Australia’s production, as measured by aggregate real GDP, continues to diverge wildly from the growth (or lack thereof) in ordinary Australian’s living standards.

To illustrate why, I have once again deflated three measures of the domestic economy, as provided in the March quarter national accounts (released yesterday), by the ABS’ population data, in order to ascertain the underlying strength of the domestic economy in per capita trend terms.

The three measures chosen are:

- National Disposable Income (NDI), which is “considered a good measure of progress for living standards because it is an indicator of Australians’ capacity to purchase goods and services for consumption” (see ABS explanation here).

- Gross national expenditure (GNE), which is “the total expenditure within a given period by Australian residents on final goods and services (i.e. excluding goods and services used up during the period in the process of production). It is equivalent to gross domestic product plus imports of goods and services less exports of goods and services”.

- Domestic final demand (DFD), which is the sum of “government final consumption expenditure, household final consumption expenditure, private gross fixed capital formation and the gross fixed capital formation of public corporations and general government”.

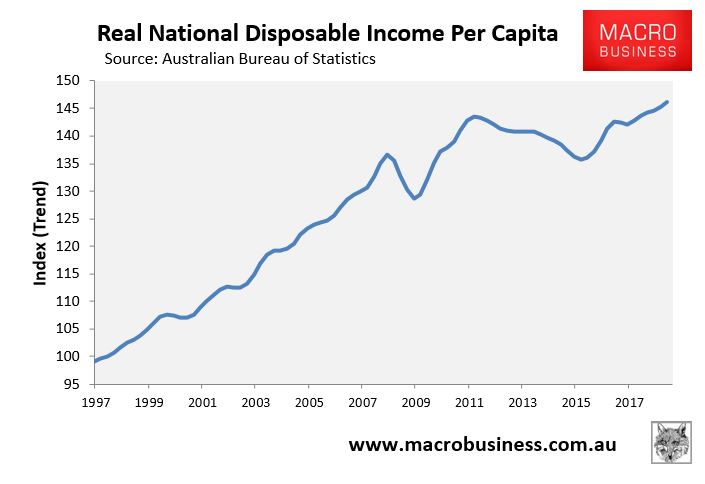

First, let’s consider real per capita NDI. As shown below, this measure rose by 0.6% in the March quarter in trend terms to be up by 1.7% over the year. However, real per capita NDI has risen just 1.8% since December 2011, suggesting stagnating living standards:

Per capita NDI is also just 6.0% higher than September 2008 when the GFC hit. That’s more than a decade with minimal income growth.

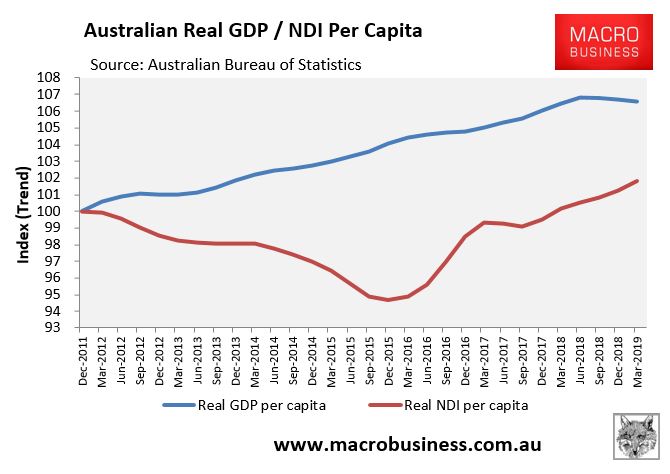

The divergence between per capita NDI and GDP remains stark:

Since December 2011, real GDP per capita has risen by 6.7% compared with only a 0.9% rise in real per capita NDI.

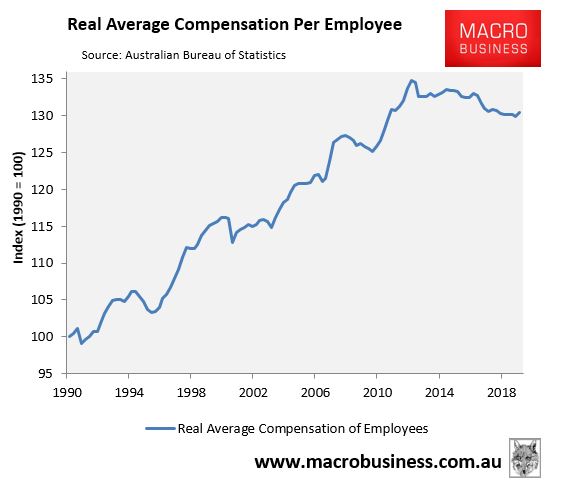

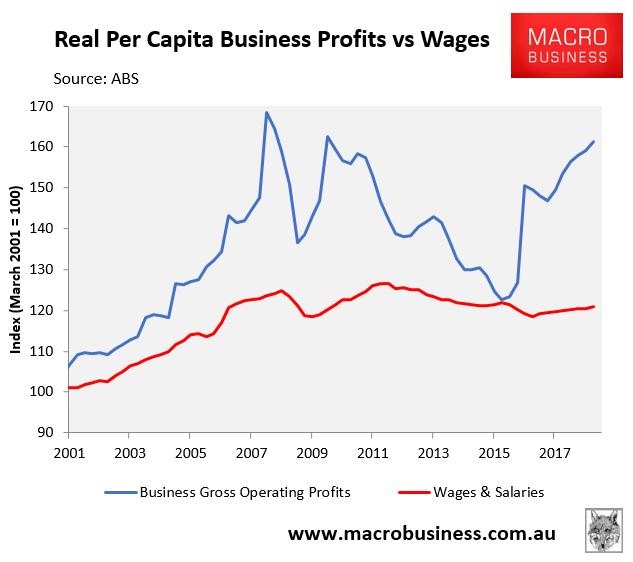

A more alarming trend is the extent to which Australian workers have failed to benefit from the recent rebound in the terms-of-trade and NDI. As shown in the next chart, real average compensation per employee has collapsed, down 3.2% since March 2012; although it did post a small rebound in the March quarter owing to the sharp fall in the CPI (to 1.3%):

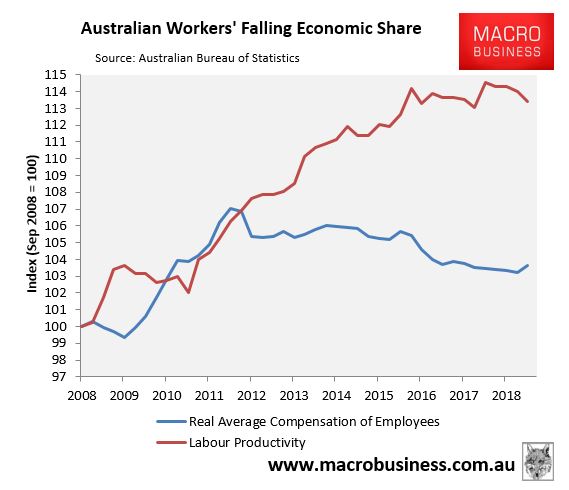

The sad reality is that since March 2012, Australian workers’ real incomes have fallen sharply despite rising labour productivity, with the spoils going to corporations:

This disconnect is shown more clearly by the wages & profits data released separately to the quarterly national accounts:

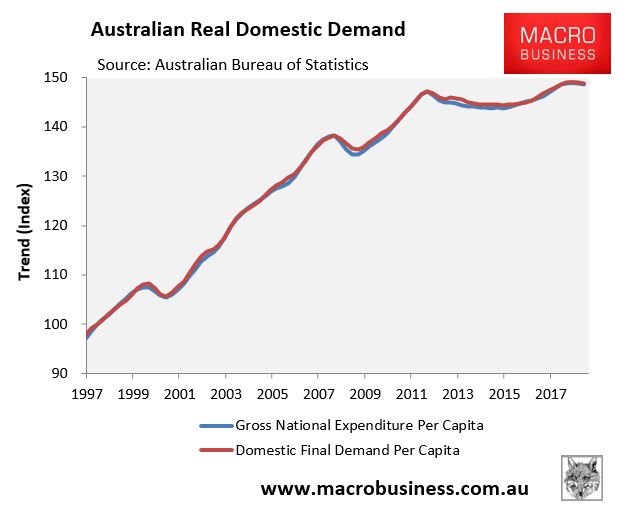

Similar trends are evident with GNE and DFD, which despite moderate improvements recently have recorded almost zero growth since June 2012:

Real per capita GNE and DFD are just 1.0% and 1.1% higher respectively than June 2012.

Essentially, the big expansion in commodity export volumes over recent years and mass immigration has supporting headline GDP, but hidden the fact that the domestic economy remains sick.

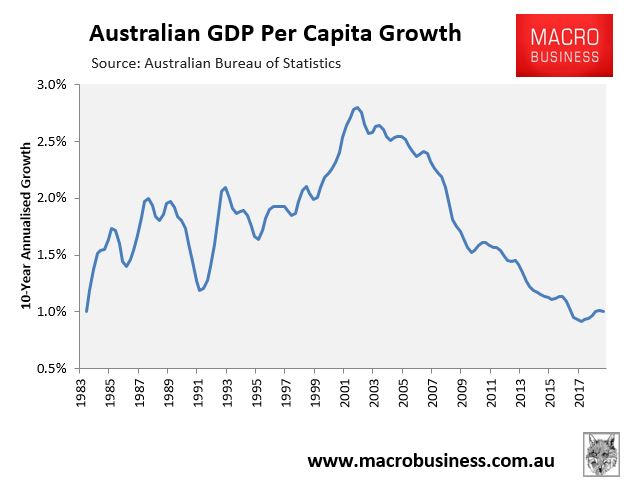

It is also worth noting that Australia’s GDP growth has been lacklustre when measured in per capita terms. Australia’s 10-year annualised growth in per capita GDP has crashed and is tracking near its lowest level on record – i.e. the same or worse than the 1980s and early-1990s recessions:

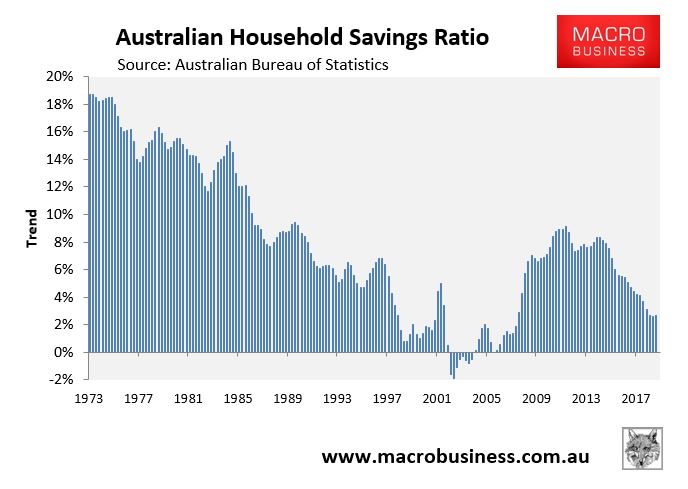

Household consumption spending has been held-up purely by running down savings amid falling incomes, with the household savings rate falling to around its lowest level in the post-GFC era at just 2.7% in trend terms. This is clearly unsustainable:

These reasons are why MB keeps arguing that Australian households are in the midst of their own “lost decade”. While the aggregate economy is still growing, albeit anaemically, they are clearly missing out.

unconventionaleconomist@hotmail.com