Policy error is the name of the game at the Australian central bank. Witness:

- house prices in Australia’s two largest cities are in outright crashes;

- it is spreading steadily to other capitals;

- building approvals are crashing coast to coast;

- infrastructure investment has topped out;

- credit is swiftly falling towards zero;

- the NAB business survey has crashed signalling the same for investment ahead;

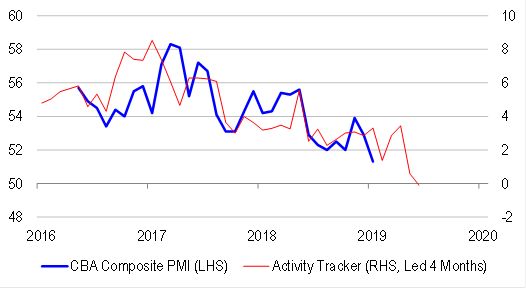

- PMIs are crashing, corroborating the NAB survey;

- car sales are marching lower;

- retail sales have stalled and posted an Xmas shocker;

- leading employment indexes have rolled over sharply;

- monthly core inflation is at 1.4 per cent and tumbling;

- bank share prices are down 40 per cent as they deliver unprecedented mortgage rate hikes into crashing house prices thanks to rising funding costs;

- trade inflows have tanked with domestic demand, and

- a federal election economic stall is imminent.

The above array of ugly data will threaten negative growth for Q4 2018, from Damien Boey at Credit Suisse:

It looks unlikely that consumption contributed anything to 4Q GDP. At the same time:

- Real net exports deteriorated, subtracting almost 0.3% from quarterly GDP growth.

- Residential investment likely fell.

- Capex at best experienced anaemic growth.

Therefore, but for inventory accumulation, it is quite possible that 4Q real GDP contracted, following modest growth in 3Q. Real GDP growth is likely to significantly undershoot the RBA’s optimistic forecasts.

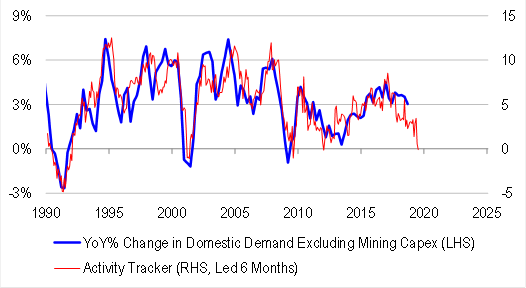

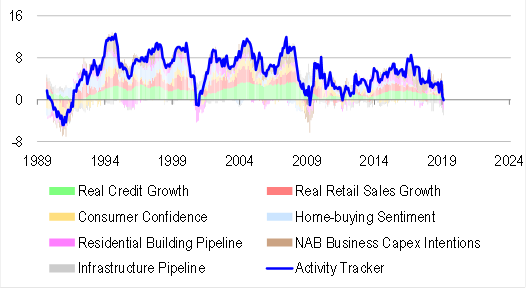

Our proprietary activity tracker reflects this logic. The tracker is a powerful contemporaneous, if not leading indicator of the cycle in core domestic demand (ie excluding lumpy mining capex). It is based on retail sales, credit, building approvals, the depth of the infrastructure capex pipeline, and various sentiment indicators. Updating it for the latest data, we find that the tracker has fallen to slightly negative levels, consistent with a sharp slowdown in domestic demand.

It’s odds-on that Q1 2019 will be more of the same. And Q2, 2019 carries guaranteed election weakness. This is more than an economic slowdown, it’s an economic stall and it’s going to drive an unemployment spike into a bursting housing bubble threatening a complete economic unwind. Not cutting now for some insurance is lunacy.

The RBA has not hiked rates at all in the cycle to deliver the above because it never produced a recovery of sufficient strength to do so. Now it is taking a crazy punt that it can prevent tumbling house prices from infecting wider activity using nothing more than the fictional forecasts of a vapid Futureboom! Talk about quixotic. Compare the above actual data with an RBA outlook that has become little more than a trailing six month moving average:

The central scenario is for the Australian economy to grow by around 3 per cent this year and by a little less in 2020 due to slower growth in exports of resources. The growth outlook is being supported by rising business investment and higher levels of spending on public infrastructure. As is the case globally, some downside risks have increased. GDP growth in the September quarter was weaker than expected. This was largely due to slow growth in household consumption and income, although the consumption data have been volatile and subject to revision over recent quarters. Growth in household income has been low over recent years, but is expected to pick up and support household spending. The main domestic uncertainty remains around the outlook for household spending and the effect of falling housing prices in some cities.

The housing markets in Sydney and Melbourne are going through a period of adjustment, after an earlier large run-up in prices. Conditions have weakened further in both markets and rent inflation remains low. Credit conditions for some borrowers are tighter than they have been. At the same time, the demand for credit by investors in the housing market has slowed noticeably as the dynamics of the housing market have changed. Growth in credit extended to owner-occupiers has eased to an annualised pace of 5½ per cent. Mortgage rates remain low and there is strong competition for borrowers of high credit quality.

The labour market remains strong, with the unemployment rate at 5 per cent. A further decline in the unemployment rate to 4¾ per cent is expected over the next couple of years. The vacancy rate is high and there are reports of skills shortages in some areas. The stronger labour market has led to some pick-up in wages growth, which is a welcome development. The improvement in the labour market should see some further lift in wages growth over time, although this is still expected to be a gradual process.

Inflation remains low and stable. Over 2018, CPI inflation was 1.8 per cent and in underlying terms inflation was 1¾ per cent. Underlying inflation is expected to pick up over the next couple of years, with the pick-up likely to be gradual and to take a little longer than earlier expected. The central scenario is for underlying inflation to be 2 per cent this year and 2¼ per cent in 2020. Headline inflation is expected to decline in the near term because of lower petrol prices.

This mad gambit (or pathological optimism?) is the perfect encore to the RBA’s “dumb bubble”, an equally toxic punt that blew a housing bubble from 2012-2016 to float the economy over a mining investment cliff that the bank never saw coming.

Now we have what looks an awful lot like a deleveraging singularity developing at the very heart of Australia’s thirty year credit boom just as we run out of monetary ammo.

This is not good monetary management. It is crazed lurching from one bubble and bust to the next, cheerfully ruining hard working people’s lives along the way, laying waste to the political economy and incinerating the last of its own brand. The Kouk summed it up perfectly:

The RBA ineptitude knows no bounds. An extraordinary statement today, devoid of insight, fact based analysis, awareness of recent data. The Board is made up of flunkies & galoots. The price of this is jobs, incomes and well-being.

— Stephen Koukoulas (@TheKouk) February 5, 2019

All work and no play makes the RBA a dull boy.