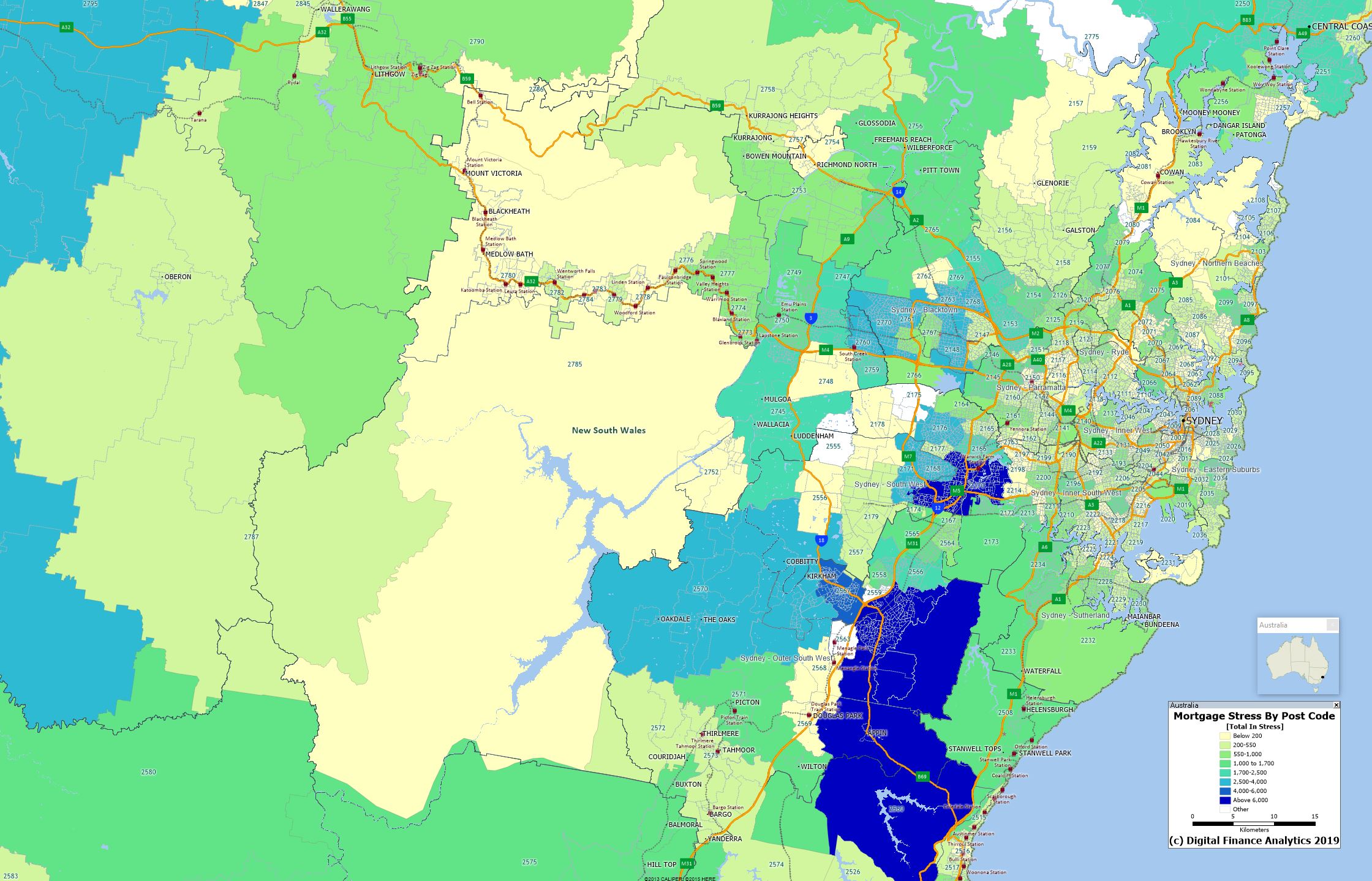

Via Martin North today come some cool mortgage stress maps. Sydney:

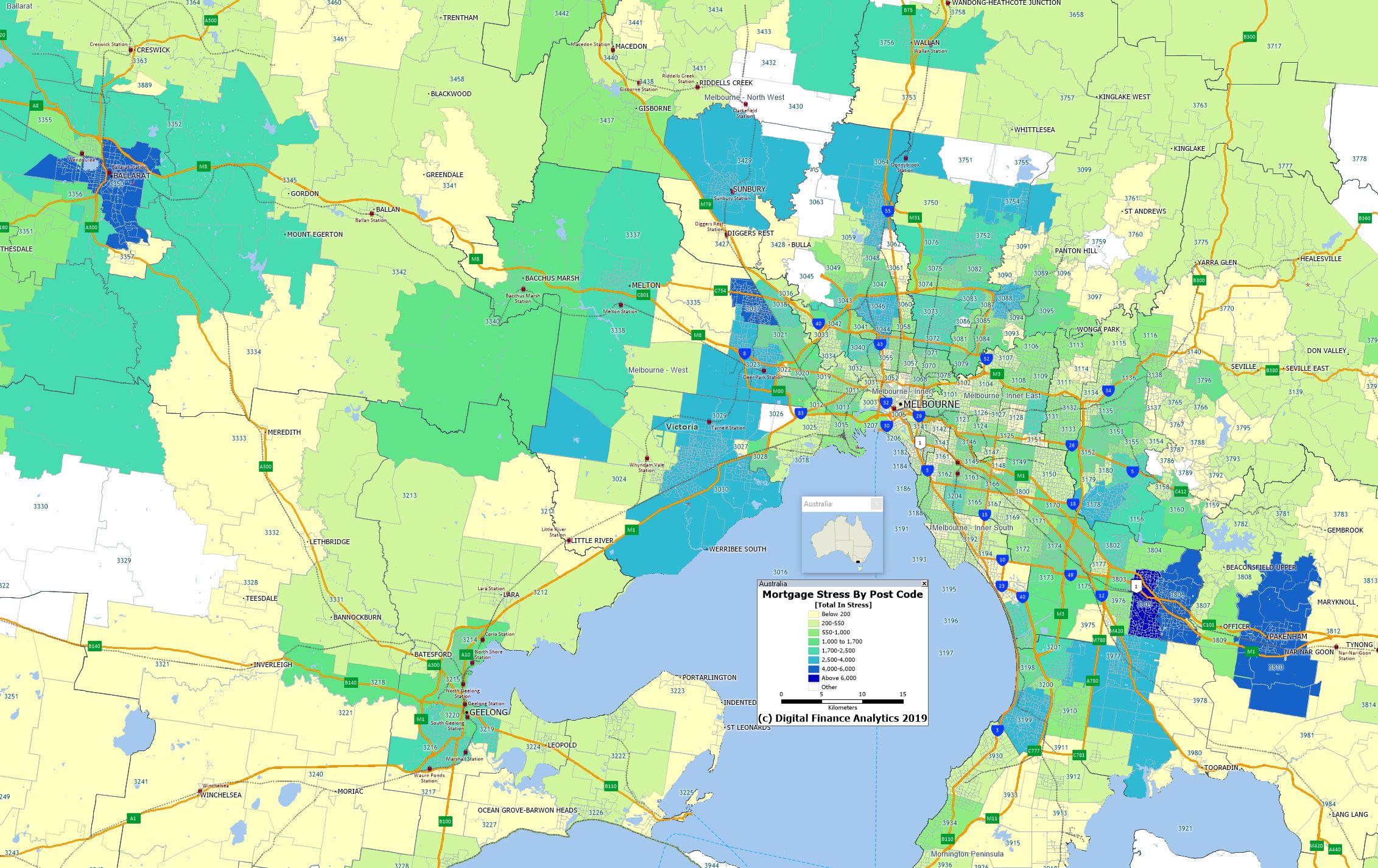

Melbourne:

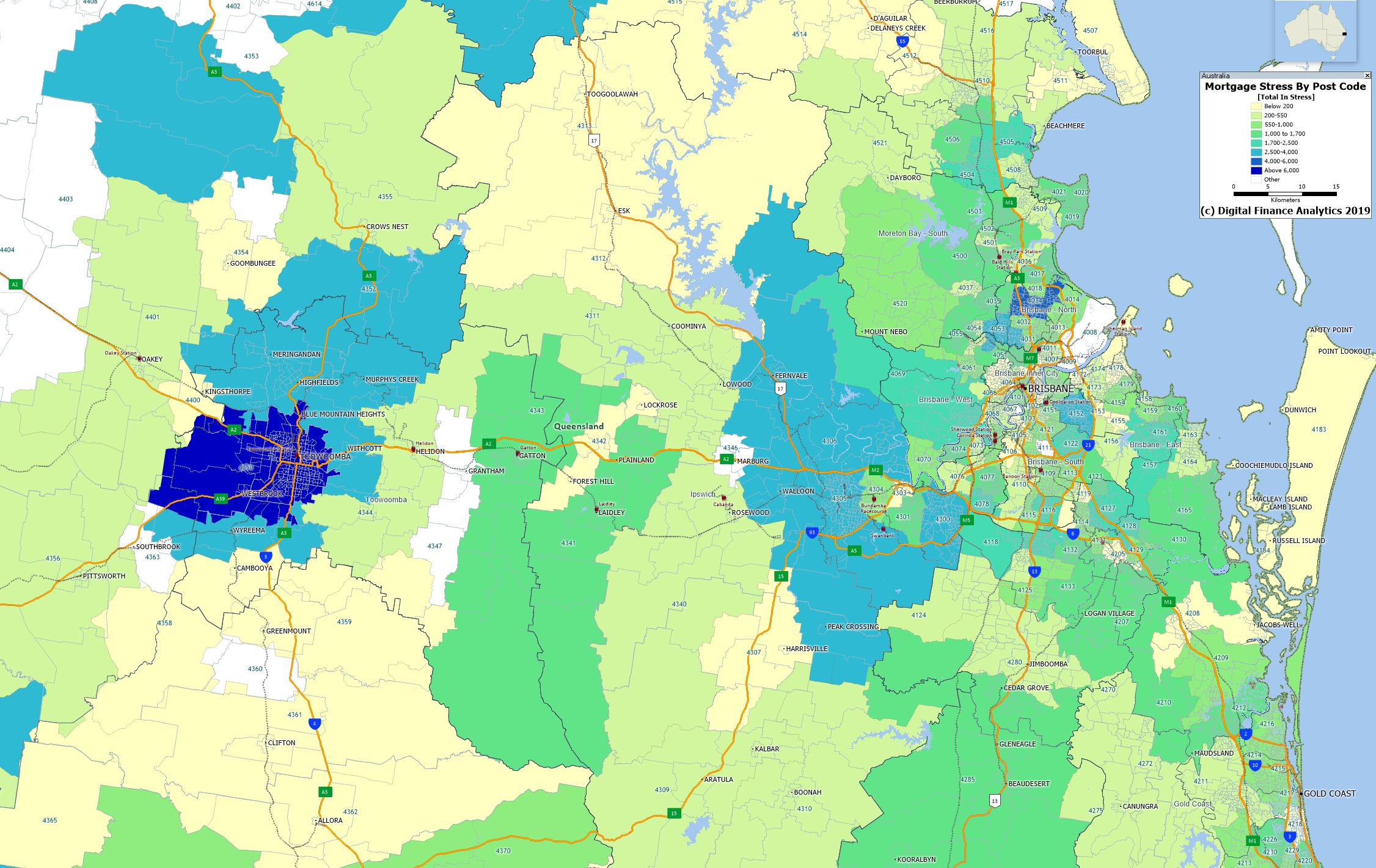

Brisbane:

Advertisement

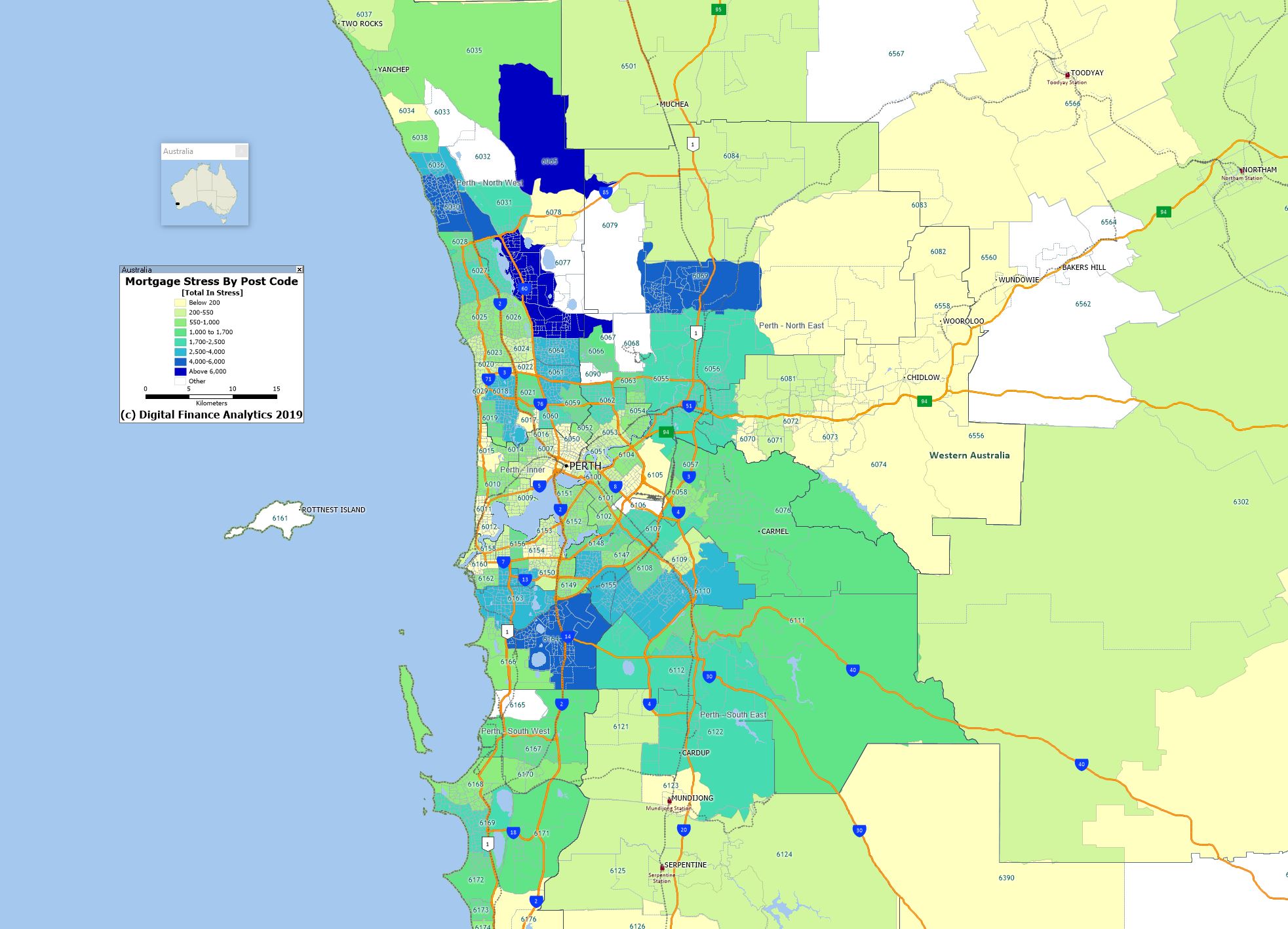

Perth:

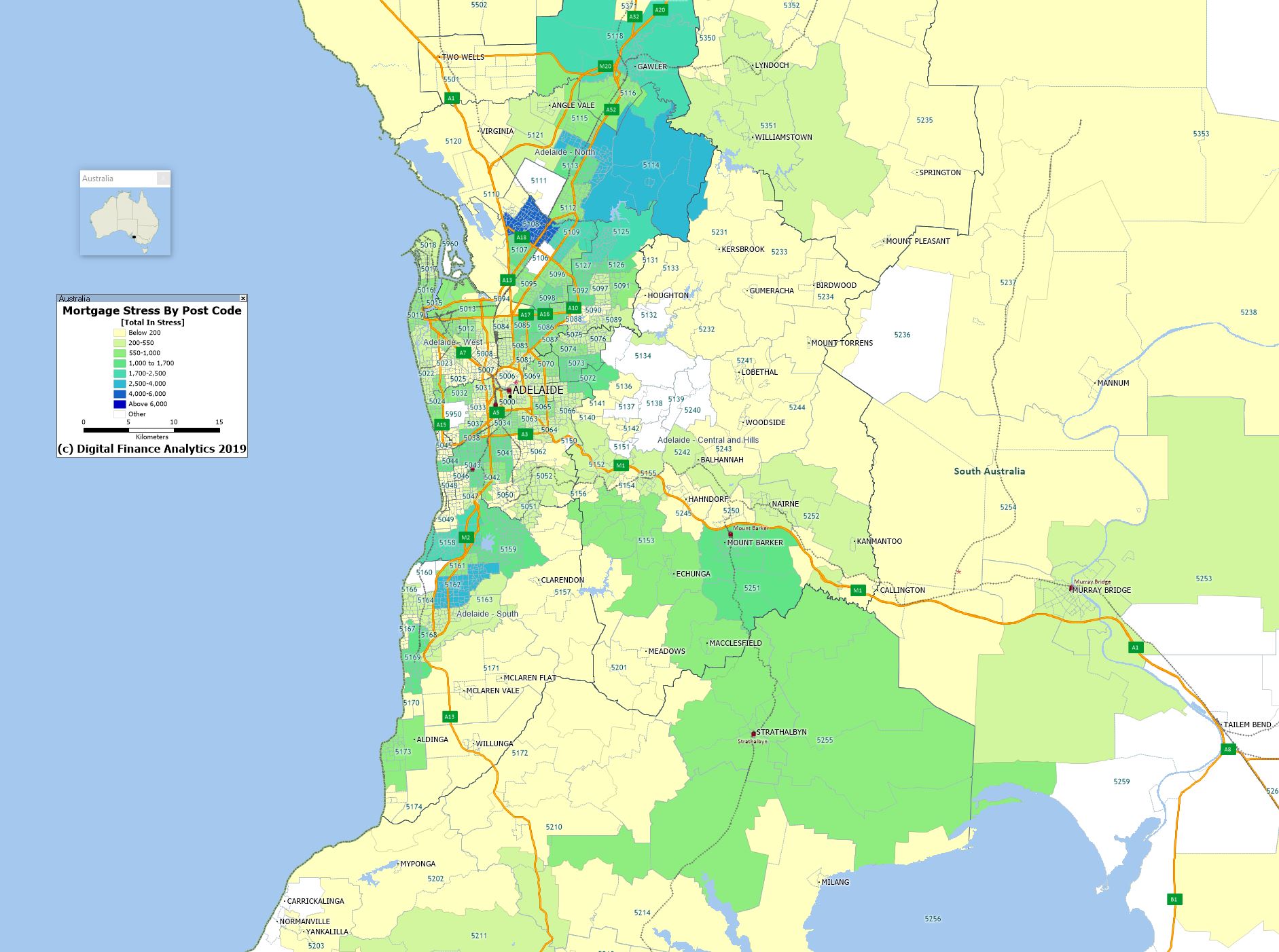

Adelaide:

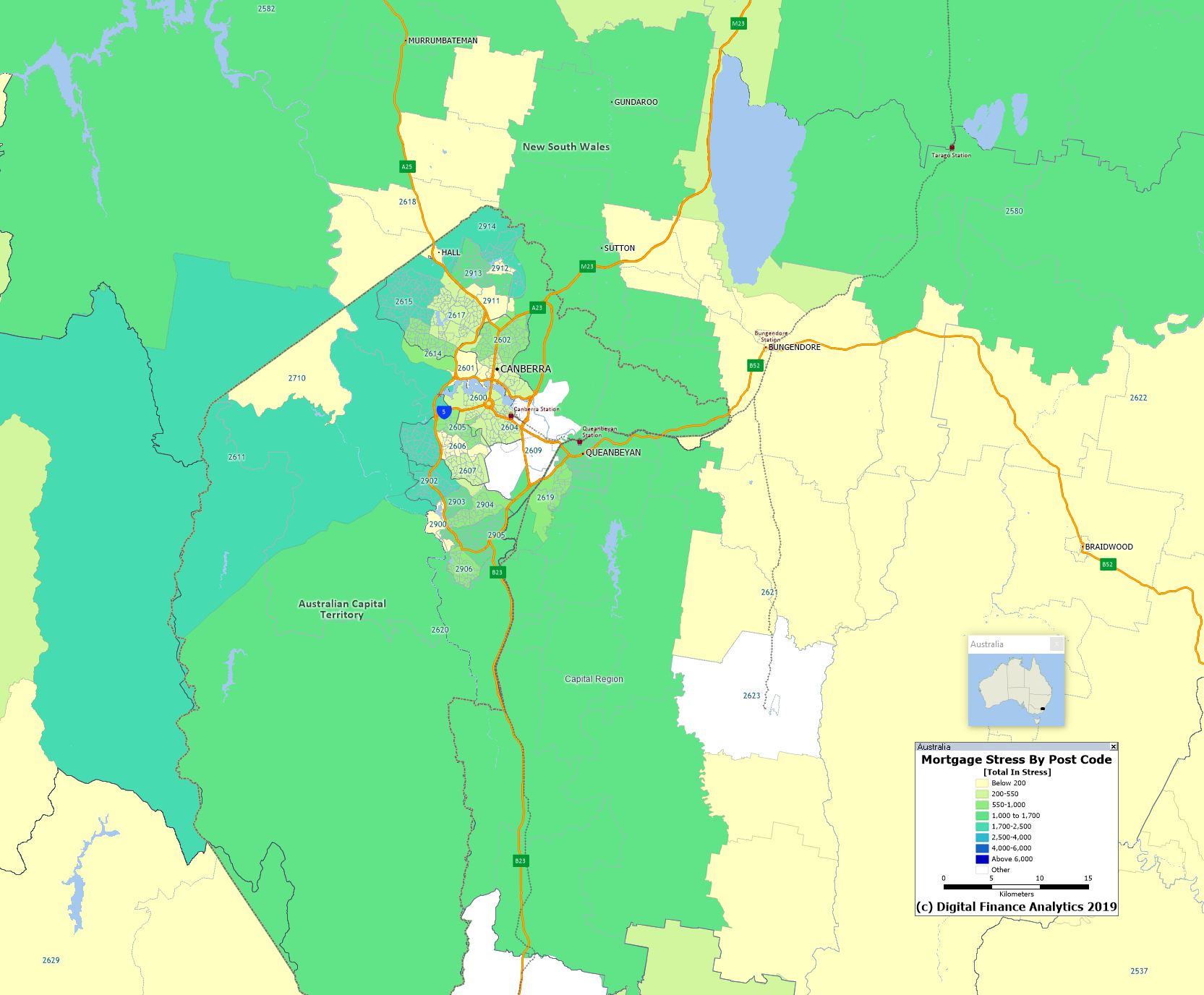

And Cambra:

Advertisement

Let the envy begin.

Via Martin North today come some cool mortgage stress maps. Sydney:

Melbourne:

Brisbane:

Perth:

Adelaide:

And Cambra:

Let the envy begin.