By Chris Becker

It was all about the USD overnight with the release of 4Q GDP figures and the latest CPI print from Europe, with the former sending Treasury yields higher and the latter jostling Euro around but giving European stocks a reprieve from impending recession fears sending them higher.

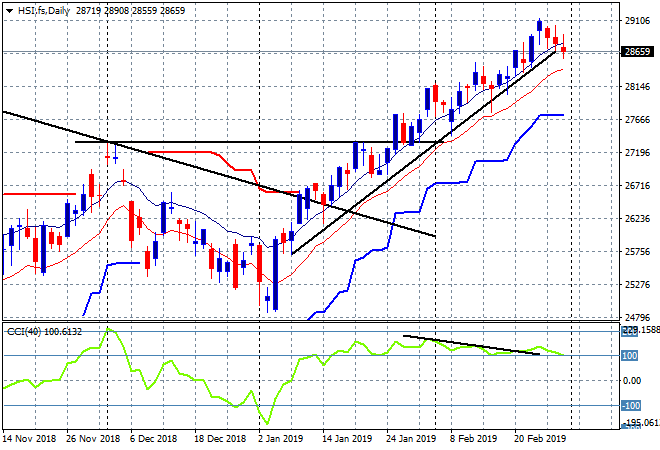

Looking first at the action on the Asian session yesterday, the Hong Kong Hang Seng Index closed down only 0.2% lower at 28700 points. Although the current rally remains intact price had gotten ahead of itself slightly so this reversion continues modestly. The interim target at 30,000 points remains intact but watch that trendline and momentum readings carefully for a correction:

Advertisement