Superannuation industry pundits remain at odds over whether the federal government should follow through with the planned legislated increase in the superannuation guarantee from 9.5% to 12%.

QIC CEO Damien Frawley has called for more flexibility regarding the compulsory superannuation guarantee. He argues that some employers and people on low incomes cannot afford the legislated increase to 12% by 2025, so there should be scope for the superannuation guarantee to have multiple tiers, such as 7.5% and the current level of 9.5%:

“If lower earners can’t afford to put 12 per cent away, or an employer can’t afford 12 per cent, let them stay on 9.5 per cent or drop it to 7.5 per cent,” he said…

He suggested “slicing and dicing” the system, acknowledging that there were some employers and employees who might be able to afford to increase their super contribution to 12 per cent, while lower earners might not be able to.

But he did not support allowing people to opt out of the system altogether as this would create a pension burden later.

However, Australia’s largest not-for-profit super fund has demanded the government stick to its legislated increase to 12%, but has urged that the inequitable concession structure be addressed:

Australian Institute of Superannuation Trustees chief executive Eva Scheerlinck said low-income earners would be hurt by a super freeze.

“Those who oppose the 12 per cent or indeed compulsory super on the basis that it will leave low-income earners worse off are attacking the wrong target,” Ms Scheerlinck said…

“It’s the taxation of super that needs adjusting, not the superannuation guarantee rate,” Ms Scheerlinck said. “Adequacy and equity are two separate issues that have been conflated into the one argument by those who are either defeatist or lack the political will to tackle the elephant in the room, which is that we need to better target the super tax concessions which disproportionately benefit the very wealthy.”

“We need to keep our super strong – we need 12 per cent.”

Meanwhile, The SMH’s Nina Hendy claims that compulsory superannuation has been successful in reducing reliance on the Aged Pension:

It has been 27 years since the introduction of compulsory superannuation… The average consolidated super balance for a typical couple starting retirement today is $400,000, according to Challenger retirement income research…

Less than half (45 per cent) of new 66-year-old retirees accessed the age pension in 2018, the latest data available, while a quarter (25 per cent) were drawing a full age pension, the data also revealed.

While in 2002 the age pension represented 2.9 per cent of Gross Domestic Product and was forecast to keep climbing until the middle of the century, recent projections show that the success of the super system appears to be reversing the government’s pension liability…

As previously revealed by The Australian, Treasury’s new modelling system, known as MARIA (Model of Australian Retirement Incomes and Assets), found projections of the share of GDP that Australia spends on the age pension is “consistent” with a fall to 2.7 per cent last year, and is expected to drop to 2.5 per cent by 2038.

There’s a several overlapping issues here that need to be unpacked.

First, lifting the superannuation guarantee would unambiguously lower wage growth (other things equal). Industry Superannuation Australia admitted this last week, thus confirming the findings of the Henry Tax Review, the Grattan Institute, the Parliamentary Budget Office, and employer groups.

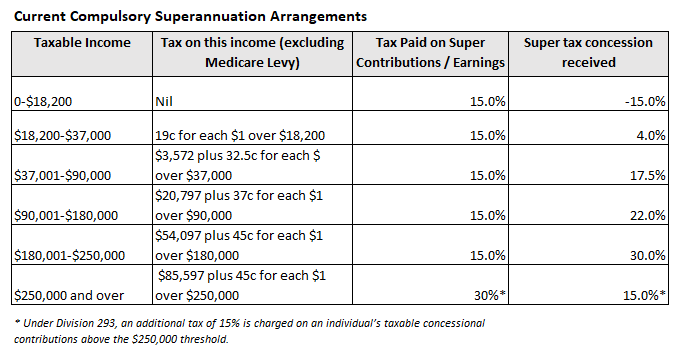

Second, the current structure of superannuation concessions is highly inequitable:

And this has resulted in higher income earners receiving the lion’s share of benefits:

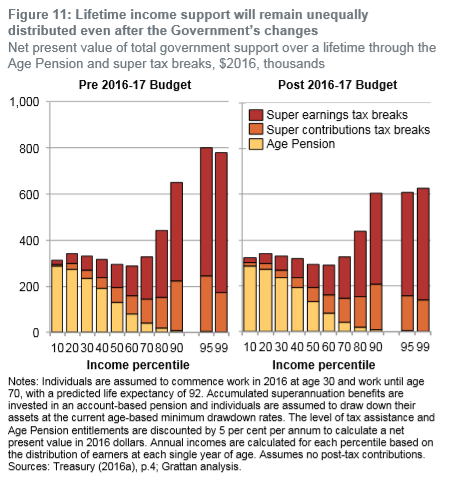

Accordingly, the superannuation guarantee costs the federal budget more than it saves in Aged Pension costs, according to both the Henry Tax Review:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

As well as the Grattan Institute, which estimates that over “both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments”:

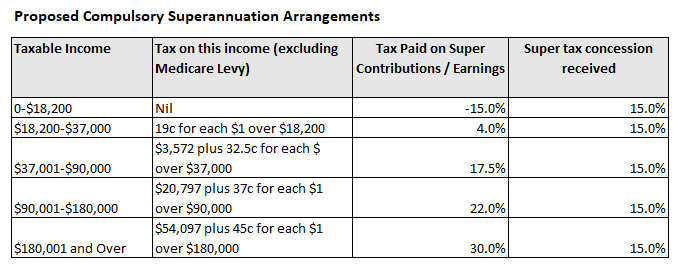

Therefore, the first best solution is to reform the superannuation system to make concessions more equitable and sustainable.

In particular, the 15% flat tax on contributions/earnings should be replaced with a flat-rate refundable tax offset (e.g. 15%):

This way, everyone that contributes to superannuation would receive the same concession, the system would be made progressive, and lower income earners would retire with far bigger superannuation balances without needing to contribute more (and without suffering lower wage growth).

The long-term cost to the federal budget would also be lowered, since lower income earners would become less reliant on the Aged Pension.

Reforming superannuation concessions should be the key priority for reform and should take place before any further increase in the superannuation guarantee rate.

Because lifting the superannuation guarantee in isolation would merely heighten inequities already rife across the system, would rob younger (and lower paid) workers of much-needed disposable income, as well as worsen the long-term sustainability of the federal budget.