DXY fell again last night as EUR rose and CNY was soft:

The Australian dollar blasted through 0.7 cents and against DMs:

Advertisement

Not so much EMs:

Gold firmed:

Oil struggled:

Advertisement

Metals too:

Big miners lifted:

EM stocks too:

Advertisement

US junk roared back but not EM:

Treasuries pulled back:

Bunds were bid:

Advertisement

Stocks took off:

The key event of the evening was a little comment from Fed Governor Jay Powell:

I’d like first to say a word about recent developments involving trade negotiations and other matters. We do not know how or when these issues will be resolved. We are closely monitoring the implications of these developments for the U.S. economic outlook and, as always, we will act as appropriate to sustain the expansion, with a strong labor market and inflation near our symmetric 2 percent objective. My comments today, like this conference, will focus on longer-run issues that will remain even as the issues of the moment evolve.

it’s time to rethink long-run strategies…[ZIRP] has become the preeminent monetary policy challenge of our time…perhaps it is time to retire the term ‘unconventional’ when referring to tools that were used in the crisis. We know that tools like these are likely to be needed in some form in the future…the next time policy rates hit the lower bound – and there will be a next time – it will not be a surprise.

Advertisement

He’s learning. Rate cuts and more QE is coming. The “Powell put” returns withe a vengeance.

That said, global growth is sliding fast. The JPM global PMI is now in contraction:

Global PMI surveys signalled that manufacturing downshifted into contraction during May. Business conditions deteriorated to the greatest extent in over six-and-a-half years, as production volumes stagnated and new orders declined at the fastest pace since October 2012.

The trend in international trade continued to weigh on the sector, with new export business contracting for the ninth month running. Business optimism fell for the second month in a row and to its lowest level since future activity data were first collected in July 2012.

The J.P.Morgan Global Manufacturing PMI™ – a composite index1 produced by J.P.Morgan and IHS Markit in association with ISM and IFPSM – posted 49.8 in May, down from 50.4 in April, its lowest level since October 2012. Later-than-usual release dates meant manufacturing PMI data for Colombia, Ireland and Thailand were not available to include in the May 2019 global readings.

Downturns continued in the intermediate and investment goods industries, which both saw output and new orders fall further during May. Although the consumer goods sector fared better in comparison, with production and new business rising, rates of expansion eased.

National PMI data signalled deteriorating business conditions in several major industrial regions including the euro area, Japan, the UK, Canada, South Korea and Taiwan. PMI readings for the US, China and Brazil were only a few ticks above the benchmark 50.0 no-change mark. The downshift in growth in the US was the main driver of the slowdown in global manufacturing, as the US PMI slipped to its lowest level in almost a decade (September 2009).

Advertisement

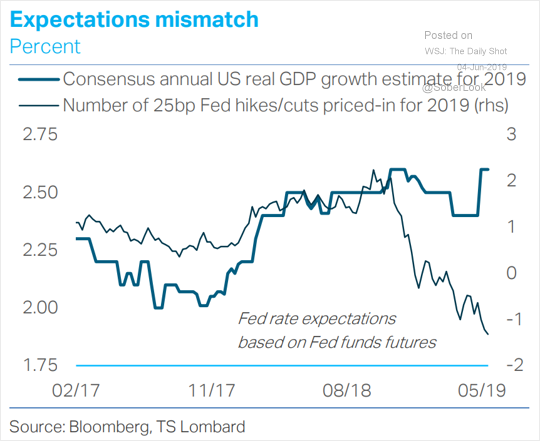

That kind of speaks for itself. So the Fed outlook is now for easing with market pricing well ahead of economists:

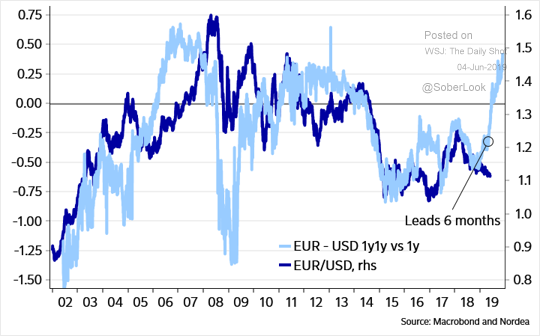

And the vital EUR/USD yield spread now favouring the latter:

Advertisement

As the EUR rises the AUD will too, ipso facto. I’m afraid to say that the Lunatic RBA missed its window on the currency.

I can’t see it getting overly far. Housing markets and the economy are going to spring out their slump like a nonagenarian in a swamp. The ASX is priced for a perfection that is falling apart all around us. There’s little fiscal support coming. The ScoMo rebound is all hot air. Other central banks will follow the US with more easing, most particularly China, weighing on CNY.

Advertisement

But in the short term, the Australian dollar looks set to rally into whatever rough beast this way comes. At least until it arrives.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.