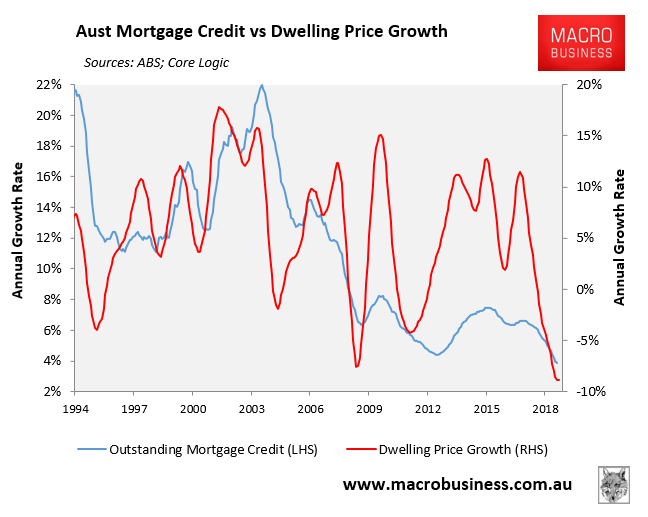

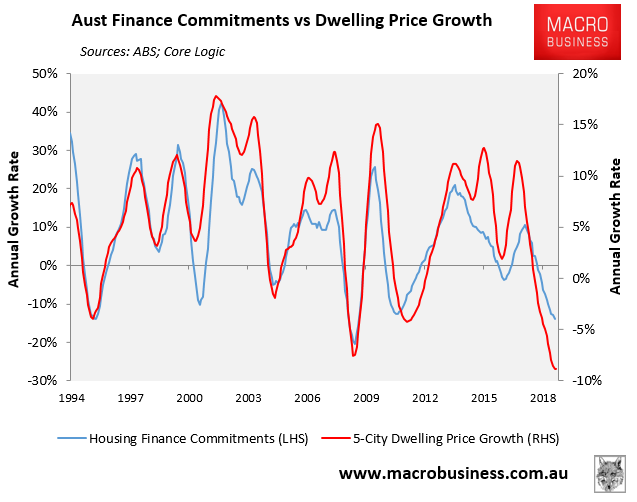

Following yesterday’s post charting Australia’s housing finance data against house prices across Australia’s major capitals, below is a chart comparing mortgage credit growth – as reported monthly by the RBA – against dwelling values nationally, since I frequently get requests for this from readers:

As you can see, unlike the ABS’ housing finance series (shown below), there is a weak correlation between the growth in outstanding mortgage credit and house prices.

Advertisement