While various Aussie China apologists use signing up to China’s One Belt, One Road as some kind of talisman to ward off the evil of arguing with Beijing, the truth is OBOR is already cooked.

Recently UBS noted that:

BHP stopped short of saying exactly when China would hit peak steel, choosing to say that it was plateauing and would peak sometime in the 2019-2025 timeframe. One Belt One Road (OBOR) was seen contributing to 1% pa growth in Chinese steel demand while domestically demand is flat. BHP estimated the scrap to steel ratio in China at 22% today, rising to somewhere between 33-60% over the long term. This is important for iron ore demand and while there is 30Mtpa of elastic iron ore supply in China that has come back on due to high prices, the low quality high cost producers in Australia and Brazil are the marginal players who will drive the long run iron ore price.

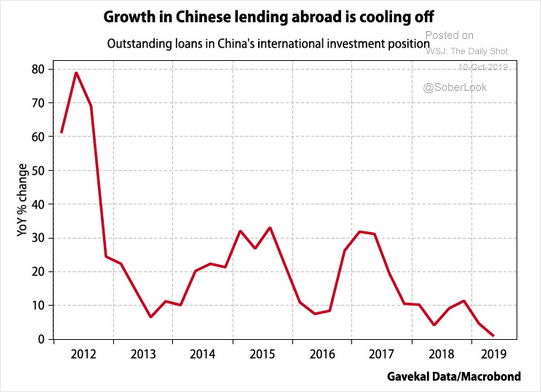

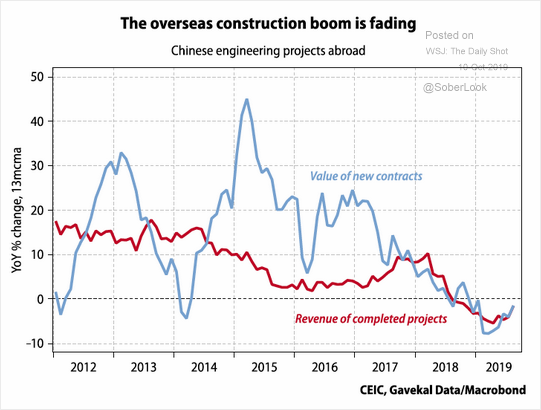

A few charts today suggest that is, in fact optimistic vis OBOR, via GaveKal:

OBOR suffers the same problem as all capex-driven growth. It’s the rate of change that matters to underlying demand not the absolute level. Once the ramp up of spending ends so does the growth.

For OBOR, we are there and the benefits for Australia will diminish from here.