Spot up. Paper calm. Steel up. CISA late March steel output fell sharply and is only up a little year on year. I’ve added a second line (in black) to show what underlying demand is like ex-reforms that shifted illegal scrap production into blast furnaces over the past two years to give some measure of underlying demand. As you can see, it is not flash.

Advertisement

This is evidence that despite the supply problems for bulks, demand is actually far below where current prices would have it. This suggests that incremental resolution in supply side issues will result in relatively swift price corrections, assuming no more stimulus. Westpac has an outlook today that nicely summarises the base case for this:

The Vale disaster continues to roil the market

Following the failure of Vale’s tailings Dam 1 at the Córrego do Feijão mine in Minas Gerais on the 15th of February, the Brazilian National Mining Agency (ANM) banned all upstream tailings dams, with inactive dams to be decommissioned by 21 August and active dams by 23 August. In response, Vale has halted production at Brucutu, Alegria and Timbopeba mines. Prior to the Brazilian dam disaster, iron ore seaborne trade was looking at a surplus of around 20Mt. Post the disaster and closure of Vale mines, it now appears the market will post a deficit of around 34Mt in 2019.

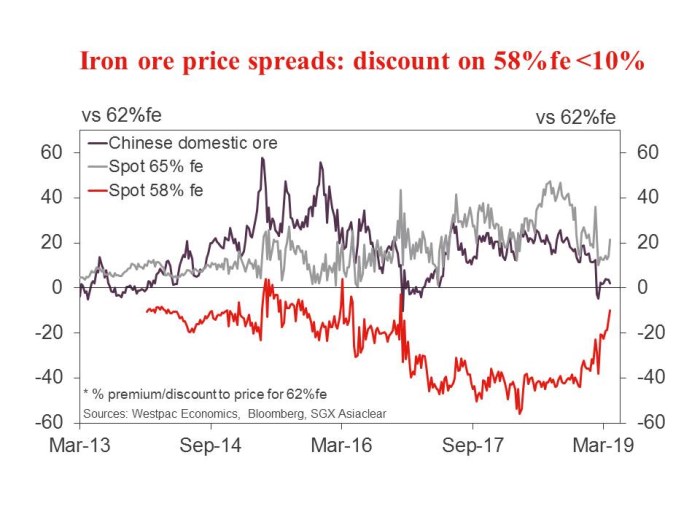

Ore inventory at Chinese ports is around 145Mt but it appears they are being drawn down. The March quarter is traditionally when port inventories are rebuilt and the 2% rise this year was much softer than usual – seasonally adjusted port inventories fell 2.6% in Q2 the third consecutive quarterly fall. Storms in March disrupted Australian shipments, which along with Brazilian disruptions, impacted on ore volumes and the price of seaborne ore closed the gap to Chinese ore. At the same time, the discount for 58%fe (vs 62%fe) closed to less than 10%, the smallest it has been since mid-2016 and well below the longer-run average of 25%.

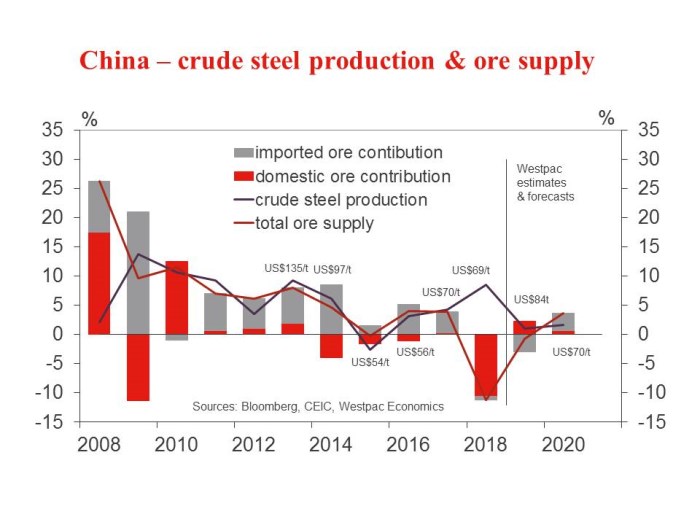

Chinese ore production set for a modest lift

The narrowing of the price spread matters as it increases the attractiveness of Chinese ore, driving a lift in production and the further unwinding of inventories. With a modest relaxation of environmental/safety regulations, Chinese ore production should lift by around 15Mt in 2019 (in 2018 Chinese ore production was 180Mt on 62%fe basis). For the near term, Australian production returning to normal should cap iron ore prices. However, if iron ore prices continue to rise, the rate of steel scrap substitution for ore in Chinese blast furnaces is likely to increase, reducing the demand for both iron ore and met coal and leading to a further narrowing in price spreads. Prices are forecast to peak in Q2 as Australian supply recovers from cyclone disruptions, Chinese production lifts and there is an increase in the use of scrap steel. Given that spot prices have exceeded our expectations to date, and the supply hit from Vale mine closures are larger than initially expected, our forecasts for iron ore have been revised. Spot 62%fe is now forecast to end the June quarter at $US87/t (was US$85/t) and end 2019 at US$77/t (was US$75/t).

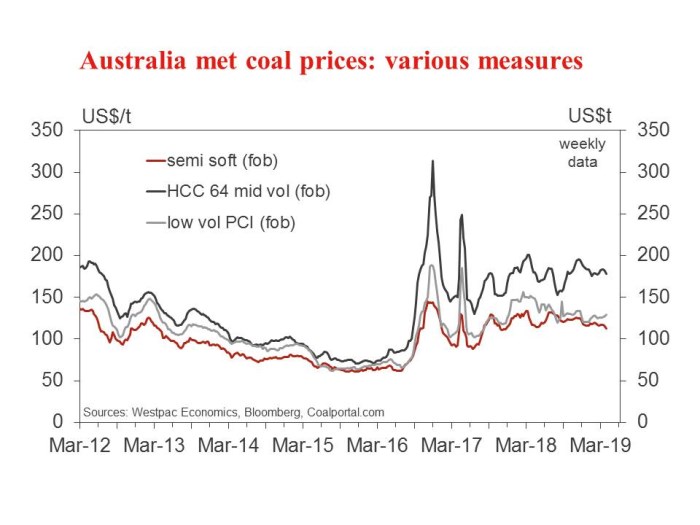

Lack of supply supporting met coal

Met coal has seen a steady stream of disruptions to Australian supply (recent severe storms disrupted production at Queensland mines, rail-lines and port facilities) which with relatively robust demand has resulted in Qld Met Coal prices holding a range of US$175–185/t. The Department of Industry Innovation & Science is forecasting Australia’s export volumes of met coal to grow from 179Mt in 2017/18 to 203Mt 2022/23 but in 2019 there is just a 5% lift to 188Mt. The demand in 2019 should be supported by India’s rapidly expanding steel sector and Chinese stimulatory measures in response to slower economic growth and growing trade concerns. We are, however, closely watching the substitution of ore with scrap steel in China, as rising scrap steel usage reduces the requirement for met coal in steel production. Qld met coal is now forecast to end 2019 at US$165/t (vs. US$150/t previously).

That looks right to me, lower again next year and the year after. In short, all things equal, we’re peaking right now.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.