The warnings of slower services activity spreading from the housing bust continue to mount. We know that Westpac is stalled, BOQ is shrinking, McGrathmageddon and Domainmageddon roll on. But these are obvious, direct casualties. More interesting now are indirect multipliers. There’s SG Fleet for instance:

Fleet management provider SG Fleet has posted a 7 per cent drop in profits amid a slump in private new car sales.

Locally, it said the absense of wage growth and percieved negative wealth effect was delaying big ticket purchases, and evident in a decrease of 11.5 per cent for private new car sales over the period.

“We continue to see tough conditions in our Consumer business and we are working on dealing with the challenges faced,” chief Robbie Blau told the market.

Investor confidence in waste management group Bingo Industries has been shredded after the company cut its profit forecasts by up to 20 per cent just three months after re-assuring investors at its annual meeting that a downturn in construction wouldn’t hurt its outlook.

…Even investors who took up shares in the May, 2017 float at an issue price of $1.80 are now heavily underwater.

…The company warned that a much faster decline in the apartment construction market has cut volumes in its building and demolition collections business, while a decision to delay price rises to customers will also leave a hole in forecast profits.

Advertisement

And Coles, where convenience is falling away versus price, the AFR:

Coles’ net profit fell 29.4 per cent to $381 million in the six months ending December after Australia’s second largest food and liquor retailer booked $146 million in supply chain restructuring charges.

…Coles posted its 45th consecutive quarter of same-store food sales growth, but momentum slowed dramatically to 1.3 per cent in the December quarter from 5.1 per cent in the September quarter as the sugar hit from the Little Shop miniature plastic groceries promotion came to an end and the retailer stopped handing out free plastic bags.

The result was also marred by a 42.7 per cent fall in earnings from petrol and convenience retailing to $47 million, which more than offset a 3.7 per cent rise in profits from liquor to $84 million.

Seven West Media has continued to slash its debt pile and has increased its cost savings targets but has reduced its underlying earnings forecast for the full-year in the face of a softer than expected advertising market.

…The tough first half for the advertising market was particularly driven by a pull back in spending by banks as financial institutions weathered public backlash from the royal commission.

People putting off elective surgery was the surprising driver behind another earnings upgrade from NIB, its second in four months, as its health insurance members worry more about their financial health and spend less on discretionary medical procedures.

NIB announced the upgrade along with a strong half-year result on Monday. The company reported a rise in membership numbers, revenue and profit margins which generated an 18.6 per cent rise in underlying operating profit to $114.3 million compared to the previous first half.

The company, which announced a 10¢ interim dividend, said underlying operating profit for the full year was expected to be at least $195 million, with reported earnings expected to reach $178 million.

Advertisement

As we know, the critical turn for the economy ahead is whether the consumer swings to renewed saving, via Gerard Minack:

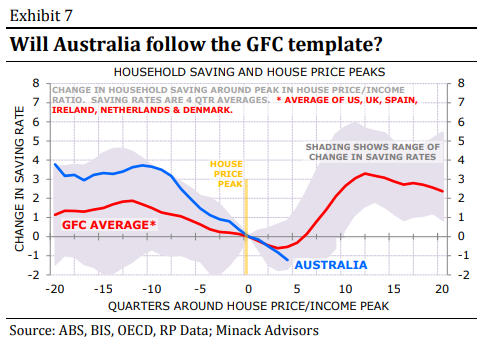

The evidence from other economies is that household saving rates typically keep falling for around a year after house prices peak relative to income. The adverse wealth effect – when household saving starts to rise – normally hits a year or two later.

Exhibit 7 shows the change in household saving rates around the house price/income peak for Australia and a selection of economies that saw significant house price declines in the GFC. On average, the household saving rate increased by 3½ percentage points over an 8 quarter period, starting one year after the peak in house prices.

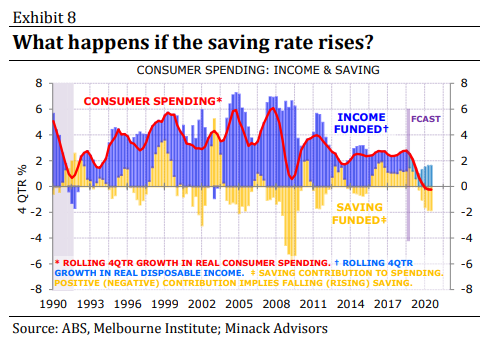

Australia is toast if it follows that pattern. Exhibit 8 shows what would happen to real consumer spending if the household saving rate rises by 3½ percentage points over the next two years. I have assumed that real household disposable income continues to rise by 1½%. Of course, that would be too optimistic: income growth would weaken if consumer spending – which accounts for over 55% of GDP – started to weaken as this scenario implies.

This illustrates the point that the wealth effect alone is capable of causing recession. The uncertainty is whether the wealth effect kicks in as powerfully as in this simple example. If the recent pattern of macro weakness – in house prices, building approvals and hiring intentions – continues, then I will make the bet that the wealth effect will cause a recession in Australia, most likely later this year.

The evidence is mounting that a turn towards saving is underway.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.