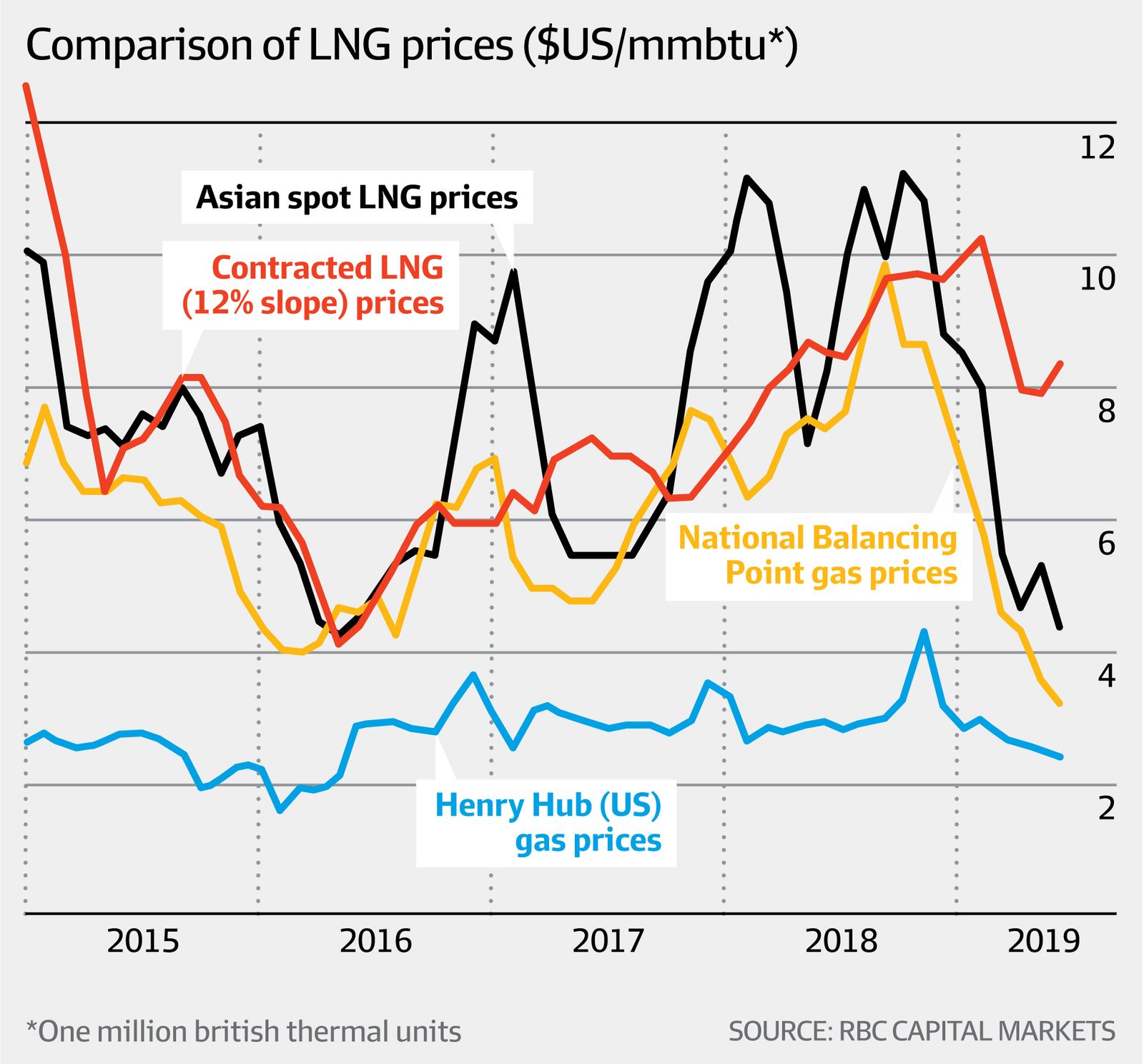

Evidence has grown in past weeks that customers in the top-tier markets of Japan and South Korea are prepared to act more aggressively than ever before in price review negotiations to reduce the large disconnect between their crude oil-based contract prices and the rock-bottom spot LNG price.

…The world’s biggest LNG buyer, Korea Gas Corporation, is already in arbitration with the North West Shelf venture in a bid to resolve a pricing dispute over an expired contract, with a decision expected in about three months.

Meanwhile, Osaka Gas is said by one source to have entered an arbitration process with ExxonMobil-led PNG LNG, the first time ever for a Japanese player to take such a step, having always in the past relied on negotiating an agreement.

That is European, US and Asian gas prices all collapsing. There are literally full LNG tankers bouncing back and forth between them at the moment unable to unload into brimming inventories and soft demand.

In the past I have called this the LNG “contractpocalypse”. It has already led to serious renegotiations on contracts over years:

Advertisement

Edison renegotiated RasGas contract on price and volume in 2012;

PGNiG renegotiated QatarGas contract on volume in 2014;

Petronet renegotiated RasGas contract on volume and price in 2015;

PetroChina renegotiated QatarGas contract on volumes in 2015;

JERA renegotiated RasGas contract on volume and price in 2016;

Pakistan renegotiated QatarGas contract on volume sand price in 2016;

Japan declares multiple contracts illegal owing to “destination clauses” in 2016, following Europe from a few years earlier;

Petronet renegotiated Exxon-Mobil Gorgon contract on volume and price in 2017;

Woodside Pluto contracts renegotiated on price in 2017;

Kogas renegotiated Woodside contract on price in 2018;

GAIL renegotiated Gazprom contract on volume and price in 2018;

India in talks with Cheniere and Dominion to renegotiate contracts in 2018.

Now another round will commence. It is my view that within a few years, the oil-linkage will be consigned to history for new projects and steadily run off as spot prices dominate the industry. There is no end in sight for the glut for as far as the eye can see:

Advertisement

Why anyone ever thought there’d be a shortage in the 2020s I will never know.

Meanwhile, back home, there is even evidence that the outrageous east coast gouge may be breaking. Spot prices hit the lowest prices in 2019 Friday as the tougher ADGSM looms:

Advertisement

But that is only 5% of the market. The proof will be in the pudding of the contract market which will also have to fall to $7Gj from its average around $10Gj in recent years.

As gas contracts break down worldwide towards glutted and cheap spot markets, there is no excuse for them to stay high in Australia.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.