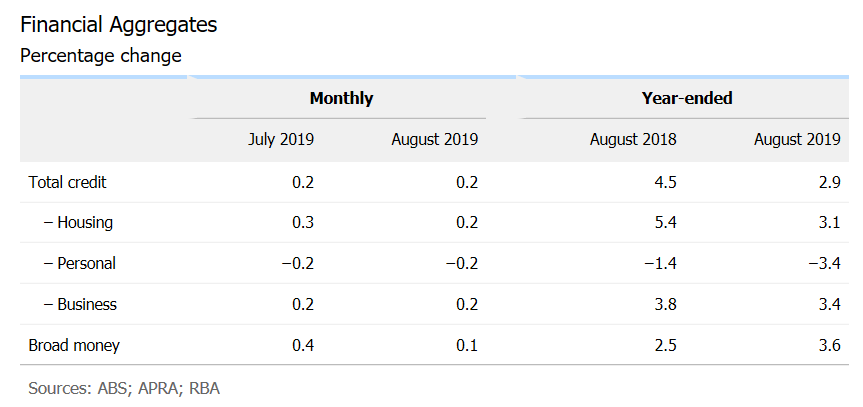

The Reserve Bank of Australia (RBA) has released its private sector credit aggregates data for the month of August 2019:

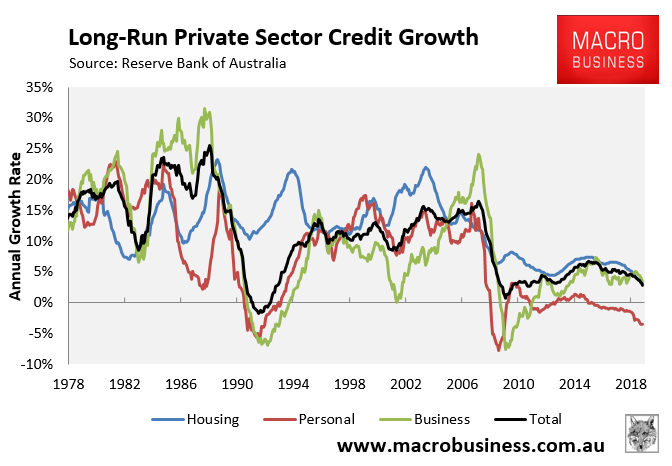

A chart showing the long-run breakdown in the components is provided below:

Personal credit growth (-0.2% MoM; -0.6% QoQ; -3.4% YoY) has plunged, whereas business credit growth (0.2% MoM; 0.5% QoQ; 3.4% YoY) and housing credit growth (0.2% MoM; 0.6% QoQ; 3.1% YoY) are at least growing, albeit slowly.

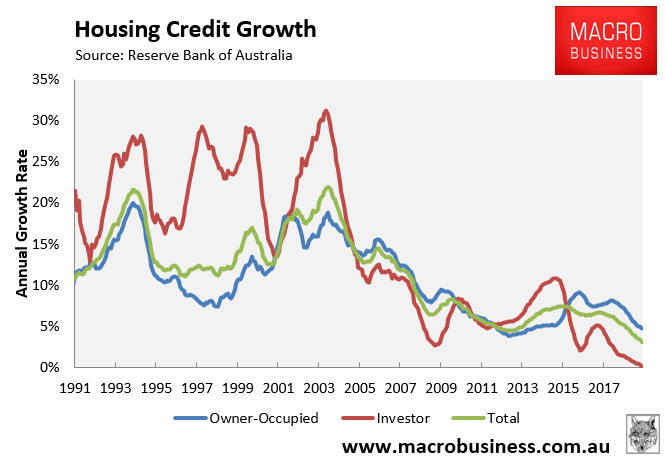

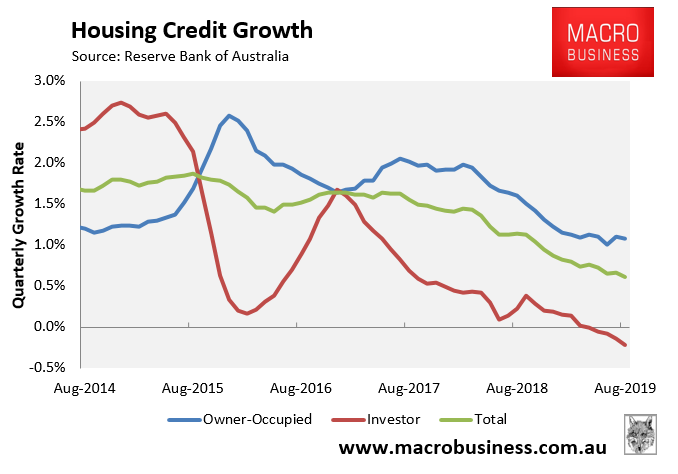

A long-run breakdown of owner-occupied credit (0.34% MoM; 1.08% QoQ; 4.72% YoY) and investor credit (-0.10% MoM; -0.22% QoQ; 0.06% YoY) is provided below:

Overall annual mortgage growth has tanked to an all-time low, with especially sharp falls in investor credit growth:

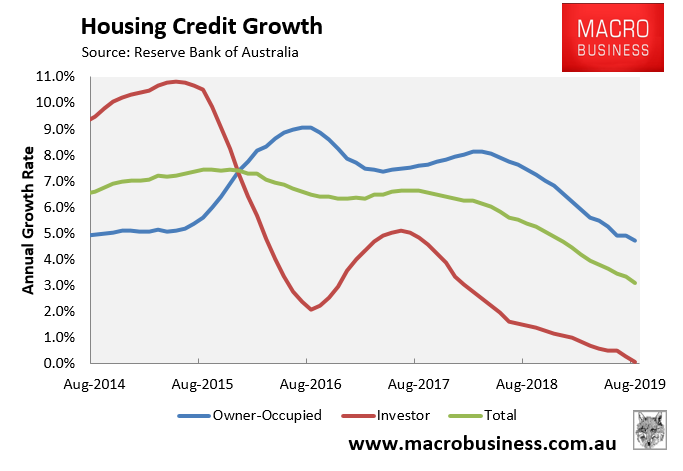

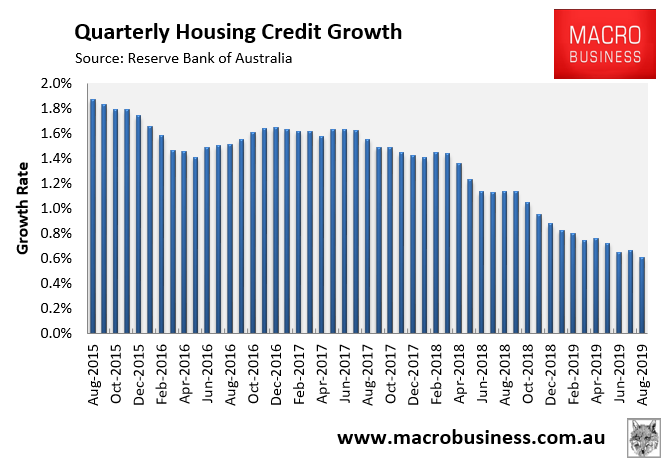

The below chart shows that quarterly mortgage growth also fell to the lowest on record in August:

Driven by investors:

This is a weird result given the boom in house prices. More on this tomorrow.