DXY broke out last night and is running. EUR was smashed:

The Australian dollar was crushed to post-GFC lows across the board:

Advertisement

Gold held on:

Oil too:

Advertisement

Metals were mixed:

Miners hammered:

EM stocks belted:

Advertisement

High yield was mixed:

The Treasury curve collapsed:

And bunds:

Advertisement

Aussie bonds rampaged on:

Stocks hated it:

US data was OK too with the ADP rebounding:

Advertisement

Private sector employment increased by 156,000 jobs from June to July according to the July ADP National Employment Report®. … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

…“While we still see strength in the labor market, it has shown signs of weakening,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “A moderation in growth is expected as the labor market tightens further.”

Mark Zandi, chief economist of Moody’s Analytics, said, “Job growth is healthy, but steadily slowing. Small businesses are suffering the brunt of the slowdown. Hampering job growth are labor shortages, layoffs at bricks-and-mortar retailers, and fallout from weaker global trade.”

However, the Chicago PMI gave a bad lead on the ISM:

The Chicago Business BarometerTM, produced with MNI, eased further to 44.4 in July from 49.7 last month, the second sub-50 reading in 30 months.

The weakness in the Barometer observed in Q2 continued into the current quarter, with the latest outturn making it the weakest start to Q3 since 2009.

…This month’s special question asked firms about their views on the US economy’s growth in the second half of the year. Two in five firms expected the economy to see slower growth than currently, with some holding tariffs responsible for the slowdown. The majority, at 46%, did not expect any change while only 14% expected the economy pick up.

“Sentiment faded further with firms facing weakness across the board. Global risks, trade tensions, slowdown in demand and sombre growth expectations, all jeopardize business conditions. Firms are not panicking yet, but the latest report isn’t adding to the cheer. The above risks lend weight to a monetary easing approach by the Fed, albeit a gradual one,” said Shaily Mittal, Senior Economist at MNI.

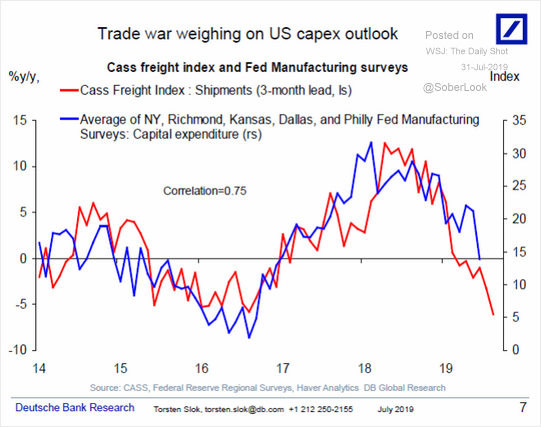

There is no doubt that the industrial economy is slowing:

Advertisement

It’s all about the consumer now.

The dovish Fed cut 25bps to support her but it just can’t get dovish enough for reflated markets:

Information received since the Federal Open Market Committee met in June indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although growth of household spending has picked up from earlier in the year, growth of business fixed investment has been soft. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 2 to 2-1/4 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. As the Committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

The Committee will conclude the reduction of its aggregate securities holdings in the System Open Market Account in August, two months earlier than previously indicated. Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; James Bullard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against the action were Esther L. George and Eric S. Rosengren, who preferred at this meeting to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent.

Advertisement

The Q&A was worse for markets, espeically this:

“What we’re seeing is that it’s appropriate to adjust policy to a somewhat more accommodative policy over time,” Mr. Powell says, adding “it’s not a long cutting cycle,” as is common in a recession.

Time to remind the Fed who’s boss.

The Australian dollar is on a hiding to nothing right now:

US outperformance and a slow moving Fed;

European recession and aggressive ECB by necessity;

troubled China on trade war and Hong Kong plus falling bulk commodities ahead;

weak Australia on the construction bust leading to more RBA cuts and unconventional policy that has already begun.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.