Michelle Grattan has penned a spurious article claiming that raising the compulsory superannuation guarantee from the current 9.5% to 12% is essential to ensure adequate savings in retirement as well as to save the federal budget future Aged Pension costs:

The temptation for scrapping the rise, or having some “opt-out” system, becomes stronger when wages are flat — a problem reinforced by the latest figures this week.

But there is a strong counter case that such a course would be bad in practical and policy terms.

There’s no certainty workers would actually get the extra money, or all of it, in wage increases. Attempting to compel that would be complex and fraught.

More importantly, failure to strengthen further the compulsory system would disadvantage many individual retirees in the future and be an added burden on a later generation of taxpayers, as more people would be pushed onto full aged pensions…

Admittedly, the argument for workers having immediate access to their money, at a time of life when they face their most severe cost-of-living pressures, is seductive. But it is short-term thinking from the points of view of both individuals and governments.

Much of the debate is being conducted around modelling, stretching out decades, calculating the competing financial implications for low-income workers. But modelling, with its assumptions, carries a degree of false precision. It also represents one-dimensional thinking.

People on low incomes are naturally going to spend any extra money rather than save it. Yet for these people savings are what they need for the long term. This applies especially for women, for whom more, not fewer, ways should be found to augment their superannuation.

Forced saving might be unpleasant at the moment, but valued at the time of a more comfortable and secure retirement. Promises of the money being used for wage increases carry political appeal for a government now, but future governments would benefit if the aged pension burden is contained by a healthily growing compulsory super scheme.

Earth to Michelle Grattan: raising the superannuation guarantee will cost the federal budget more than it saves in Aged Pension costs. This was made clear by the Henry Tax Review, which explicitly stated:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

Advertisement

Accordingly, the Henry Tax Review explicitly recommended against raising the superannuation guarantee, also because it would lower workers’ take home pay and have a particularly adverse impact on lower-income earners:

“Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners”.

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

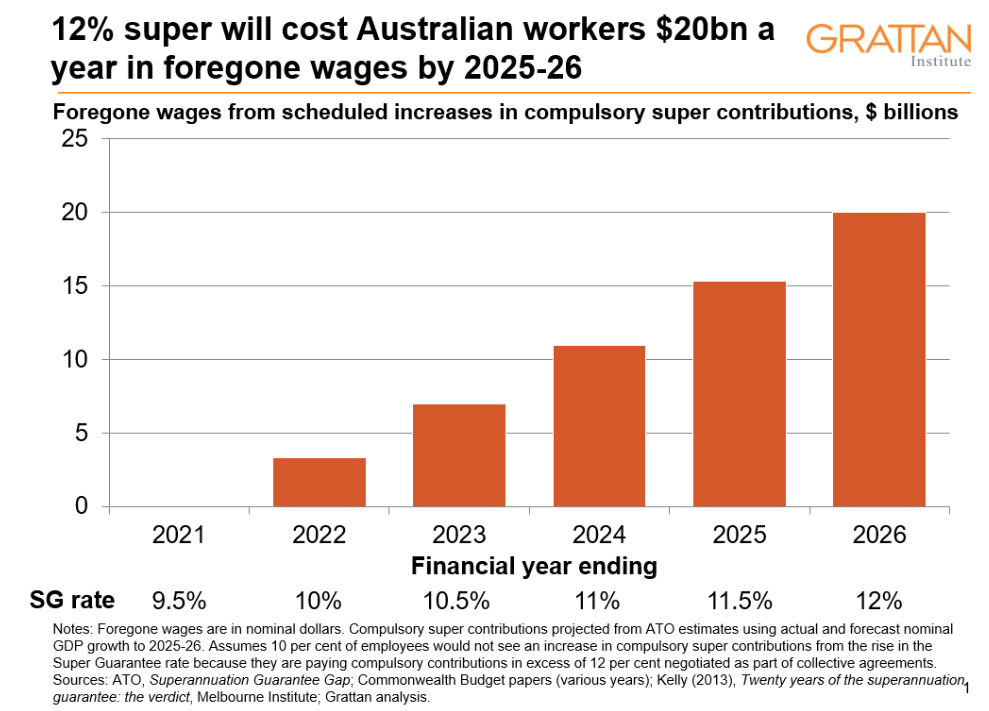

If compulsory super contributions go up, wages will be lower than they otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP…

[Moreover] both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

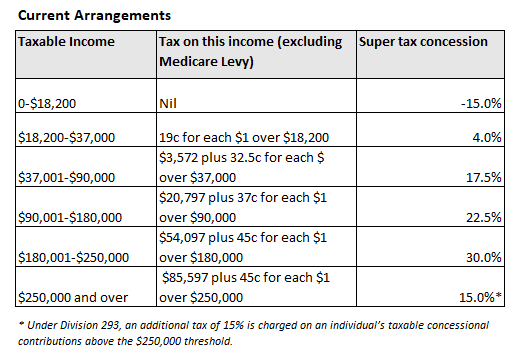

The reason why raising the superannuation guarantee would be so ineffective can be explained by Australia’s flat 15% tax on contributions and earnings. This ensures that those workers on lower incomes receive minimal concessions (or are penalised), whereas those on higher incomes receive the biggest tax concessions on contributions:

Advertisement

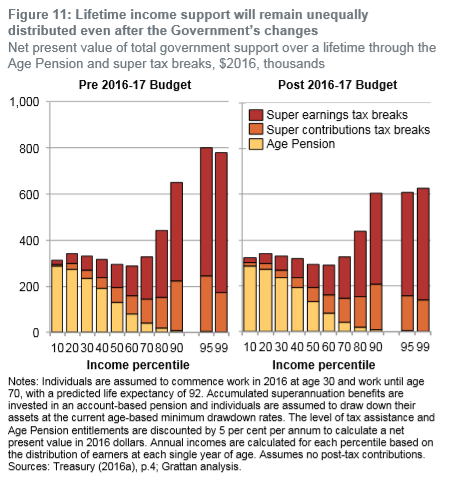

Division 293 remedies the situation for those very high income earners above $250,000. But even then, the lion’s share of superannuation concessions still flow to the highest income earners, whereas the lower income earners continue to be disadvantaged by the system:

Michelle Grattan needs to face up to the facts. Tax concessions on superannuation already cost the Budget an inordinate sum, and are growing rapidly. Raising the superannuation guarantee to 12% would mean they become an even bigger ($2 billion a year) Budget drain over time.

Advertisement

Meanwhile, it would do little to boost superannuation savings for lower income workers – those most likely to become reliant on the Aged Pension – given the lion’s share of superannuation concessions would flow to higher income earners.

Raising the superannuation guarantee would merely heighten inequities already present in the system. It would rob younger (and lower paid) workers of much-needed disposable income and worsen the long-term sustainability of the Budget.

About the only winners from such a policy would be the superannuation industry, which would get to ‘clip the ticket’ on more funds under management and earn fatter profits.

Advertisement

Instead of raising the compulsory superannuation guarantee, both equity and Budget sustainability would be improved by replacing the 15% flat tax on contributions/earnings with a flat-rate refundable tax offset (e.g. 15%). This way, everyone that contributes to superannuation would receive the same tax concession, the system would be made progressive, and lower income earners would get a better deal.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.