Australia’s vast household debt a giant economic millstone

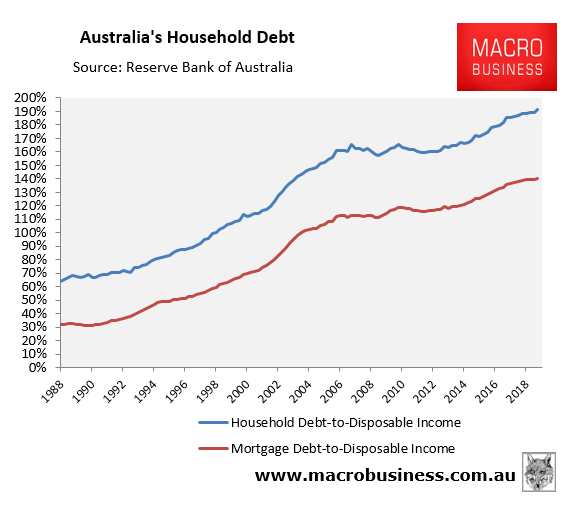

Over the June quarter, Australia’s household debt hit a record high 191% of household disposable income, after roughly tripling since the late-1980s:

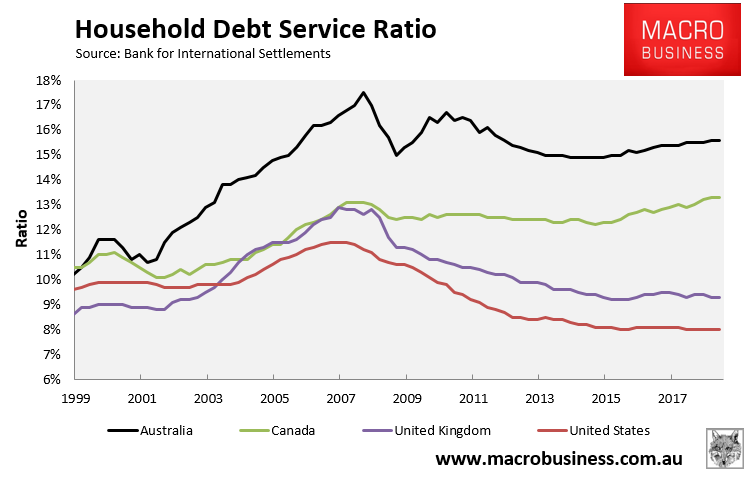

The latest Bank for International Settlements (BIS) global household debt data also confirmed that Australia has the second highest debt load in the world behind Switzerland, as well as the second highest average principal and interest payments on debt:

According to the ABC’s Michael Janda, Australia’s record household debt loads have become a millstone around the economy’s neck, forcing households to both work longer and spend less:

Ninety per cent of the nearly 55,000 respondents to the ABC’s Australia Talks National Survey rated household debt as a problem for the nation.

On an individual level, 37 per cent are struggling to pay off their own debts, with almost half of millennials reporting that debt is a problem for them personally…

Professor Roger Wilkins from Melbourne University is the deputy director of HILDA… says housing debt has more than doubled in real terms since HILDA was launched in 2001.

“So it’s now averaging around about $350,000 for those who actually have mortgage debt, compared with around about $160,000 in 2002, 2001,” he observes…

“When people are increasing their debt from one year to the next, they’re essentially accessing the equity in their home … people are evidently using that increased equity to fund consumption.

“Now that consumption could take many different forms — it could be renovating the home, it could be going on holiday, buying a new car.”

The problem is, after many years of a virtuous circle of rising home values on the back of rising debt, allowing further rises in home values and funding our lifestyles, to an extent the music has stopped…

“Such things as reducing interest rates as a guaranteed way of increasing demand so that there’s more employment, more housing, more purchase of housing and so forth, that no longer works”…

“What this research from the RBA shows is that households that have a higher level of debt, even if they have the same level of wealth overall, are going to have lower levels of consumption,” says Zac Gross, an economics lecturer from Monash University who used to work at the Reserve Bank…

Given Australians are amongst the world’s most indebted people, it’s no surprise then that we’re not running to the shops…

But we’re not just saving money by spending less, we’re also trying to work more.

Professor Rachel Ong ViforJ from Curtin University has found that the increasing number of older Australians who have yet to finish paying off their mortgage are far more likely to remain in the workforce.

“If you’re aged in your 40s, 50s or 60s and you’ve paid off your mortgage debt then the odds of you leaving the workforce is about four to five times higher than someone in the same age group who still has a mortgage debt burden,” she says…

Dr Manning says the ultimate flow-on from continued high debt levels is the risk of a financial and economic crisis if Australia’s overseas creditors get nervous about our ability to repay what we owe them on time and in full…

“If foreign lenders begin to take a dim view of Australia and, particularly, its banks, they’ll be reluctant to reinvest, they may require a higher interest rate, they may, in the last instance, simply refuse, in which case you’ve got big problems,” he says.

There’s nothing here readers of MB don’t already know. We’ve raised these risks repeatedly since our inception in 2011.

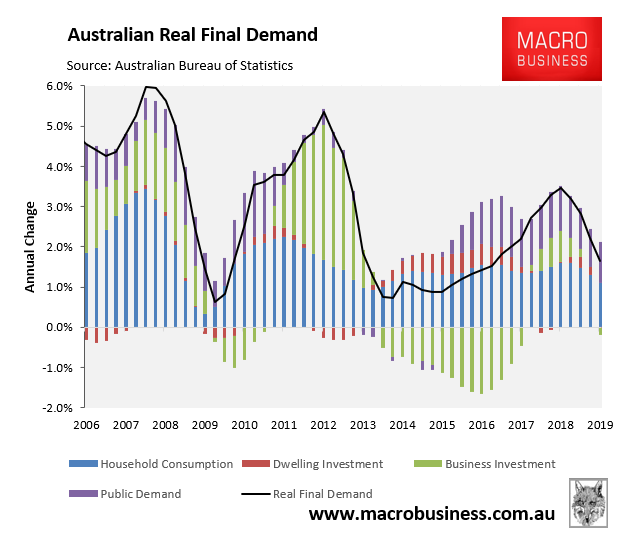

The drain on Australia’s economy is illustrated below. Household consumption accounts for around 55% of Australia’s final demand:

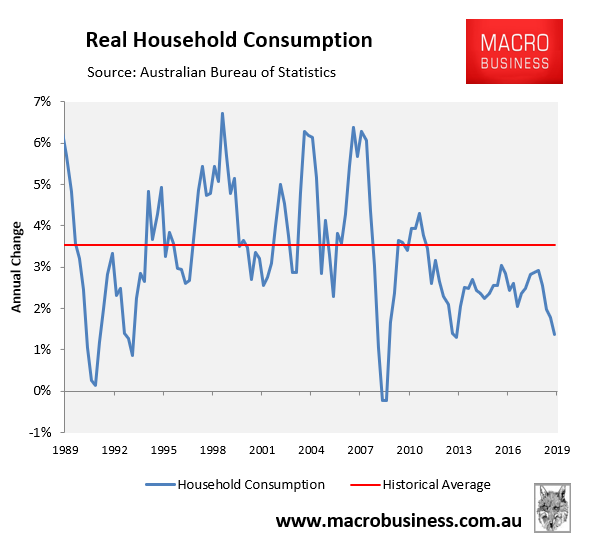

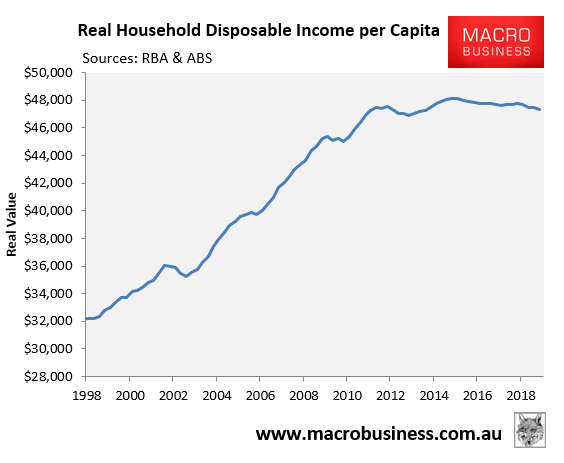

Household consumption is falling fast as consumers tighten their belts amid stagnating incomes:

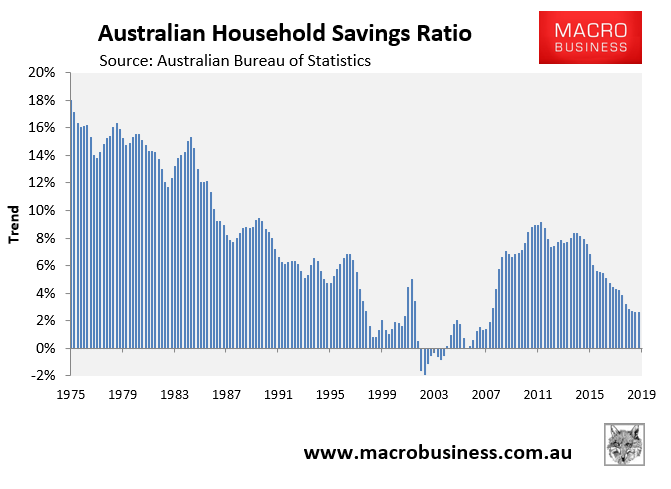

As bad as the situation is, it would be much worse had the household savings rate not crashed and household debt risen, thus allowing households to increase their consumption spending as their incomes stagnated:

Obviously, the ability (and willingness) of Australian households to continue leveraging up to fund consumption is hitting its limits, which means that consumption spending growth must continue to fall.

Which make you wonder the Government’s overriding economic plan is to drive that leverage higher.

Basically, the Australian economy is facing a long period of sluggish demand growth as our record high household debt becomes a giant millstone around the economy’s neck.