Credit Suisse has released its 2019 Global Wealth Report, which reveals that the recent housing bust has pushed Australia down the wealth rankings, falling from second place to fourth:

According to Credit Suisse:

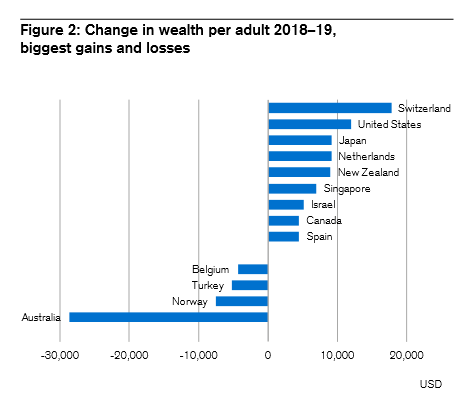

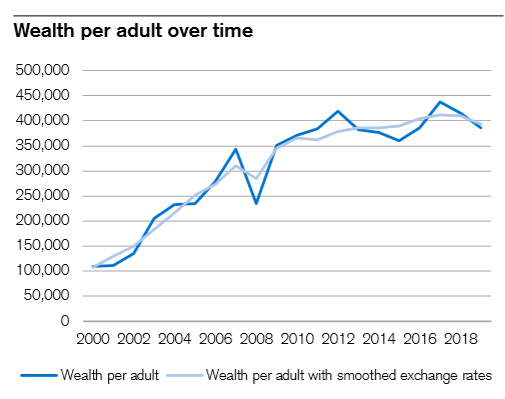

Household wealth in Australia grew quickly between 2000 and 2012 in USD terms, except during 2008. The average annual growth rate of wealth per adult was 12%, with about half due to exchange-rate appreciation against the US dollar. The exchange-rate effect went into reverse after 2012, with the Australian dollar declining 33% relative to the US dollar. The result is that wealth per adult in 2019, at USD 386,058, is close to its 2011 level of USD 384,640. In real AUD terms, however, wealth per adult today is 16% above its 2011 level. Despite the exchange rate effects, Australia’s wealth per adult is fourth highest in the world in US dollars. In terms of median wealth, it ranks second after Switzerland.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.