Again great stuff from Damien Boey at Credit Suisse who has a much better grasp of the economy than does the lunatic RBA:

By now, CPI, unemployment and RBA forecast downgrades are becoming old news … The Consensus view is that the RBA will moderately downgrade its forecasts, but not capitulate on its rate stance next Tuesday.

This view is probably right. Probably. But there is another possibility worth considering, that we wrote about recently. Please see our article “Positioning for RBA forecast downgrades” dated 30 January 2019

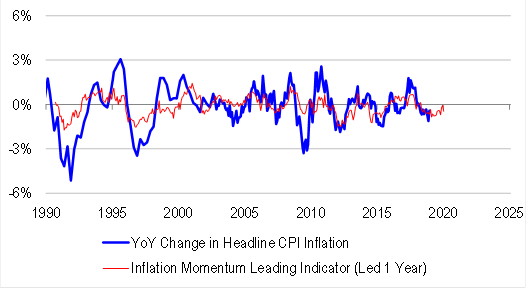

On the RBA’s narrow list of criteria for setting rates, the economy is evolving within its desired parameters. The unemployment rate is at a cyclical low of 5% (as forecast), and CPI inflation is around 1.75% (also as forecast). And we also know that in the “Lowe-era”, the Bank is more macro-prudentially minded than not. Therefore, it is willing to suffer growth and inflation undershoots for the sake of not cutting rates, and not inflaming the household debt situation. In the extreme, this means that even if GDP growth were to slow to 1-2%, and inflation follow suit, the Bank would not cut rates. But there might be a case for easing in the remote scenario where GDP growth turns negative.

We can see the merit in this argument. But what if GDP growth were slowing very sharply, to the point where it is unclear whether it will turn negative or not. And what if at the same time, the commercial banks were conducting out-of-cycle rate hikes? We think that in this scenario, a rate cut is not just a possibility, but a likelihood. Indeed, multiple rate cuts are likely in this scenario, because monetary transmission is impaired. So far, the money market is only pricing in a 50% chance of a 25bps rate cut this year. We think that it has not gone far enough.

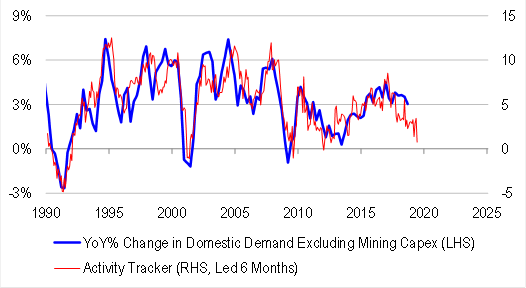

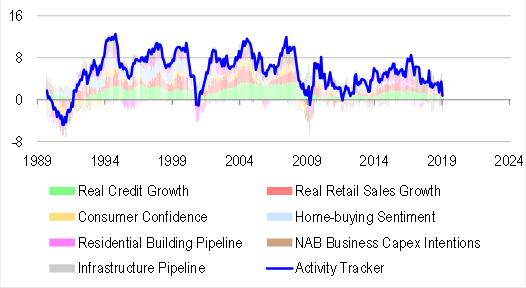

Looking at the data, there are reasons to be concerned, even for the hawks at the RBA. Real GDP only grew by 0.3% in 3Q. In 4Q, things look worse. Net exports could subtract 0.5-0.8% from GDP growth. Residential investment likely fell. Infrastructure spending probably plateaued at a high level. Consensus is looking for 0.7% real retail sales growth – but this assumes something very generous for December, when we already know from higher frequency data that spending was weak. For example, the NAB cashless retail index maps to an 0.3% contraction in nominal retail sales, while vehicle sales plummeted over the month. In lieu of all these data points, if 4Q can repeat 3Q’s performance on the back of inventory build and other miscellaneous spending, this will be a very good outcome! But even so, 2-quarter annualized growth will only be running at 1.2%, well short of the RBA’s forecasts.

Slower growth leads to slower inflation. And slower inflation leads to higher real borrowing costs, even before we factor in out-of-cycle rate hikes. So financial conditions are tight, and possibly tightening in the absence of intervention.

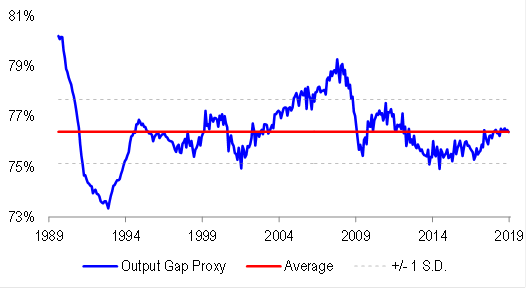

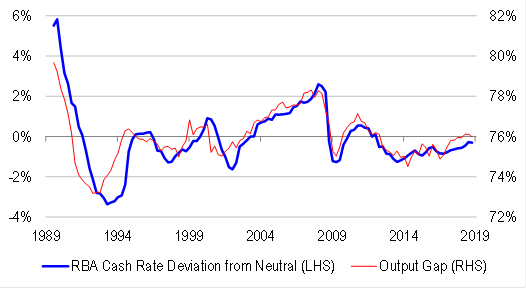

Updating our output gap, bond yield and cash rate models, we find that:

- The output gap is currently close to zero, consistent with …

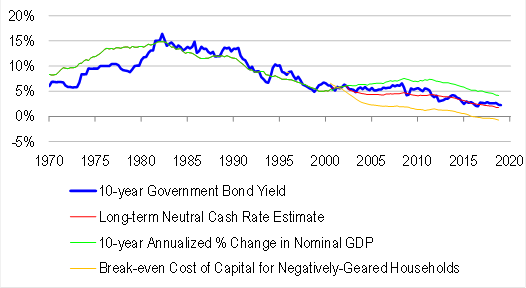

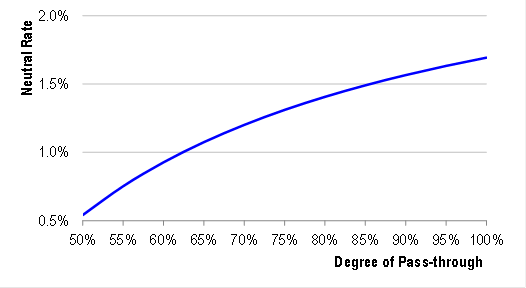

- The cash rate being set in line with the long-term neutral rate …

- Which is falling due to impaired monetary transmission, towards 1.1% from 1.7%.

Also, if our activity tracker and now-casts are anything to go by, the output gap will not stay at zero. It will likely widen, adding to the cyclical downside to rates.

We think the RBA is well aware of the risks. The Board’s Harper valiantly attempted to defend the status quo a few days ago, but the bond market gave his comments little credit. At some point, the money market will compel the RBA to cut. Probably not yet. But the pricing is becoming too dovish to ignore. And we expect the dovishness to continue, as Australian yields fall relative to US yields, which themselves are now falling on a more dovish Fed.

Some Bank officials might think that the credible thing to do is stick with the script. But we think there is more credibility value in changing the script now.