China is going ex-growth. The August monthly data dump is unequivocal. Industrial production slumped to the lowest year dot at 4.4%, fixed asset investment is slowing too at 5.5% and retail is tracking both down at 7.5%:

The trends are rock solid down.

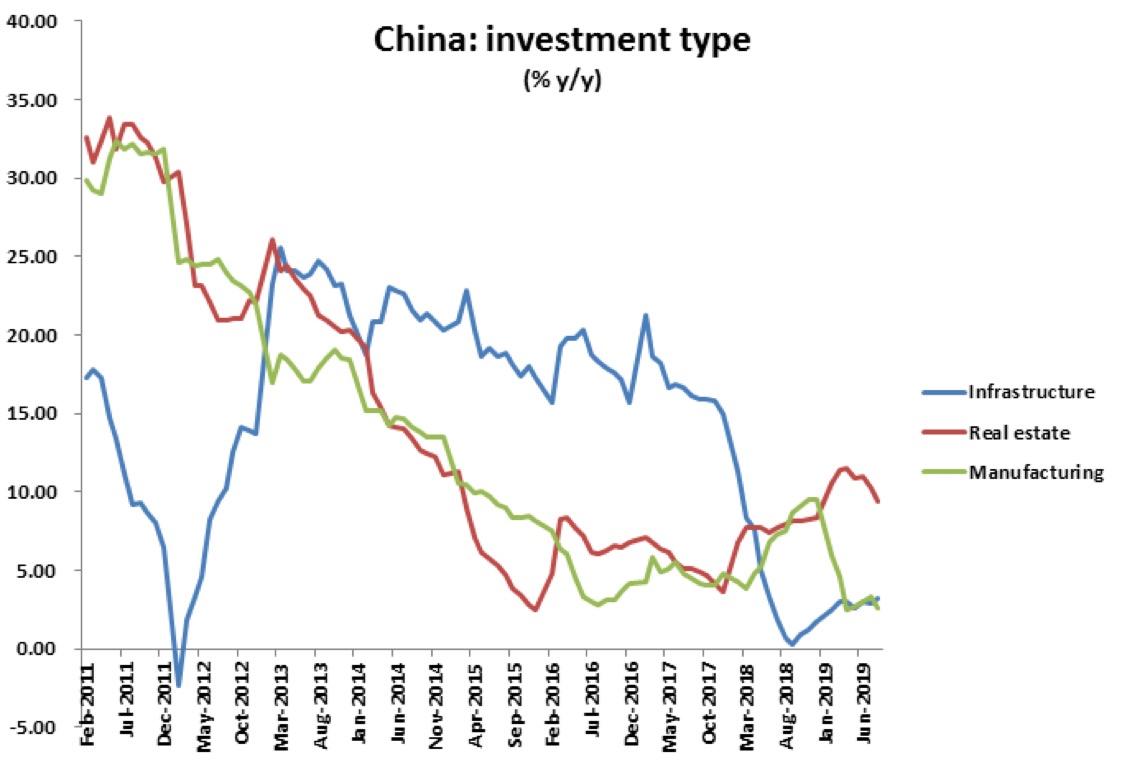

Under the bonnet the news is also bad for the growth mix. While industry is being put to the sword by the trade war, the offset of fixed asset investment continues an ever increasing imbalance of unproductive debt wasted on pointless construction:

Advertisement