Industry Super Australia bigwig and former union strongman, Greg Combet, has warned of an advertising blitz if the federal government tries to abandon plans to raise the superannuation guarantee (compulsory super) from the current level of 9.5% to 12%. From The Brisbane Times:

Mr Combet is the chairman of Industry Super Australia, the lobby group for super funds, and its investment management arm IFM Investors. As such he is considered one of the most influential people in the nation’s financial services industry…

[Combet] said any attempt to overturn the rise in the superannuation guarantee would be “appalling” and that Industry Super Australia was “looking into” an advertising campaign to that effect.

“Retirement savings growth has been the greatest mitigant of wealth inequality in our country in the last quarter of a century,” Mr Combet said.“And once the parliament has legislated this – to reverse that would be a big deal. We would not support it” he said…

“If we stop it now, for a 30 year old on about $85,000 a year will be done out of about $150,000 by the time they retire. And I don’t think they’ll appreciate it”…

“Labor are 100 per cent committed to raising the super guarantee”

Greg Combet’s claim that “retirement savings growth has been the greatest mitigant of wealth inequality in our country” is complete bunkum. If anything, superannuation has increased inequality.

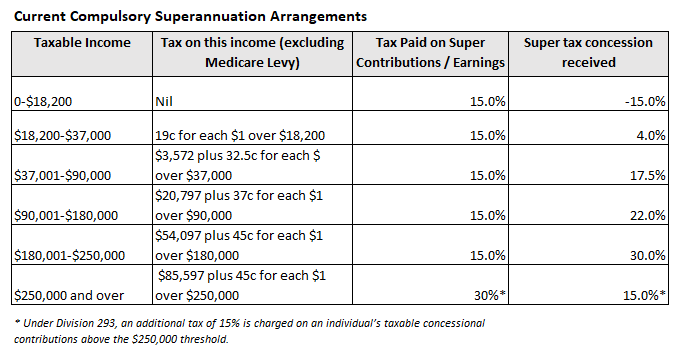

The reason is simple: the 15% flat tax on superannuation contributions and earnings ensures that those on higher incomes receive larger tax concessions, whereas those on lower incomes receive few tax concessions or are penalised. The below table illustrates this state of affairs clearly:

It is true that Division 293 of the Tax Act mitigates this inequity for very high income earners – i.e. those earning over $250,000 per year – by lowering their superannuation tax concessions to 15%. But even then, the retirement system remains far more generous to higher income earners than lower income earners, thanks to the inequitable distribution of superannuation tax concessions on contributions and earnings:

There is also the important issue of wages. Wage growth in Australia has been anaemic for many years and the superannuation guarantee is paid for by workers through lower take-home pay.

Thus, raising the superannuation guarantee would lower workers’ disposable incomes, whilst also worsening the present inequities already present in the superannuation system – a highly undesirable outcome.

For these reasons the Henry Tax Review explicitly recommended against raising the superannuation guarantee:

“Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners”.

The Henry Tax review also warned that a higher superannuation guarantee would have a negative impact on the federal budget, since the cost of concessions would outweigh any benefits flowing from a lower Aged Pension bill:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

The Grattan Institute has come to the same conclusions and has also recommended against lifting the superannuation guarantee:

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

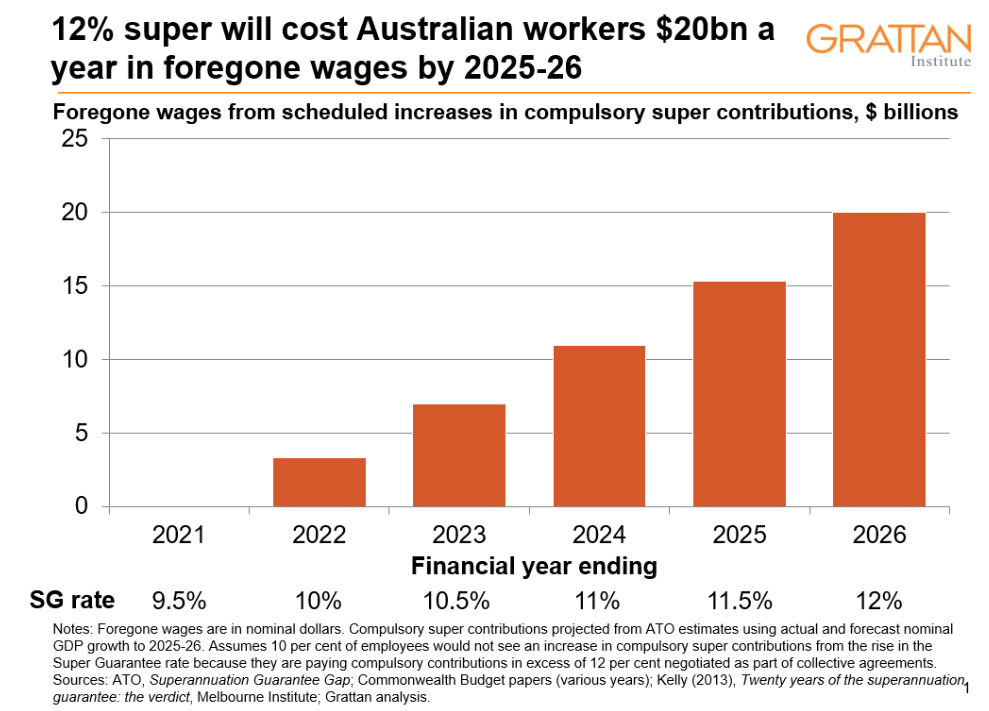

If compulsory super contributions go up, wages will be lower than they would otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP…

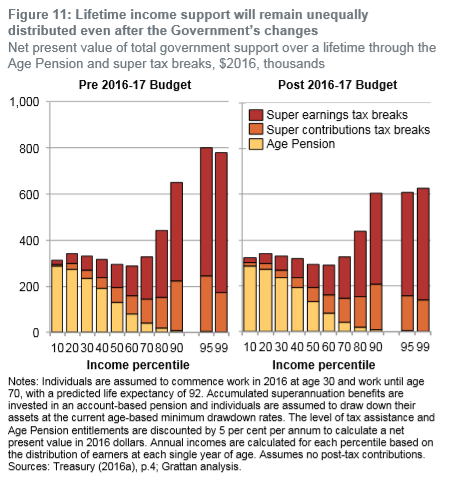

[Moreover] both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

If Greg Combet was genuinely concerned about improving equality and outcomes for Australian workers, he would abandon increasing the superannuation guarantee in favour of making the concession system progressive.

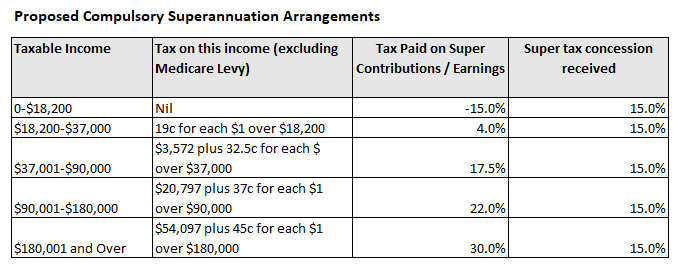

This could be done by replacing the 15% flat tax on contributions and earnings with a 15% concession that is subtracted from one’s marginal tax rate. The below table illustrates how this concession scheme would work:

Under this reform, everybody that contributes to superannuation would receive the same tax concession (15%), the system would be made progressive, and lower income earners would get a better deal.

But lifting the superannuation guarantee in isolation – as espoused by the industry and Labor – would simply heighten inequities already present across the system. It would rob younger (and lower paid) workers of much-needed disposable income and worsen the long-term sustainability of the Budget.

About the only winners from such a policy would be the superannuation industry rent-seekers like Greg Combet’s Industry Super Australia and IFM Investors, which would ‘clip the ticket’ on more funds under management and earn even fatter fees.

For an ex-union guy that is supposed to care about the welfare of Australian workers and equality, Greg Combet has clearly sold-out.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.