US private payrolls rebounded in the June ADP jobs report, albeit to a still mildly disappointing +102k. The service sector ISM fell more than expected in June, to 55.1 from 56.9, a two-year low, though both the new orders and employment sub-indices remain comfortably above 50. The US May trade balance widened more than expected, to $55.5bn from $51.2bn and factory orders were revised down to show a steeper 0.7% fall in May.

The majority of Eurozone and periphery service PMI’s beat, admittedly low, estimates and so provided a more stable profile for the Final June service and composite PMI’s. However, Markit’s commentary and assessment remains decidedly negative. They project regional 2Q GDP of +0.2%q/q with downside risks ahead suggesting that ECB ought to provide further accommodation.

EC dropped the potential of disciplinary action against Italy with respect to fiscal responsibility over their 2019 budget.

UK’s June CIPS/Markit PMI at 50.2 missed estimates (unchanged at 51.0) and dragged the composite PMI to 49.7 and so in technical contraction. Brexit uncertainty remains a key obstacle for business optimism.

Event Outlook

Australia: May retail sales are expected to rise 0.2% (Westpac +0.1%) with conditions looking to have remained soft during the period.

Euro Area: May real retail sales are anticipated to show the annual pace edge up to 1.6%yr from 1.5%yr.

US: It is the Independence Day public holiday, markets are closed.

There are any number of factors we can point to explain the Aussie dollar strength overnight: soft US data; easing trade war fears; tearaway iron ore prices; ScoMo’s tax cuts getting up. But the truth is it just jumped with other risk currencies as global stocks pour on the buying.

Advertisement

The driver sure isn’t growth. Following the awful manufacturing PMIs worldwide we got lackluster services, via JPM:

The performance of the global service sector remained sluggish in June. Despite uplifts in the rates of expansion of business activity and new orders, growth of both was among the weakest since late-2016. Business optimism was also relatively downbeat, falling to a three-year low and its second-lowest level in the series history. The J.P.Morgan Global Services Business Activity Index – a composite index produced by J.P.Morgan and IHS Markit in association with ISM and IFPSM – was at 51.9 in June, up slightly from May’s 33-month low of 51.6. The strongest rate of output expansion was registered in the financial services sector, followed closely by consumer services, with both seeing mild growth accelerations. The increase in activity at business service providers was comparatively subdued, matching May’s 32-month low growth rate. Ten of the 13 nations for which June services PMI data were available recorded an increase in output. The exceptions were Brazil, India and Russia. Brazil saw its rate of decline ease, whereas India and Russia both fell into contraction following periods of growth. The strongest performers – Ireland, Spain, Germany and France – were all based in Europe. Japan, China and Australia also registered growth at, or above, the global average. Expansions were also seen in the US, the UK and Italy.

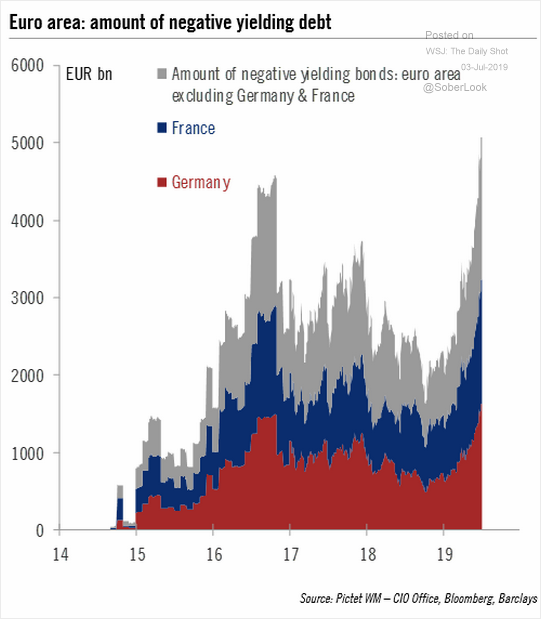

The real driver of the global stocks surge is global bond yields which just can’t find a bottom. US yields keep falling as growth slows. But Europe was just as bond bullish on the news that dovish Christine Lagarde will take the helm at the ECB. Indeed, it is all so heated in European bond markets that even the Italian short end inverted negative:

Advertisement

This is a fascistic state, openly hostile to the Europe and its currency, in the process of developing a parallel bond market and currency, with the sole purpose of defaulting on its debt, and you have to pay it to take your money. Risk has become meaningless as yields crash.

Another chart:

Advertisement

The only reason that stocks are thundering higher is that there is no yield left anywhere. While that happens, the Australian dollar just catches the thermal.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.