Texture from Reuters:

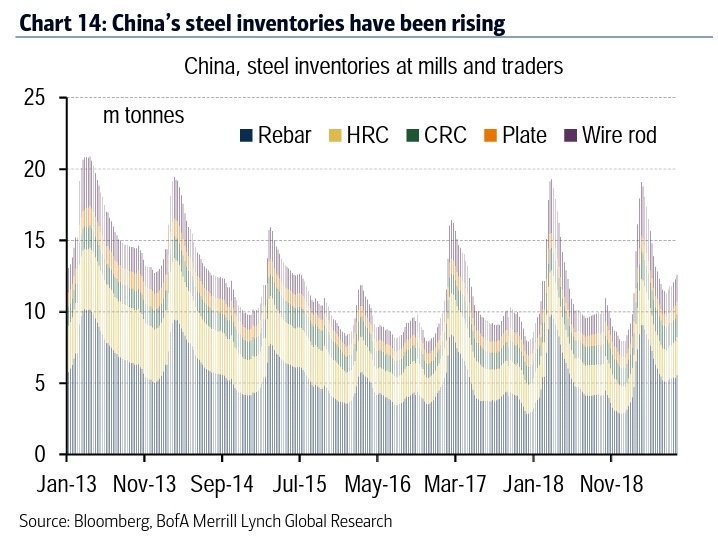

Steel product inventories in China notched up a third weekly decline in the week to Oct. 25, down 600,000 tonnes from the previous week at 9.85 million tonnes, marking the lowest level since mid-January, according to data compiled by Mysteel consultancy.

That is normal for time of year and it has cleared some of the excess inventory we saw in Q3: