Is there any difference? Via the excellent Damien Boey at Credit Suisse:

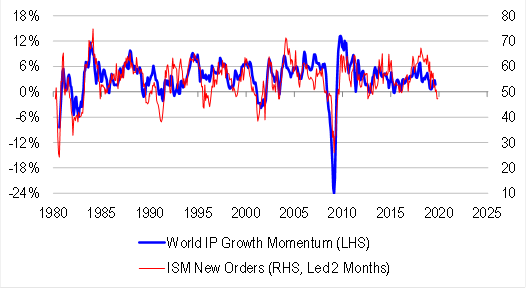

What a wild ride it was for bonds overnight! In the Asia-Pacific time zone, bonds sold off aggressively outside Australia, as investors became worried about a potential slowdown in BoJ asset purchases in a fairly illiquid environment. But in the US time zone, the ISM manufacturing index came in below expectations, remaining at 47.8 in September, consistent with ongoing contraction in world industrial production. Bonds rallied strongly on the back of this, more than clawing back earlier losses.

Equities sold off on the weak ISM data. Within equities, defensive momentum plays outperformed, while value and small caps underperformed. Macro remained front and centre, even for stock pickers.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.