Over the past few days, we have witnessed some rather sharp deterioration in the leading indicators of Australian growth:

Westpac consumer confidence fell sharply in early October to 92.8 from 98.2. For reference, readings below 100 have historically been associated with contraction.

Westpac home-buying sentiment fell in early October to 116.6 from 123.4, with NSW and VIC leading the declines. Sentiment is off its recent lows, but the relapse is concerning considering the extent of credit loosening and rate cuts.

NAB business confidence fell to -0.4 in September from 1.1, while business conditions improved slightly to 1.6 from 0.6. Capex intentions fell sharply to 2.9 from 6.2, while employment rose to 3.5 from 1.7.

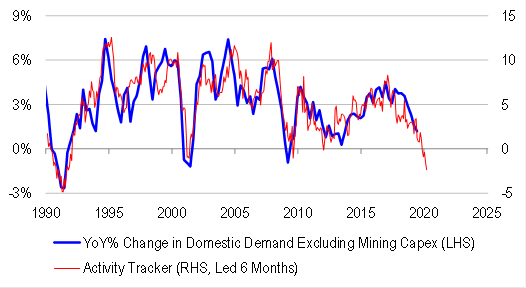

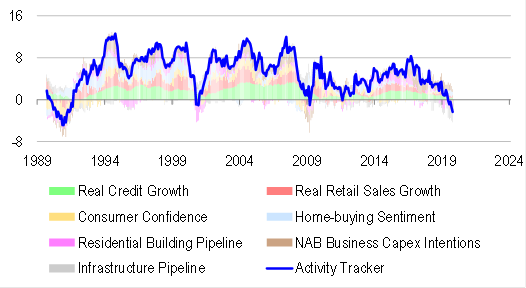

Feeding the relevant data points into our proprietary domestic demand tracker, we find that the non-mining economy is in a deep state of contraction – in fact, the deepest contraction since the 1990s recession. The economy is in a lot of trouble from this perspective.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.