The private sector is done for but all praise the gubmint, via Damien Boey at Credit Suisse:

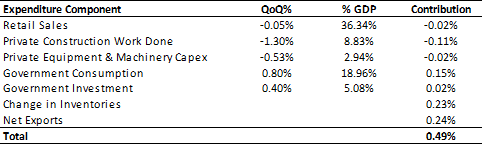

We now have all the partials we can get to “now-cast” 1Q real GDP. Today we received trade and government spending data, which on balance surprised to the upside:

- Net exports were as expected, contributing 0.2% to quarterly GDP growth.

- Government spending contributed to growth, with consumption rising by 0.8%, and investment rising by 0.4%.