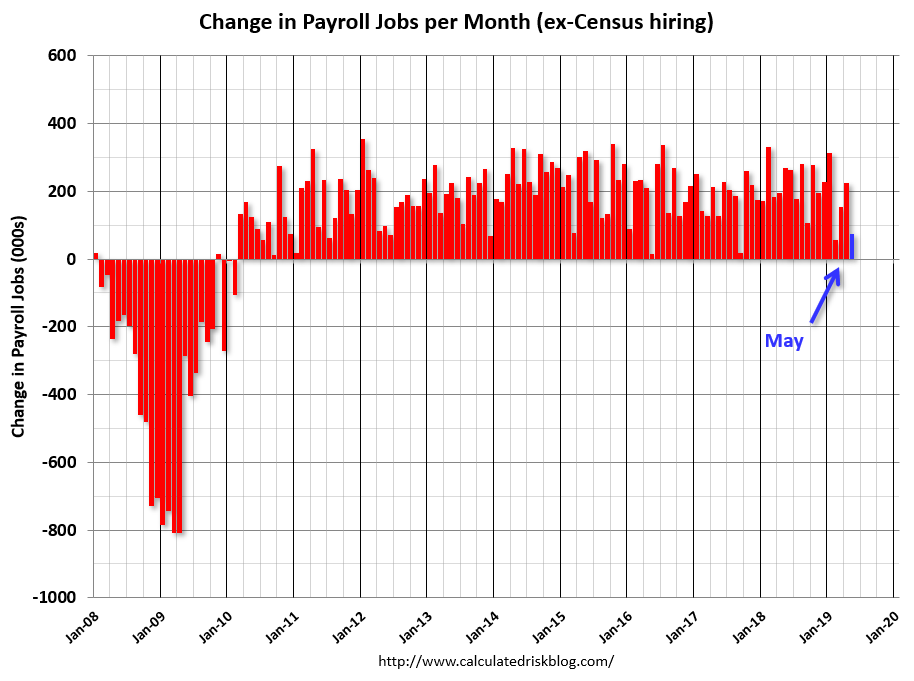

Total nonfarm payroll employment edged up in May (+75,000), and the unemployment rate remained at 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in professional and business services and in health care.

…The change in total nonfarm payroll employment for March was revised down from +189,000 to +153,000, and the change for April was revised down from +263,000 to +224,000. With these revisions, employment gains in March and April combined were 75,000 less than previously reported.

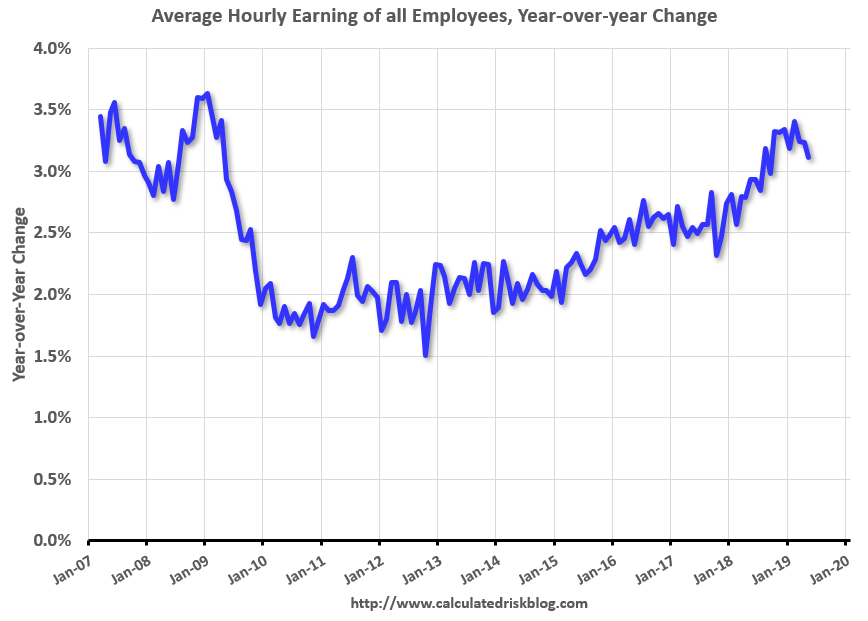

…In May, average hourly earnings for all employees on private nonfarm payrolls increased by 6 cents to $27.83. Over the year, average hourly earnings have increased by 3.1 percent.

Not terrible but clear deceleration. Fed hikes are just a matter of timing and quantity:

Advertisement

But that’s only the beginning. Once the Fed eases, the PBOC will almost certainly follow, as it hinted at Bloomberg:

In an exclusive interview with Bloomberg in Beijing, People’s Bank of China Governor Yi Gang also signaled that he’s not wedded to defending the nation’s currency at a particular level, and stressed that the value of the yuan should be set by market forces.

…“We have plenty of room in interest rates, we have plenty of room in required reserve ratio rate, and also for the fiscal, monetary policy toolkit, I think the room for adjustment is tremendous,” he said. Yi said the currency has been weaker recently due to “tremendous pressure” from the U.S. side but the impact will be temporary.

“A little bit of flexibility of renminbi is good for the Chinese economy and for the global economy because it provides an automatic stabilizer for the economy,” he said. “The central bank of China is pretty much not intervening in the foreign-exchange market for a long time, and I hope that this situation will continue, not intervening.”

As both central banks cut, it takes on the form of the shadowy “Shanghai Accord” of 2016. Whether any such deal actually existed between the Fed and PBOC for combined stimulus as the commodity crash of 2015 threatened a global shakeout is debatable. But there doesn’t need to be a deal. Once Fed tightening derails EM growth sufficiently for it to blow back into Wall St, the Fed must ease and the PBOC will always follow to prevent a rising CNY. It’s the same dynamic at work in American-led trade wars.

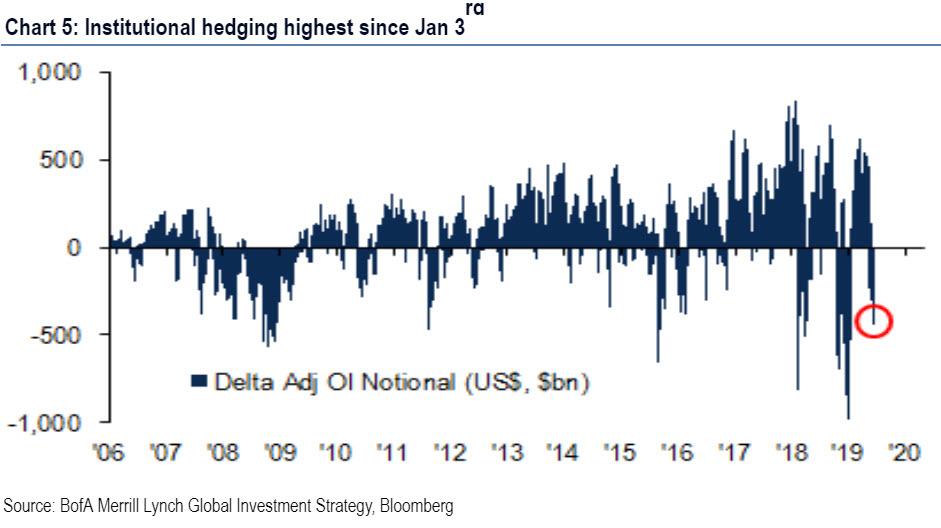

Positioning: investors are extremely bearish, with the BofAML Bull & Bear Indicator plunging to 2.5, a fraction away from “buy” signal level of 2.0; and equity investors very bearish – as the latest BofA FMS survey revealed, investors are most hedged since Jan 3rd equity lows. The weekly flow data suggests the same: $17.5bn into bonds (2nd biggest week of inflows ever) offset by $10.3bn out of equities; YTD $183bn into bonds, $155bn out of equities as nobody wants to have anything to do with stocks (despite the S&P being just shy of all time highs again).

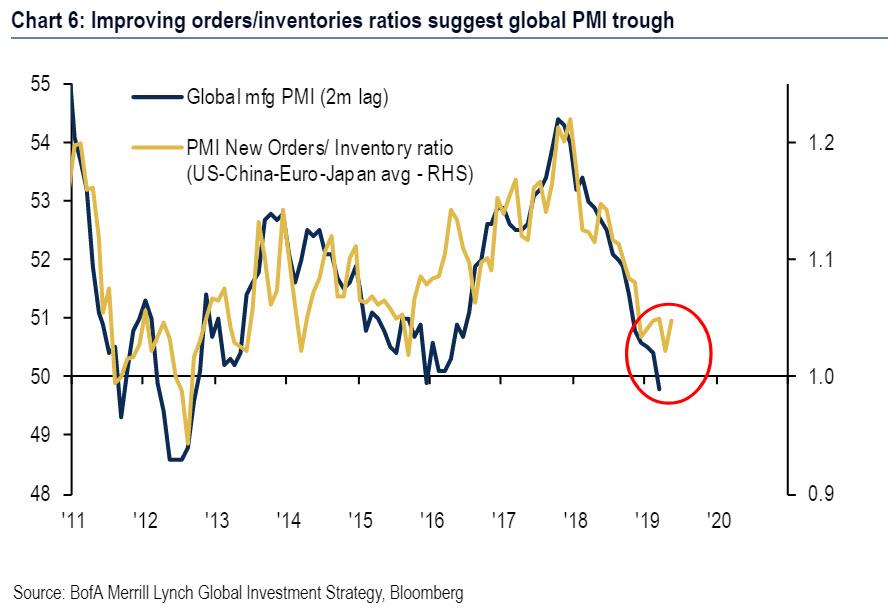

Profits are about to trough: the Global PMI (highly correlated with global EPS) was 49.8 in May, i.e. on “boom-bust” border; makes stocks a one-decision market…”sell” if PMI heads toward 45, and “buy” if PMI heads toward 55. However, providing a somewhat bullish take on this series, is the ratio of orders/inventories which leads PMI by 2-months and has turned higher. At the same time, US/China financial conditions are easing via liquidity/lower yields/lower oil, and assuming no material escalation of trade war, BofA thinks that PMI troughs next 3 months, resulting in a rebound in EPS as well.

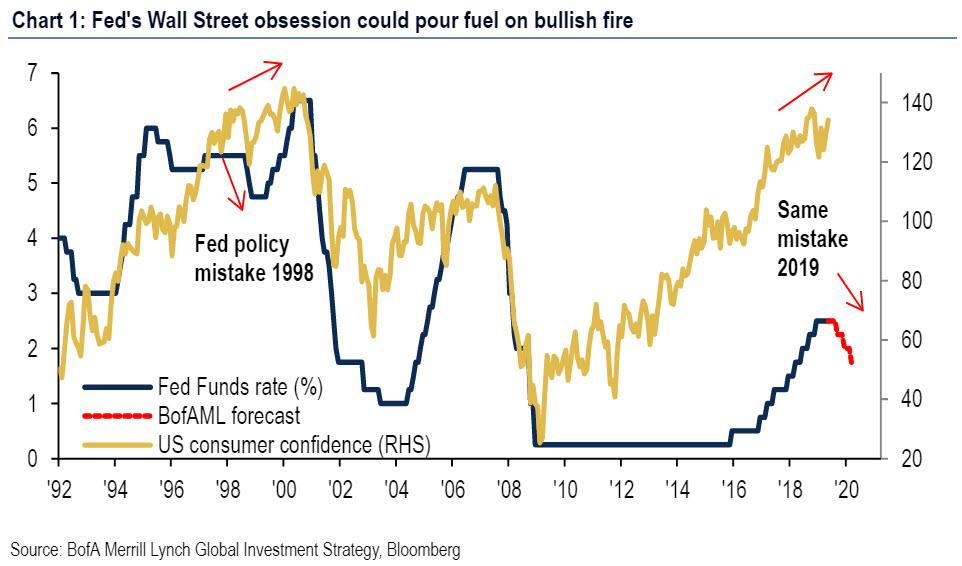

Monetary policy is already max bullish and exhibits clear parallels to the Shanghai Accord ’16, ahead of the Osaka G20 meeting. As a reminder, the Shanghai Accord saw global coordinated policy easing coinciding with extreme pessimism & trough in profit expectations. In its aftermath, the S&P500 & ACWI multiple jumped 1.5-2x in next 3 months. Fast forward to today, when in the run-up to Osaka G20 big global monetary ease underway, investor sentiment is likewise plunging. At the same time, a key catalyst is already in play – there is a big global monetary ease underway for 1st time since Q2’17 as 9 central banks cutting rates and Fed/PBoC/ECB/BoE are all turning dovish while there are rate cuts in Malaysia, New Zealand, India, Philippines, Australia; additionally if Trump changes his mind and there is no U.S. imposition of 25% tariffs on remaining $300bn of Chinese goods policy will be max bullish for risk in H2; however, the narrative can quickly flip to trade war, leading to 2019 playing out like Asia crisis ’98.

In other words, all else equal, the foundations for the S&P rising to 3,000 in the summer – which is BofA’s base case (before the S&P slides back down in the second half) are already there. In light of this, the risk is that the Fed does precisely what the market now expects with certainy, that it cuts rates as soon as July.

This is shown in the chart below, when in the aftermath of the Asian crisis of 1998, the Fed cut rates only to cause the dot com bubble… and its subsequent bursting and the plunge in rates from 6%+ to just 1% as the first 21st century bubble popped.

It is this risk that threatens markets now as well: an overly easy Fed cutting rates, only to create a historic meltup just ahead of the 2020 election, and eventually bursting the biggest asset bubble in history.

There’s more: the Fed could cut and join the ECB and BOJ among those central banks that are losing credibility, as a result of it “patiently” flipping from hikes to cuts with no material change in macro: after all, in the past 6 months US CPI is unchanged, and, as BofA notes, the US unemployment rate down.

Under the circumstances, the Australian dollar is doing well to not to skyrocket as it did under Shanghai Accord 1.0. Higher ahead in the short term.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.