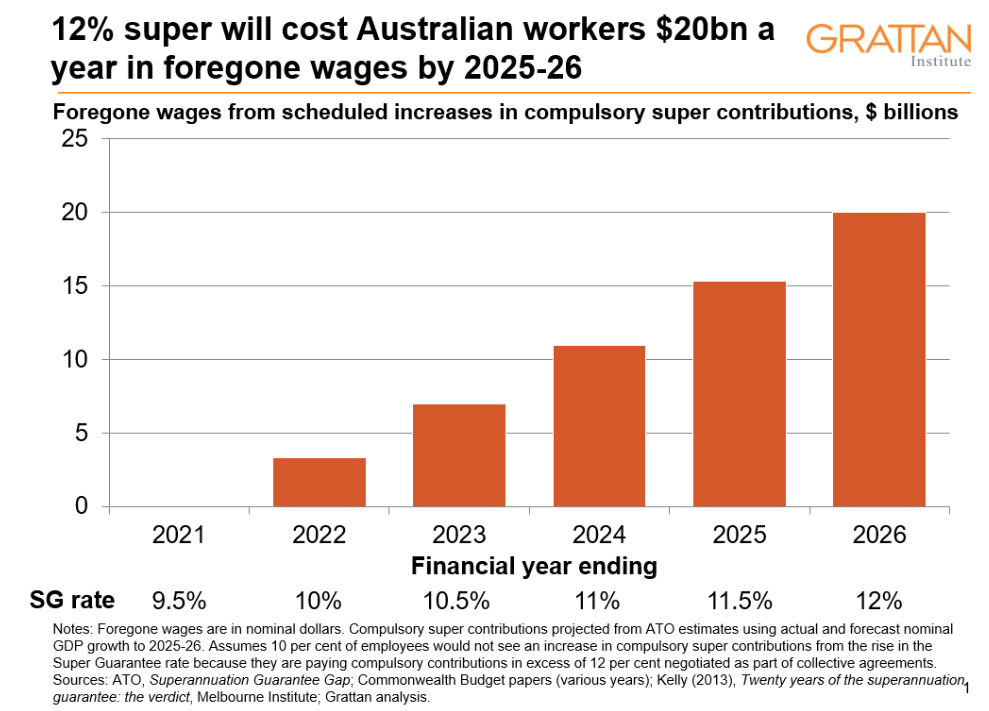

If compulsory super contributions go up, wages will be lower than they would otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP..

The only one who has been comprehensively “discredited” is Paul Keating, who continues to spout “demonstrable lies”.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.