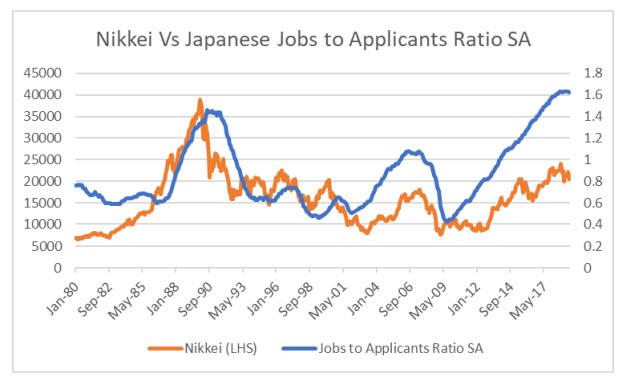

Japan pioneered many of the monetary policies that we now find common in the Western world. Despite the Bank of Japan (“BOJ”) taking monetary policies to ever more extreme levels, including negative interest rates and very large purchases of Japanese government bonds, the Nikkei still languishes well below the all-time highs set in 1989. Despite the BOJ’s best efforts, the Nikkei still has a tendency to move with employment.

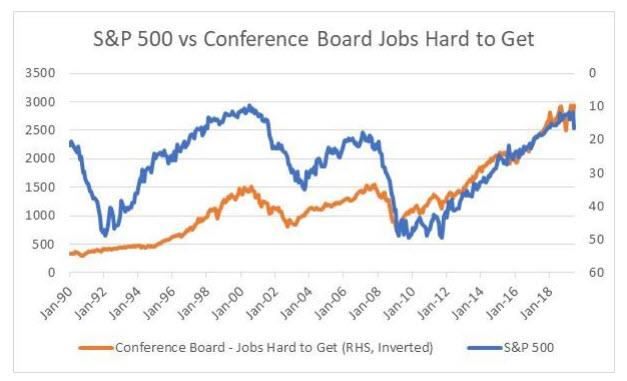

Since the bursting of the dot com bubble, US Equities seem to also follow the Japanese tendency of equities and employment. The below table shows the S&P 500 Index vs the Conference Board Employment Trends Index/Conference Board Consumer Confidence Survey which shows the number of unemployed in the US/percentage of survey respondents who say they find “jobs hard to get.”

Advertisement

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.