Rising mortgage debt to crush Australian pension

Data from the Australian Housing & Urban Research Institute (AHURI) shows that the proportion of homeowners aged 55+ with a mortgage rose from 14% in 1987 to 28% in 2015. Professor Rachel Ong Viforj from Curtin University, who led the AHRI’s research, says governments need to be prepared for the likelihood that an increasing number of older Australians will not be able to keep up their mortgage payments and will be forced into the rental market. And this will place acute pressure on Australia’s retirement system. From The AFR:

Average real mortgage debt among older Australians soared 600 per cent from $27,000 to over $185,000, while their average mortgage debt-to-income ratios tripled from 71 to 211 per cent over the same period.

This blow-out – made worse by the practice many people had of redrawing equity on their home loans and extending the length of their loans – would not just carry consequences for the mental health and wellbeing of older people who would have to bear the pressure of debt later in life…

“The likelihood of falling out of home ownership is going to be higher from older people in the future,” said Prof Ong ViforJ…

In addition, high mortgage debt poses a further risk as many among older people would spend their superannuation to pay off their housing debt, leaving them with insufficient funds to live off, Prof Ong VitorJ said.

Higher numbers of older people falling out of home ownership will also add to the demand on federal coffers for Commonwealth Rent Assistance, the report says.

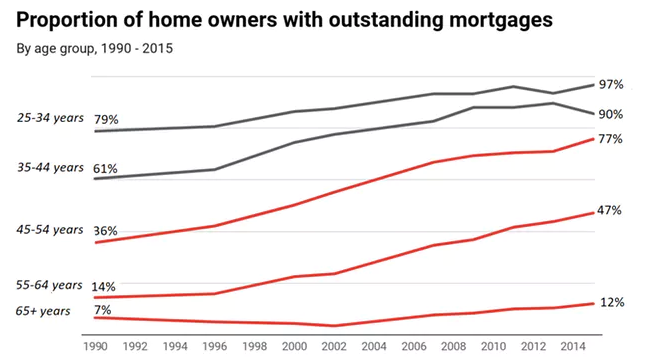

The below charts tell the story.

For home owners aged 55 to 64 years, the proportion owing money on mortgages has tripled from 14% to 47%:

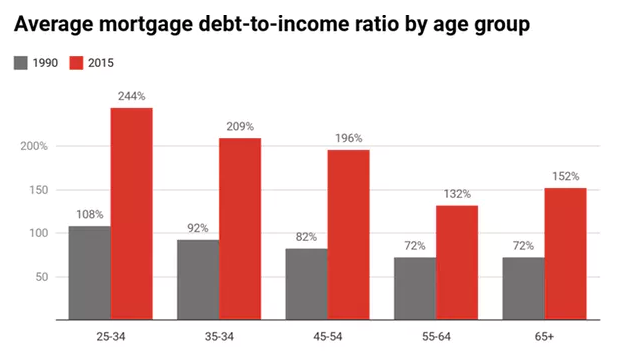

Whereas the average mortgage debt-to-income ratio among those with mortgages has roughly doubled across every home-owning age group:

The Grattan Institute has similarly warned that crashing home ownership rates will place acute pressure on Australia’s retirement system and could send government spending on housing assistance soaring:

…new Grattan Institute modelling shows the share of over 65s who own their home will fall from 76% today to 57% by 2056 – and it’s likely that less than half of low-income retirees will own their homes in future, down from more than 70% today…

Today’s younger Australians will become tomorrow’s retirees.

Worsening housing affordability means renting will become more widespread among retirees. As a result, more retirees will be at risk of poverty and financial stress, particularly if rent assistance does not keep pace with future increases in rents paid by low-income renters.

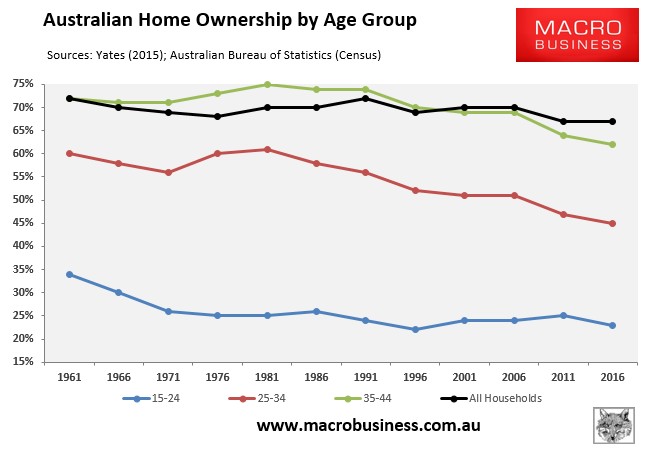

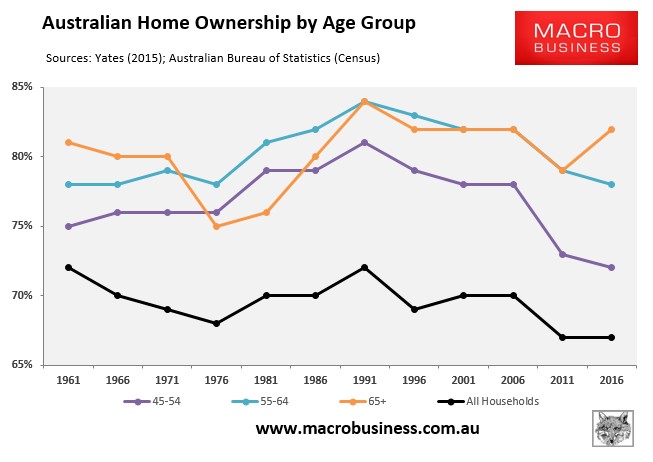

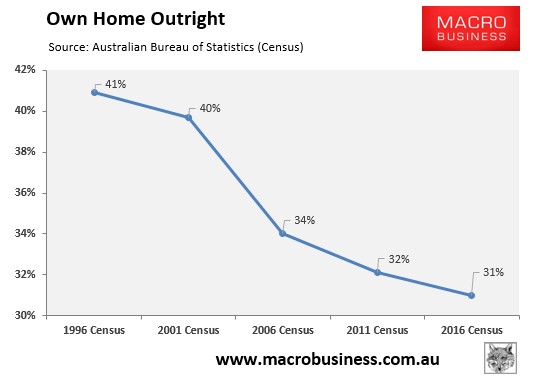

The 2016 Census highlighted in all its hideous glory the collapse in home ownership, especially among younger Australians:

As well as the collapse in the proportion of households that own their homes outright, from 41% in 1996 to 31% as at the 2016 Census:

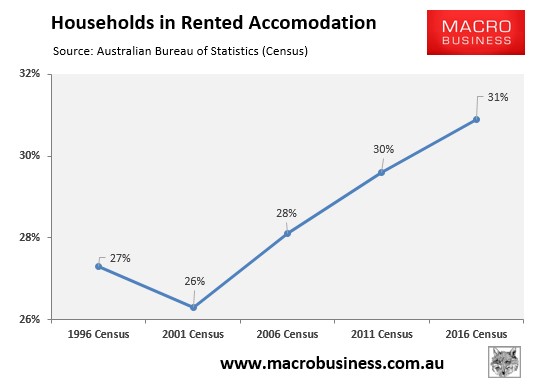

As expected, the decline in home ownership has been met with an increase in households in rental accommodation, which has increased from 27% in 1999 to 31% as at the 2016 Census:

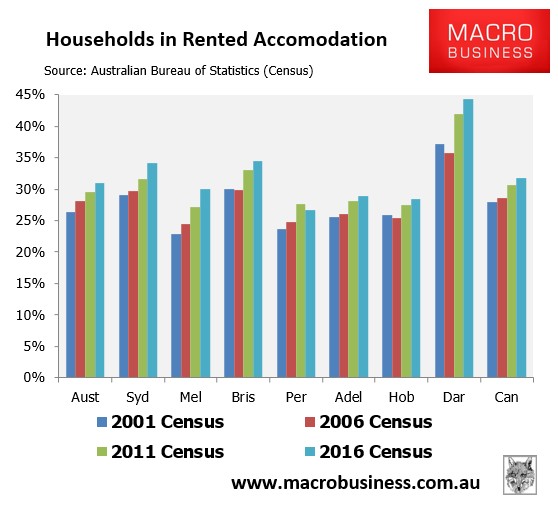

The growth in rented accommodation has also been broad-based, with all jurisdiction experiencing large increases since 2001:

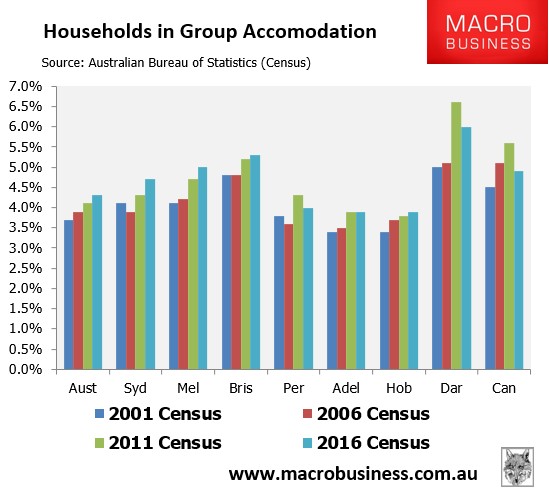

In a similar vein, the percentage of households in group accommodation – defined as one that consists of two or more unrelated people, where all residents are 15 or over – has increased across all jurisdictions and nationally since 2001:

Australia’s current retirement system is based on the assumption that most people will own their homes. But that assumption is running face first into rising debt levels and falling rates of home ownership.

In addition to lowering the system-wide cost of housing through a combination of reforms, the Aged Pension system needs to be transformed to make it more neutral between owning a home and renting.

The solution I have espoused many times is to:

- Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Raise the overall pension asset test threshold as well as the base rate.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HECS-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under such a plan, asset rich pensioners choosing to remain in place could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. But they would similarly be incentivised to move as the family home would no longer be viewed as a tax free shelter. Renting pensioners would also be made significantly better-off via the combination of a higher asset test threshold and a higher pension base rate.

The May 2018 Budget addressed the third point by extending the Pension Loans Scheme, but it did not touch the other two areas, which is vital if the system is to be made more neutral towards home owner retirees and renting retirees.

One wonders how long this issue can continue to be ignored given the collapse in home ownership and the rise in renters.