The Australian Bureau of Statistics (ABS) today released the national accounts for the March quarter, which registered soft 0.4% growth in real GDP over the quarter and 1.8% growth over the year.

On a per capita basis, real GDP was flat over the quarter, which follows the September and December quarter’s 0.1% and 0.2% falls.

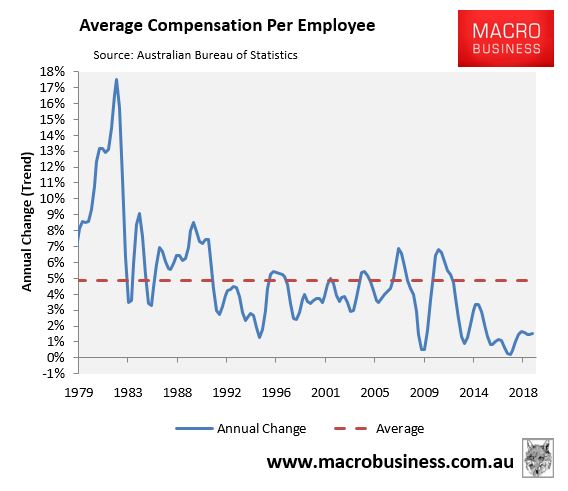

Most importantly for Australian workers, average compensation per employee rose by just 1.5% in the year to March – continuing the run of weak prints.

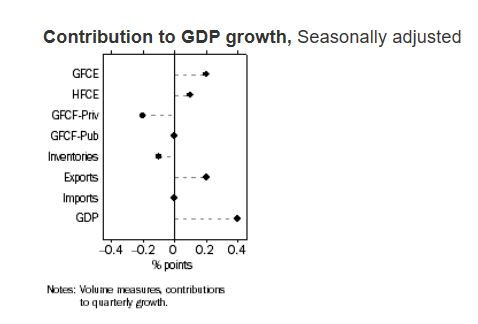

According to the ABS, seasonally adjusted GDP growth for the quarter was driven by public consumption spending and net exports, which each contributed 0.2% percentage points:

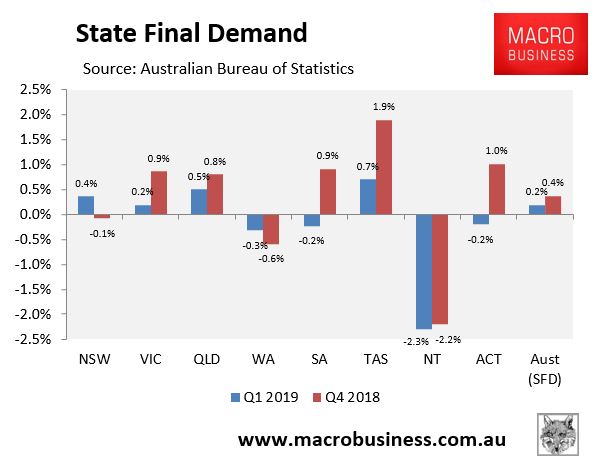

Quarterly final demand, which excludes export volumes, weakened to only 0.2% growth over the March quarter, with significant variation across jurisdictions:

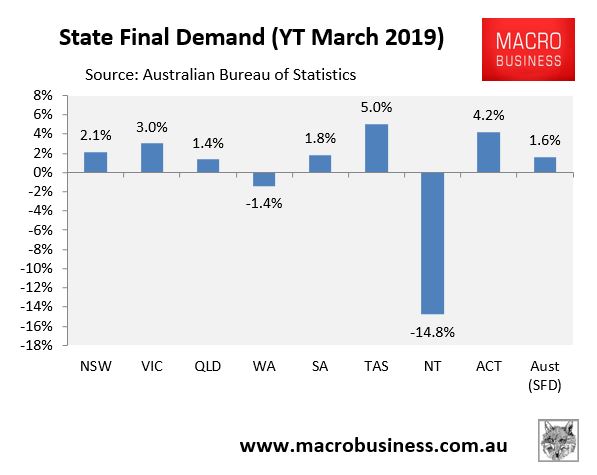

In the year to March 2019, final demand growth was anaemic, growing by just 1.6% nationally (0% on a per capita basis), with the mining strongholds continuing to struggle:

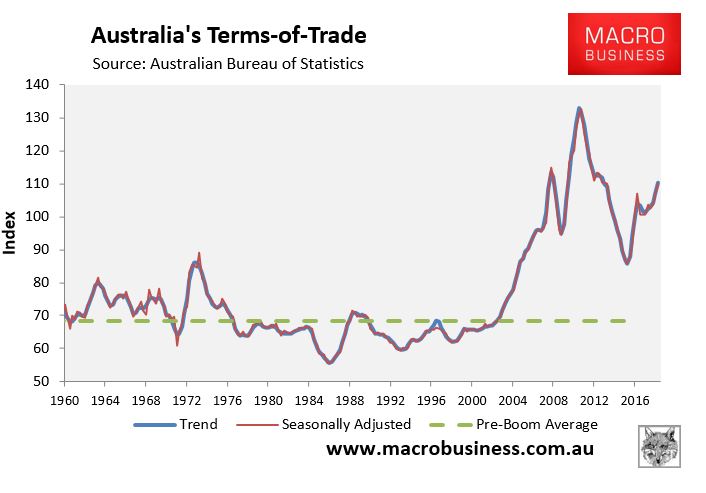

The terms-of-trade jumped by 3.1% over the quarter in seasonally adjusted terms and by 3.2% in trend terms. Over the year it rose by 6.1% in seasonally adjusted terms and by 7.9% in trend terms:

The strong lift in the terms-of-trade helped boost national income growth, with real NDI rising by 0.9% over the quarter and by 3.0% over the year.

After population growth, per capita NDI rose by 0.6% over the quarter and by 1.7% over the year.

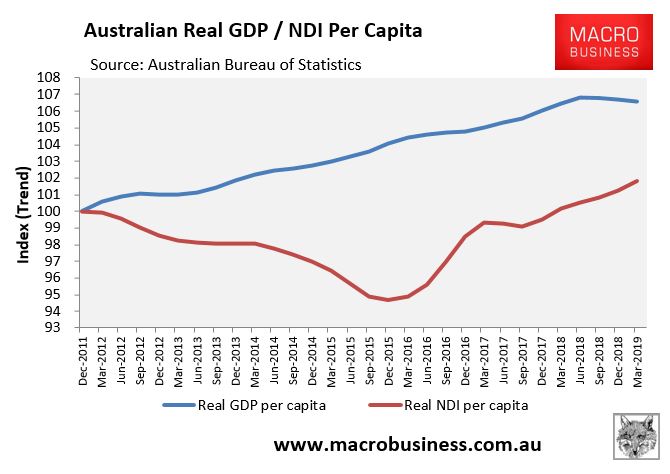

However, in trend terms, since December 2011, per capita NDI has risen by just 1.8% versus 6.6% growth in real per capita GDP:

As noted above, average compensation of employees remains in the gutter. It rose by a measly 0.4% in the March quarter in nominal terms and was up just 1.5% in the year to March 2018:

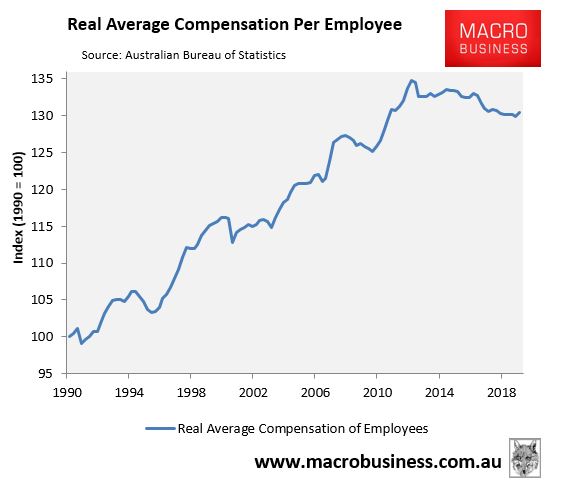

Adjusting for inflation, the situation facing Australian workers is glum, with real average compensation falling by 3.2% since March 2012; although it did rebound in the March quarter thanks to the sharp fall in the CPI (to 1.3%):

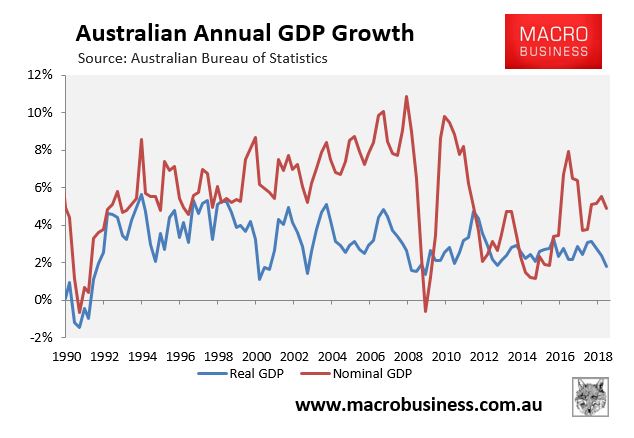

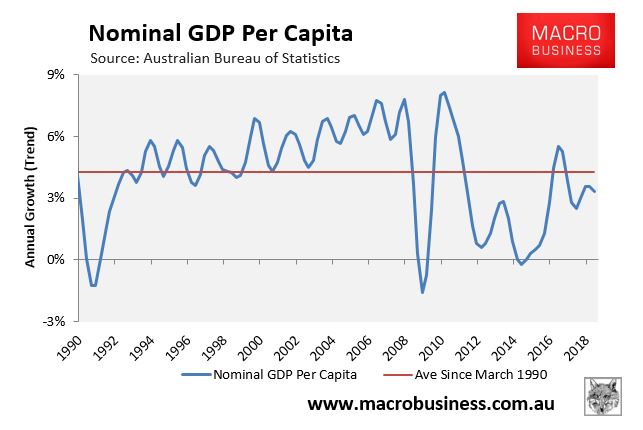

Nominal GDP rose by 1.4% over the quarter but just 4.9% over the year:

The below chart shows that trend nominal GDP is still tracking below the average since 1990, which continues to make life challenging for Government finances:

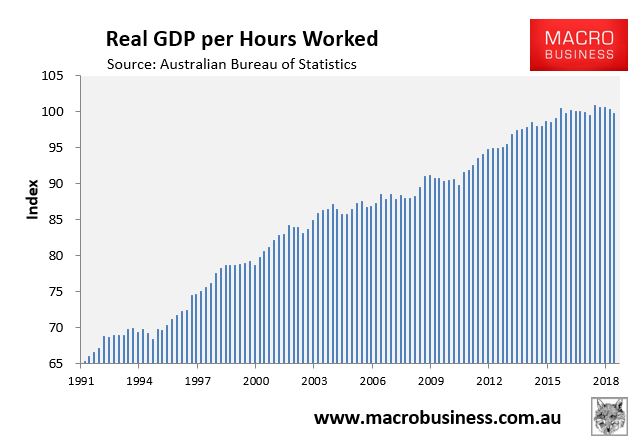

After rebounding last quarter, real GDP per hour worked fell for the fourth consecutive quarter, down by 0.5% in the March quarter and down 1.0% over the year, suggesting sluggish labour productivity:

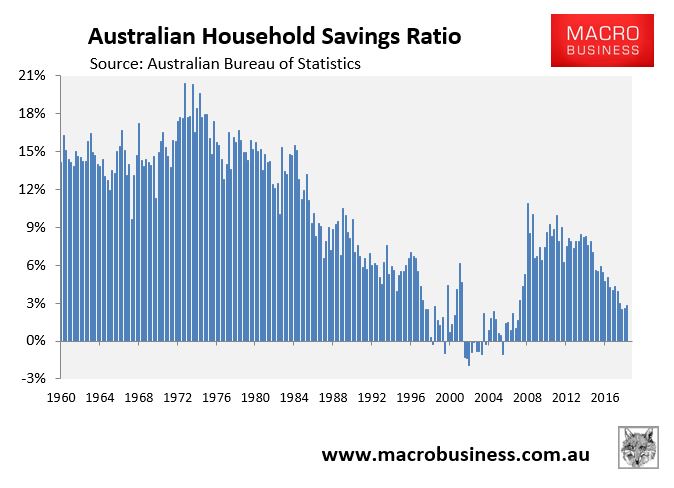

Meanwhile, the household savings ratio recovered slightly, rising by 0.2% to 2.6% – but remains near the lowest level in the post-GFC era:

In summary, not only is the headline growth figure weak, and the Australian economy is experiencing close to a per capita recession, there is further trouble under the hood.

First, Australian workers’ incomes remain in the gutter, as measured by the average compensation of employees.

Second, notwithstanding the tiny rise in the Mach quarter, households have been running down their savings. This is clearly an unsustainable support to household consumption, which is the main contributor to domestic demand.

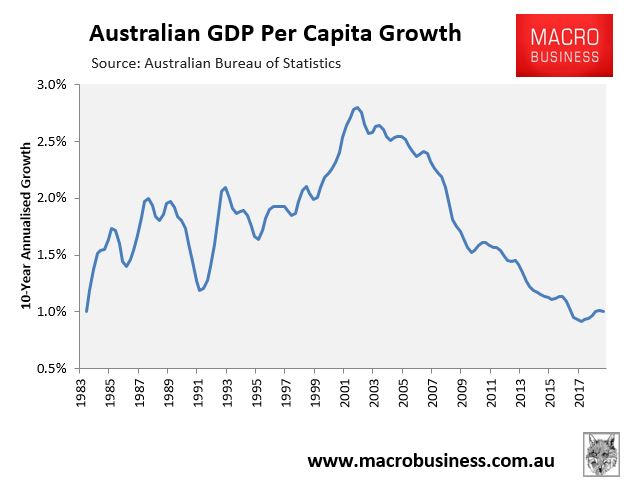

Third, Australia’s 10-year annualised growth in per capita GDP continues to track near its lowest level on record – i.e. around levels seen during the 1980s and early-1990s recessions:

Fourth, domestic demand fell in per capita terms over the March quarter – further signs of a per capita recession.

Fifth, labour productivity is weak, as evident by falling GDP per hour worked.

Finally, Australia’s growth is being driven largely by public (taxpayer) expenditure, rather than the private sector, which is ultimately unsustainable.

So, while there is still the ‘illusion’ of growth at the aggregate economy level, thanks to force-fed mass immigration and government spending, along with debt-fuelled consumption, the situation facing ordinary workers remains glum.

This is Australia’s ponzi economy in action: everyone’s share of the economic pie is not increasing sufficiently, real wages have been going backwards, and living standards in the big cities are being crush-loaded by the never ending people flood.