Advertisement

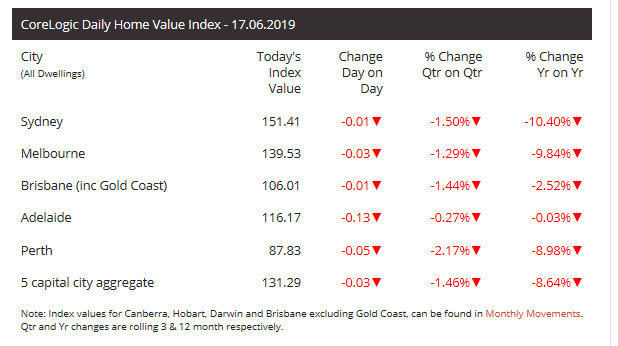

In all the years following the CoreLogic daily dwelling values index, I can’t remember ever seeing wall-to-wall falls across all major markets on a daily, quarterly and annual basis:

Certainly one to frame and put on display in the economic pool room.

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement