SQM Research’s flawed and debunked analysis of Labor’s negative gearing policy looks to have united Australia’s property parasites.

The Real Estate Institute of Australia (REIA) has warned of economic Armageddon from Labor’s policy:

“The losers are mum and dad investors, home owners, renters, the construction industry, state governments and the economy”…

“There are no winners. Even first home buyers will face a faltering economy with lower employment prospects,” the REIA president concluded.

The Housing Industry Association (HIA) has warned of soaring rents:

“Changes to existing capital gains tax and negative gearing arrangements on residential investment properties proposed by the federal opposition will dampen first home buyer capacity to save for their first home,” explained MD at HIA, Graham Wolfe…

“Any increase in rental costs will impact capacity to save a deposit, extend the savings’ period and dampen home ownership aspirations”…

“Australia needs to reverse this trend, renew our national commitment to home ownership and adopt measures that support first home aspirants. That includes support while saving for a deposit,” concluded Wolfe.

As has the Urban Development Institute of Australia (UDIA):

“Currently, investors accept modest rental returns because they expect to realise a capital gain in the future, when they sell their investment property,” he said.

“However, this will not happen if there are fewer investors out there and they are relying on owner-occupiers to eventually buy their investment property. This will make people unwilling to invest in the first place, further exacerbating the problem.”

Whereas Daniel Walsh from Your Property Your Wealth – a buyers’ agent for investors – repeated the debunked lie that the abolition of negative gearing in the 1980s caused rents to surge:

Mr Walsh said scrapping negative gearing made it less lucrative to be an investor, which meant there was less rental stock to meet demand.

‘In 1985, the newly minted Hawke Labor government abolished negative gearing on rental properties,’ he said.

‘They, too, believed it would aide housing affordability by evening the playing field, so owner-occupiers could get into the market at the expense of landlords.

‘You know what happened? Rents went up. With less rental stock in the market, supply dwindled while demand remained high and prices increased.’

Mr Walsh said Labor’s policy would ‘see rents increase and your competition for good investment opportunities dry up’.

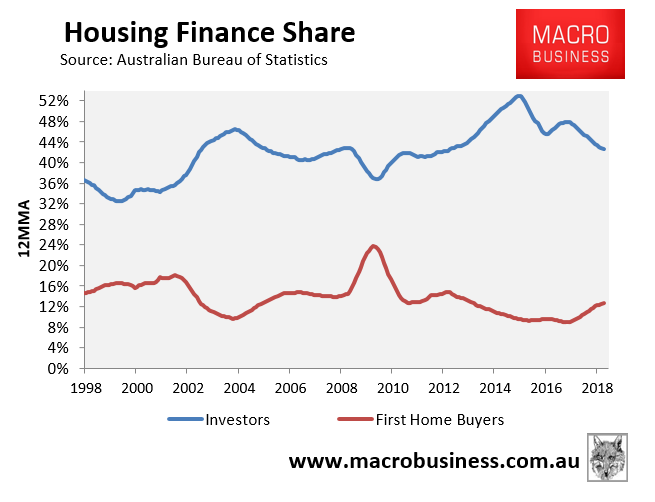

Anyone without a vested interest knows that Labor’s policy will be unambiguously good for first homes buyers (FHBs).

There is an inverse correlation between FHBs and investors, meaning that as fewer investors flood the market (and prices fall), there will be a lift in FHBs and home ownership rates:

Indeed, the Australian Treasury concluded that Labor’s policy would shift the “composition of ownership… away from domestic investors”, thereby helping to boost home ownership rates.

Meanwhile, the claim that rents will magically rise under Labor’s policy doesn’t make much sense. Contrary to the claims of the property lobby, there was zero impact on rents when negative gearing was abolished between 1985 and 1987. And unlike Labor’s current policy, the 1980s experiment didn’t maintain negative gearing on new builds.

Let’s not forget that only last month, housing experts smashed the property lobby’s claims about rents:

Grattan Institute budget policy director Danielle Wood… said that the Treasurer’s “scare campaign on rents makes even less sense”.

“If there are fewer investors there are less properties for rent, but those properties don’t disappear – home buyers move in, and so there are also fewer renters,” she said.

Tenants’ Union of NSW senior policy officer Leo Patterson Ross said that renters, would-be home buyers, researchers, and those at the coalface of affordable housing and homelessness know that “this housing tax warning and these problems are not real concerns” but rather “just industry trying to protect their business model”.

There is “no credible evidence” to support the government’s claims that rents would rise, Mr Patterson Ross said…

“If they think reforming negative gearing and the CGT discount would increase rents, then why are they not supporting it? They are treating Australians with contempt.”

UNSW City Futures research fellow Chris Martin also rubbished the Treasurer’s claims… “Investors do not currently pass the benefit of negative gearing onto tenants; they leverage that benefit into greater purchasing power for themselves, and hence into higher prices,” he said.

By reducing investor demand for housing as a financial product, the reforms should also help bolster flagging home ownership rates, by assisting renters in making the leap to buying, Dr Martin said.

“The proposals should result in more renters becoming home owners, because they will be less likely to be outbid for properties by ‘investors’ than they currently are,” he said.

As we keep saying, now is actually a good time to implement Labor’s policy. Since investor demand has already crashed, there’s far less risk of investor flight and widespread market disruption than if investor demand was running at the turbo-charged levels of two years ago.

What Labor’s policy will do, however, is prevent a future investor bubble, moderate the cycle, and boost the first home buyer share over the longer-term.

But that isn’t going to satisfy bankers who descended upon the AFR:

The availability of credit is being squeezed by the emergence of micro-regulation which is weighing on the size of loans small businesses can afford while making bankers fearful of making a mistake, Westpac’s business banking boss David Lindberg said.

Mr Lindberg – who was appointed to head up Westpac’s consumer banking division following an executive reshuffle last week – said responsible lending obligations and weaker house prices had contributed to a situation where business investment had “ground to a halt”.

Mr Lindberg said the combination of small business owners feeling the wealth effect and over-zealous bankers who were making borrowers go into excruciating details because “there are scared of making a mistake” was making matters worse.

Good. After a period of far too lax lending standards what else should we expect? Next up, a fundie used to enjoying the bank’s rentier returns is also moaning:

A major global investor in the banks has warned that ongoing government raids on bank profits would increase the cost of funding, while a senior legal adviser feared the corporate regulator’s a “litigate first” strategy will delay customers being compensated and restrain credit growth.

Fidelity International portfolio manager Kate Howitt told The Australian Financial Review Banking & Wealth Summit that the royal commission had shown banks to be “too big to behave badly” but said this should not lead policy makers to raid the cookie jar.

“These banks have had failings and have remediation programs. That doesn’t now make them the cookie jar of the nation that we dip into whenever we need a snack,” she said.

Yes, it does. When banks are wards of state, such as our guaranteed current account funding big four, that is exactly what they can expect to be. If not, get off the guarantees and return to more normal rates of return then can complain with justification about being a cookie jar.

The parasite swam them moved down the value chain with nobody’s like PIP up in lights, also at the AFR:

“Lower interest rates from the Reserve Bank will be fruitless unless the assessment lending rate is reduced by APRA,” Property Investment Professionals of Australia chair Ben Kingsley said.

…”[The current market] has everything to do with the regulator, not demand – It has been manufactured first with a cap on interest-only lending, but most importantly what really took demand completely out of the market was their strict interpretation of assessment lending rates and leaving them at 7 per cent. That’s killed borrowing power,” Mr Kingsley said.

Lending standards are where they should be finally. Hello, Hayne Royal Commission?

Finally, construction and mortgages got a hearing:

While an interest rate cut would have a positive effect on consumer sentiment, Stockland chief executive Mark Steinert said it was the availability of credit and the loan approval process that remained the most critical factors.

…Economists are increasingly expecting the next move by the RBA to be a rate cut, after rates have remained on hold at a record low of 1.5 per cent since August 2016, but Steve Mickenbecker, group executive, financial services at Canstar agreed it would not be enough to suddenly quash the pervasive negative sentiment in the market.

Correct. This is the whole point of macroprudential. It tightens credit while the price falls so that the currency tumbles. That shifts growth drivers away from household debt to external competitiveness. So long as you have central bank that has a clue.

Boy, what a swarm.