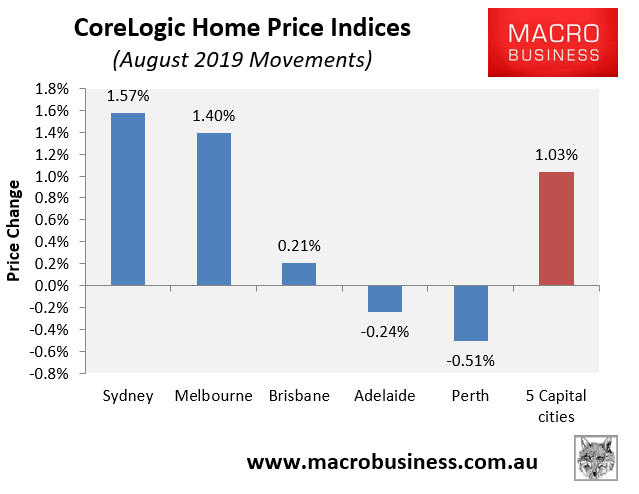

CoreLogic’s dwelling price results have been released for August, which reveals a strong 1.0% increase in values recorded over the month at the 5-city level, driven by surging values across Sydney (1.6%) and Melbourne (1.4%):

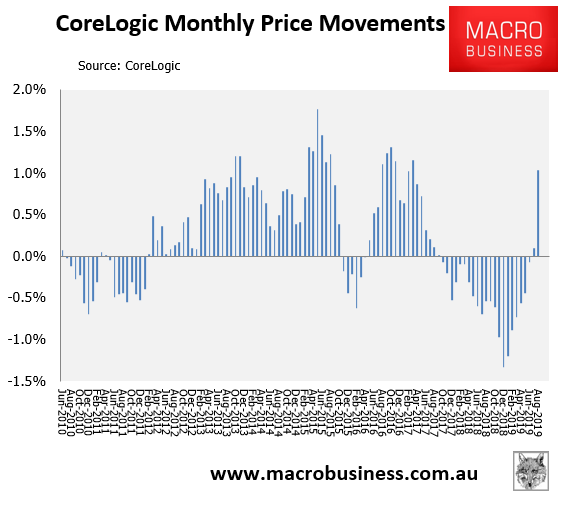

It was the second consecutive monthly rise in home values at the 5-city level, which follows a run of losses extending back to August 2017:

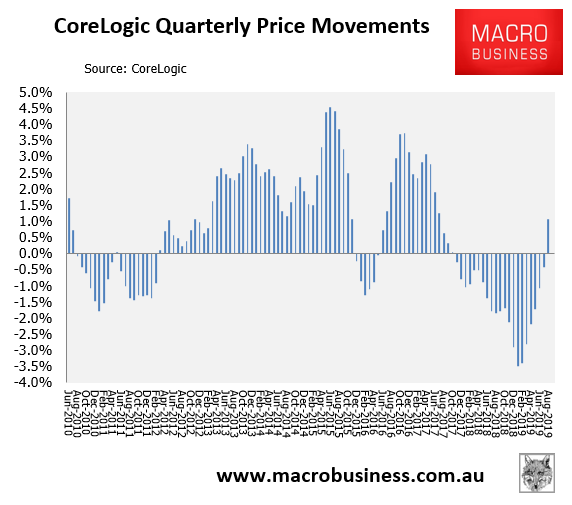

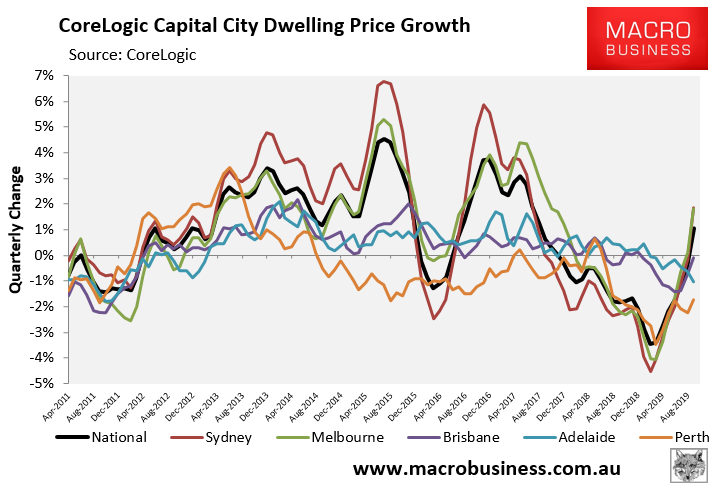

Over the August quarter, dwelling values rose by 1.1% across the major capitals, the first quarterly rise since October 2017:

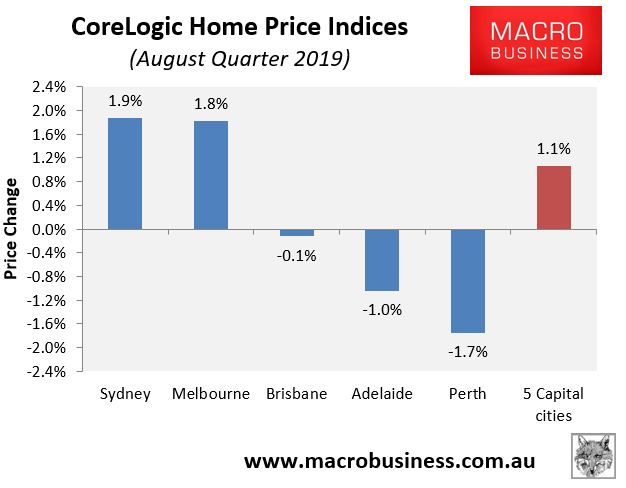

Over the August quarter, values surged across Sydney and Melbourne, but fell across the other major capitals:

The next chart plots quarterly price growth by major capital, which illustrates the massive lift across Sydney and Melbourne, as well as the improvement in Perth:

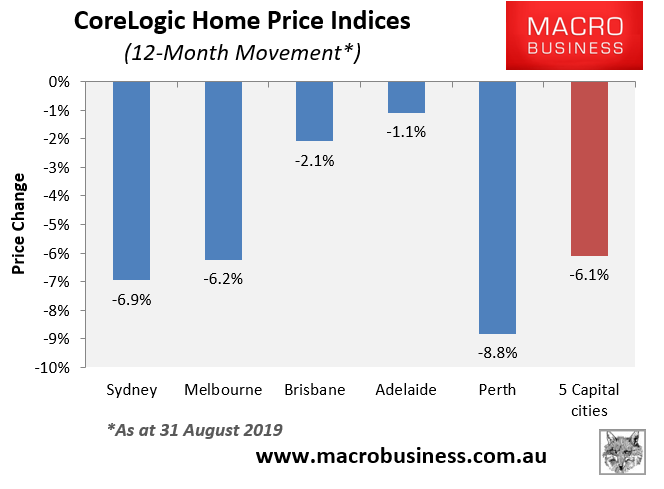

In the year to August 2019, home values have fallen by 6.1% at the 5-city level, driven by Sydney (-6.9%), Melbourne (-6.2%) and Perth (-8.8%):

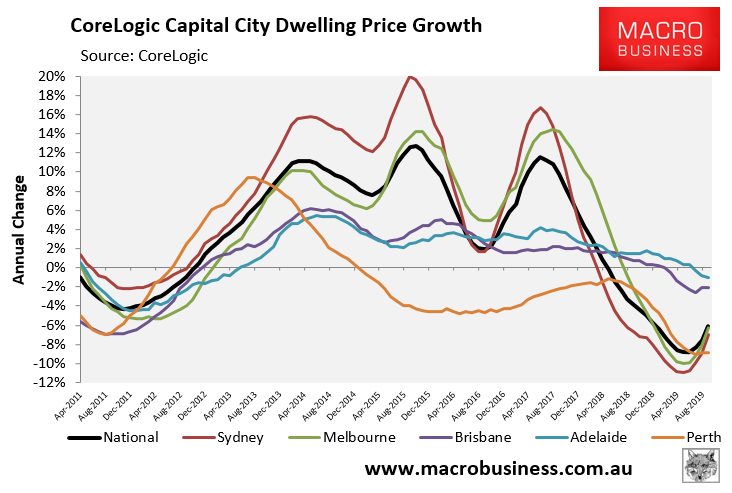

However, the next chart, which tracks trend annual price growth, shows a strong rebound led by Sydney and Melbourne:

The housing market has clearly turned, led by Sydney and Melbourne where auction clearance rates have rebounded strongly:

How long the rebound persists is now the big question mark.