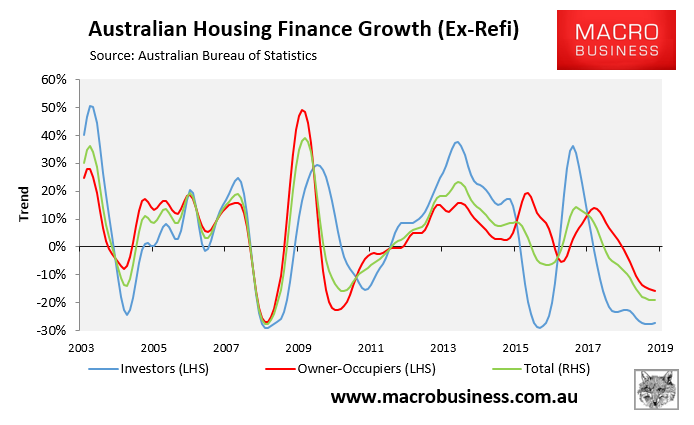

Friday’s Lending to households and businesses release from the ABS revealed that total mortgage lending (excluding refinancings) stabilised in April, but have tanked by 19% over the year in trend terms, driven by an epic 27% crash in investor commitments, whereas owner-occupied commitments also fell by 16%:

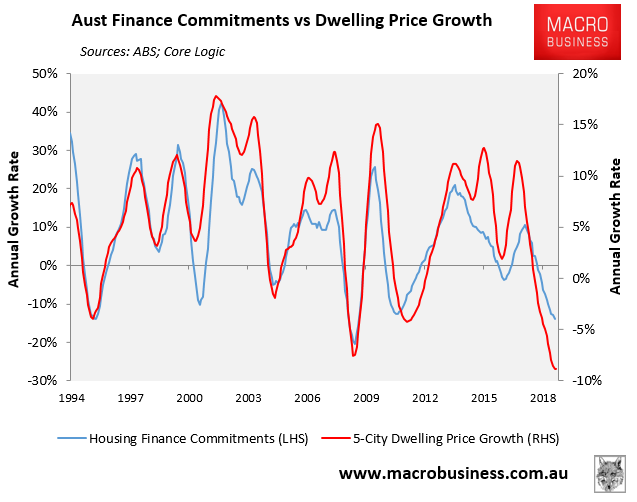

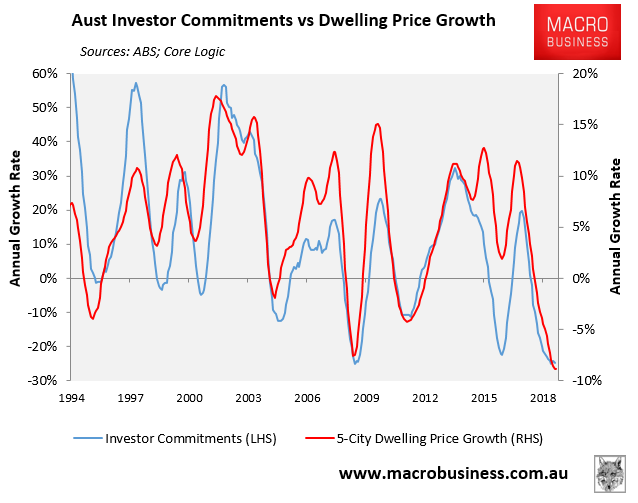

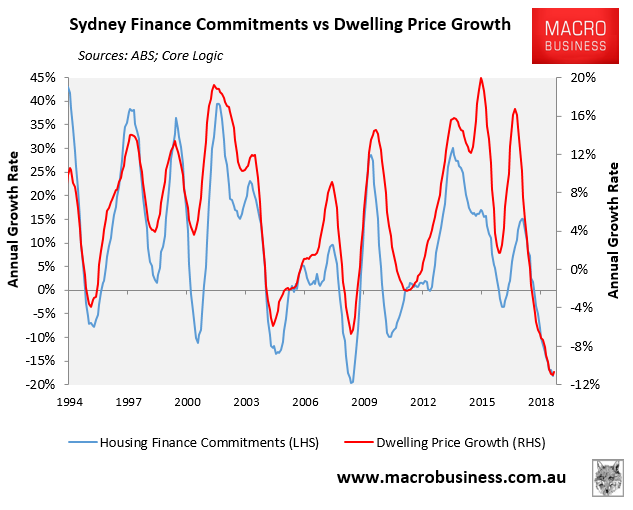

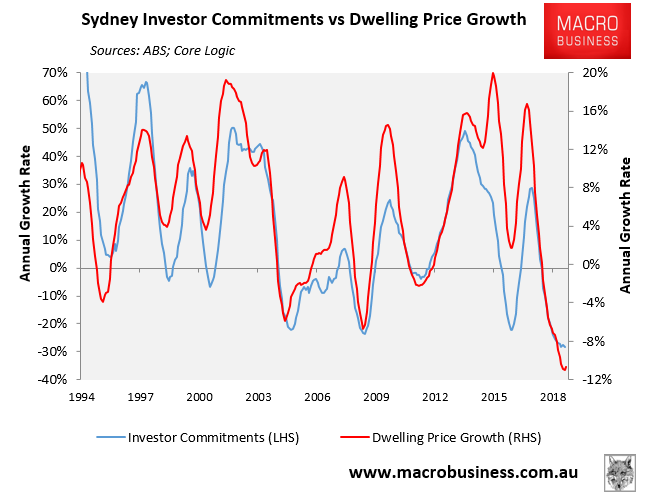

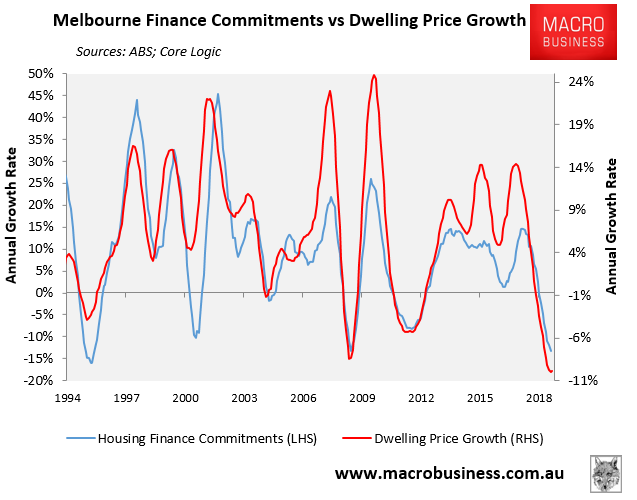

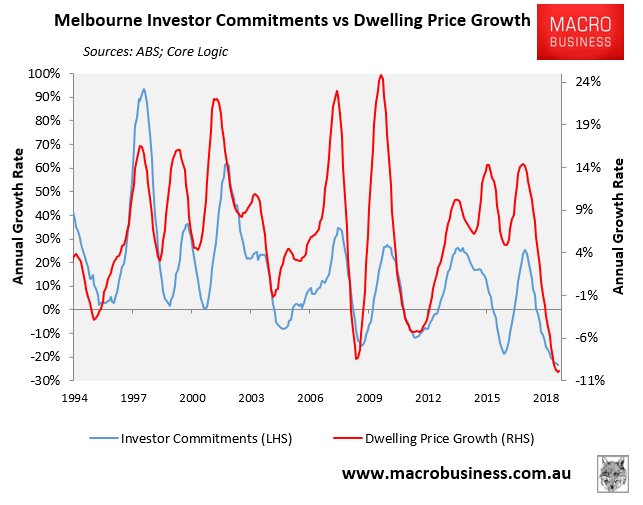

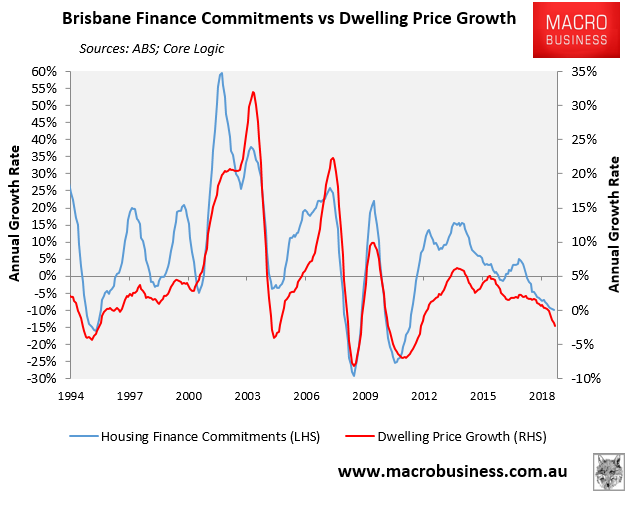

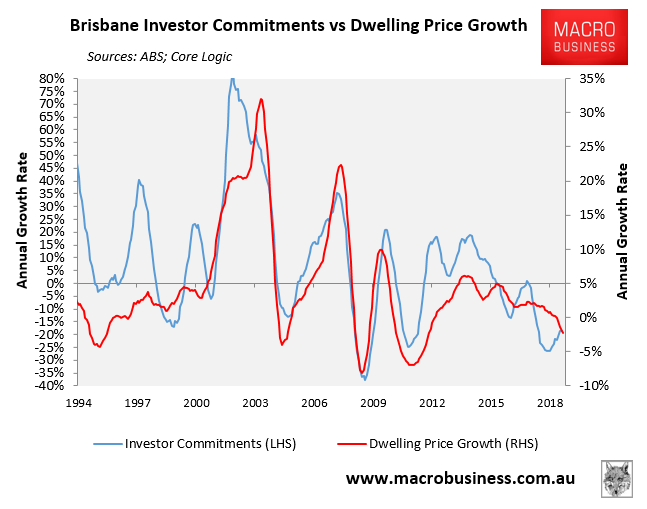

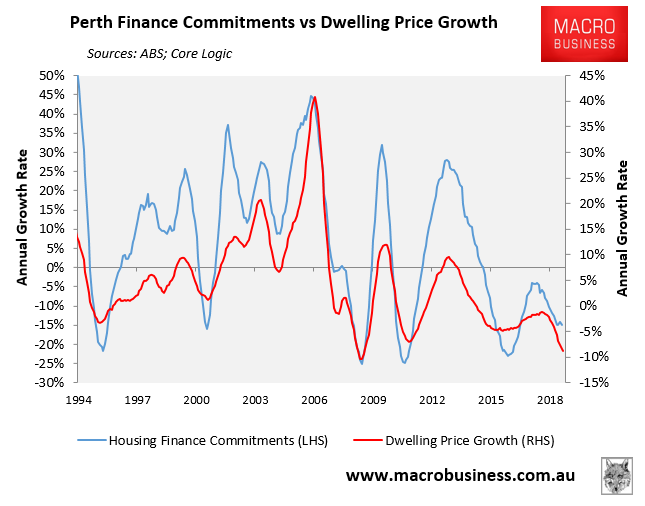

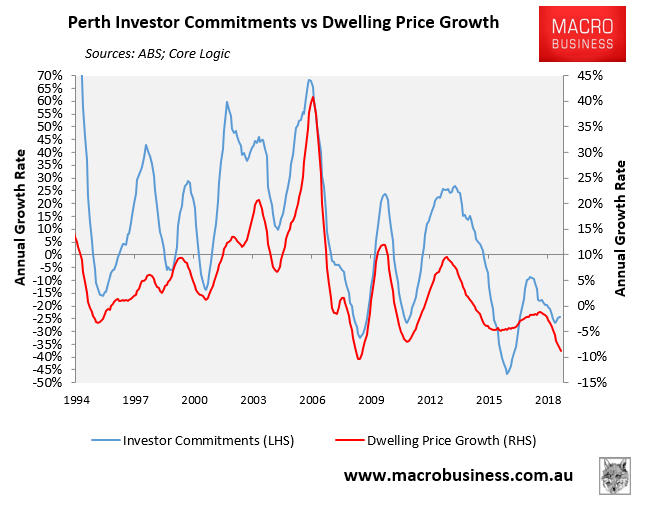

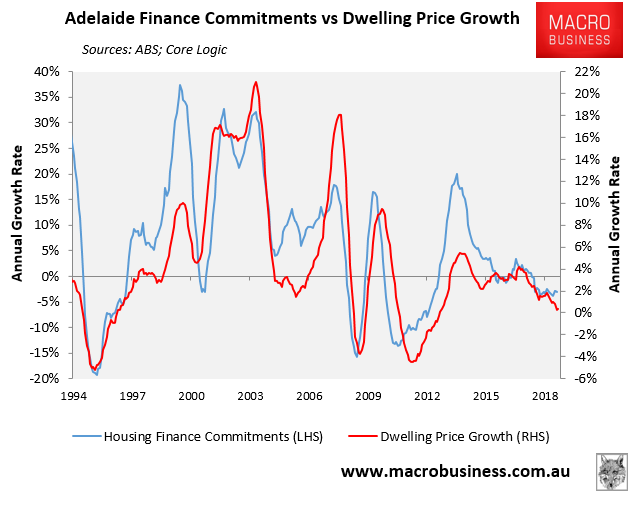

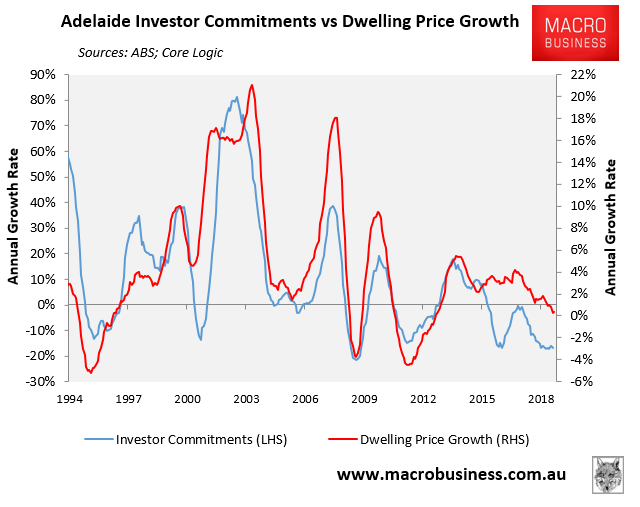

As regular readers of MB will know, we consider the flow of housing and investor finance commitments to be premier indicators for dwelling value growth. This view is based on the incredibly strong historical correlation between finance and prices, as illustrated by the next charts:

As you can see from the above charts, investor and housing finance growth as well as dwelling price growth has crashed particularly hard across Sydney and Melbourne, but is also weak across the other major capitals. However, there are signs of stabilisation.

This data obviously pre-dates the Federal Election, as well as the RBA’s latest interest rate cuts, macro-prudential easing by APRA, as well as announced first home buyer subsidies. We therefore expect mortgage credit to improve in the second half, with house prices likely to rise modestly in 2020.

We’ll provide detailed analysis in MB’s half-year report for paying subscribers, due for release toward the end of the month.