Treasury analysis, obtained under Freedom of Information, claims that raising Australia’s superannuation guarantee (‘compulsory superannuation) to 12% would lower wage growth and would make the gender retirement savings imbalance even worse:

Though compulsory SG contributions are paid for by employers, wage settings generally takes into account all labour costs. As such, it is widely accepted that employees bear the cost of higher SG in the form of lower take home pay. This means there will be a trade-off between peaople’s income during their working lives and their income during retirement.

The main driver of women having lower balances than men are women’s lower incomes and longer career breaks. While the increase in rate of SG would increase retirement balances for women, it would likely lead to an even larger increase in male retirement balances due to their high lifetime earnings.

Nobody should be surprised by this result given it basically echoes the findings from the Henry Tax Review:

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

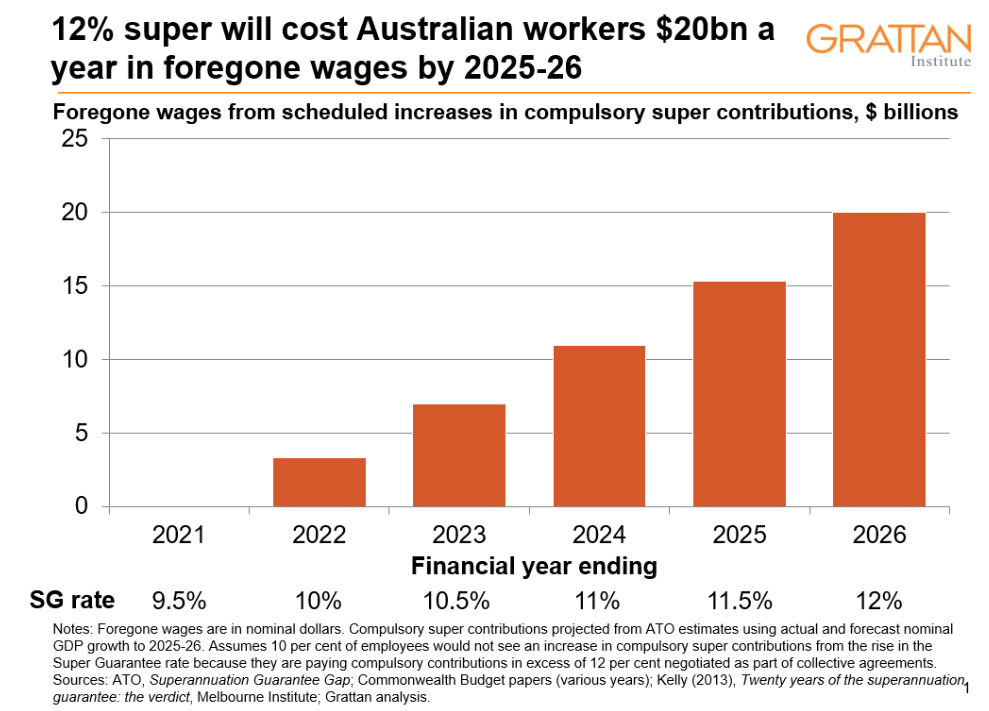

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

If compulsory super contributions go up, wages will be lower than they would otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP..

The increase in the superannuation guarantee to 12 per cent will likely lead to lower wage increases, shifting a greater proportion of earnings into the superannuation system.

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost… In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages.

Advertisement

I could go on, but you get the drift.

While the industry’s support in raising the superannuation guarantee is understandable, given it would directly profit from the increased funds under management, Labor needs to hang its head in shame for supporting a policy that would unambiguously lower the wages of its purported working-class base.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.