DXY was soft last night and looks like it’s in for more for a while. CNY and EUR were firm:

The Australian dollar was firm:

But not so firm as EMs:

Advertisement

Gold is consolidating. There’s a good chance it’s going to push higher short term as DXY weakens:

Oil was firm:

Advertisement

Base metals were mixed:

Big miners strong:

EM stocks are up but hardly partying:

Advertisement

Unlike high yield which is leading the risk rally:

Treasuries were bashed:

And bunds:

Advertisement

As stocks marched higher:

Westpac has the wrap:

Economic Wrap

The US services sector cooled in December, the ISM non-manufacturing index fell a larger than expected 3.1pts to 57.6; a five-month low though still consistent with decent momentum in the services sector. The underlying detail showed more resilience, new orders and new export orders both firmed, while employment eased a touch.

German Nov. factory orders missed expectations and fell -1.0%m/m, -4.3%y/y (est. -0.1%m/m. -2.7%y/y). There was a notably deep slide (-11.6%m/m) in foreign orders within the Eurozone which highlights the downside risks for the region into 2019.

EZ Nov. Retail sales rose a firm +0.6%m/m, +1.1%y/y (est. +0.2%m/m, +0.4%y/y) lifted by German Nov. retail sales rising +1.4%m/m, +1.4%y/y (est. +0.4%m/m, -0.4%y/y) however the sales data has been volatile of late and may have been distorted by pre-December discounting.

The return of UK Parliament has livened debate around the forthcoming “meaningful vote” that was postponed in early December. Markets anticipate a vote on 15th Jan. but the timing of next week’s vote will be confirmed at a Cabinet meeting on Wednesday, after May attempts to garner some form of support on the Continent and within UK. Risks of another delay remain given the lack of support for May’s current Brexit plan

Event Risk

Australia’s trade balance for Nov is expected to decline slightly from $2.3bn to $2.2bn (Westpac estimate $2.1bn). Lower export prices for energy and lower coal volumes were contributing factors.

US NFIB small business optimism is expected to remain positive on current conditions as well as the outlook. JOLTS job openings data will update the hiring and quit rates, which are watched by the Fed.

So, the usual action if you believe that the Fed is going to ease and EMs stimulate; the US dollar falls, EM assets and commodities lift. FTAlphaville captures the moment:

Advertisement

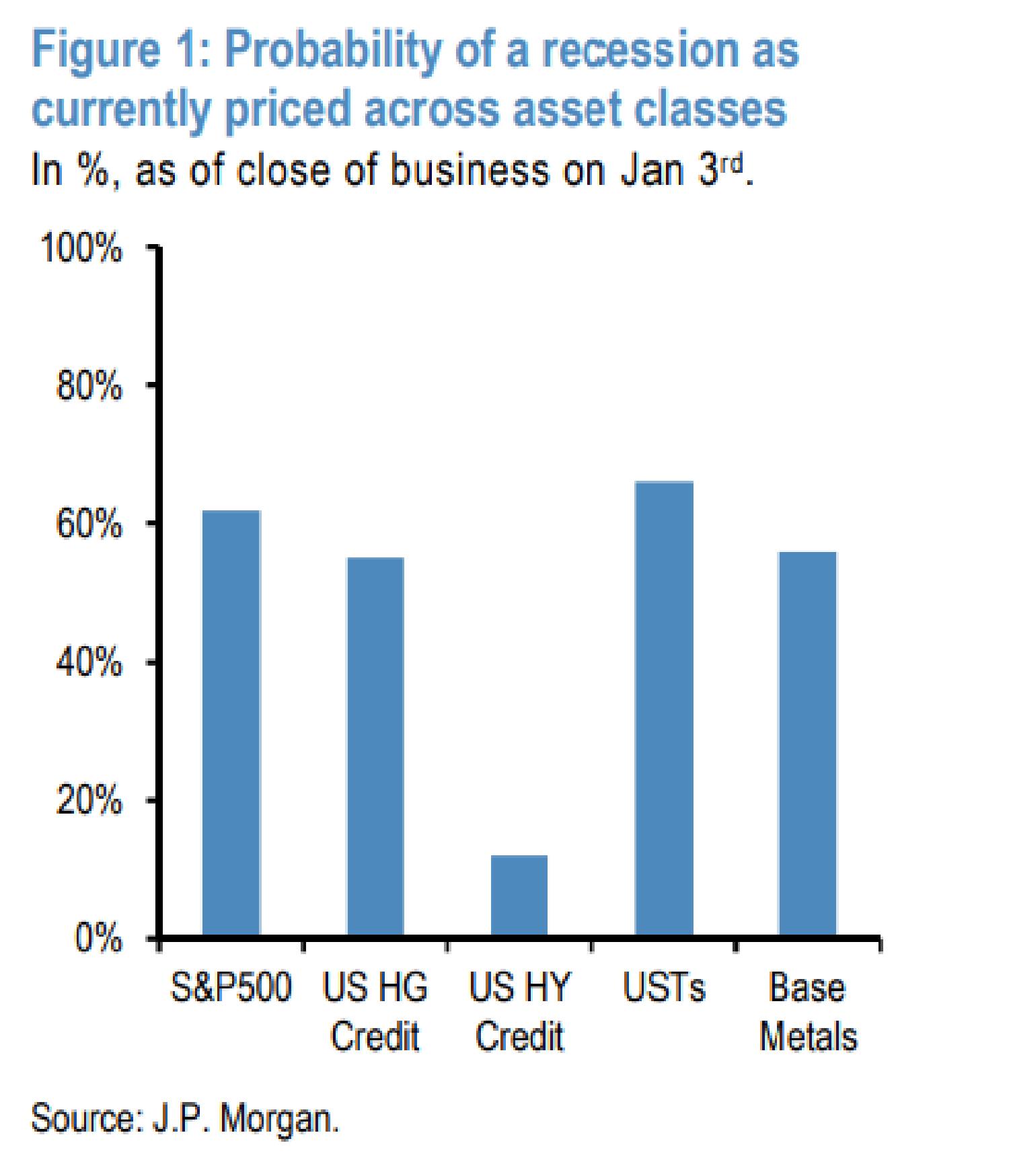

According to Nikolaos Panigirtzoglou at J.P. Morgan Securities, US equity markets are currently pricing in a 60 per cent chance of a US recession within one year. High-grade credit points to similar odds, as does US Treasuries and base metals. Investors in the one outlier, US high-yield credit, seem more sanguine. The asset class is pricing in a 12 per cent chance:

In order to determine these probabilities, Panigirtzoglou and his team looked at the historical behaviour of different asset classes in the lead-up to US recessions in the past. What they find is that over the past 11 recessions, the S&P 500 declined an average 26 per cent. With the S&P 500 down some 16 per cent since its peak, there’s that approximate 60 per cent chance within the year. (Because 16 is roughly 60 per cent of 26. So of course, this is rather rough measure; indeed not all economic downturns are preceded by stock market sell-offs at all.)

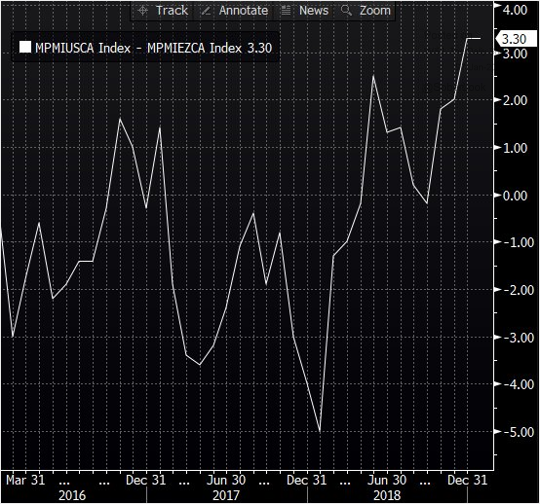

With everybody worried about a US recession the short term shift is out of DXY. The US is clearly going to slow but I’m not worried about recession. I can’t say the same for Europe. Check out the relative position of the composite PMIs between the two:

Advertisement

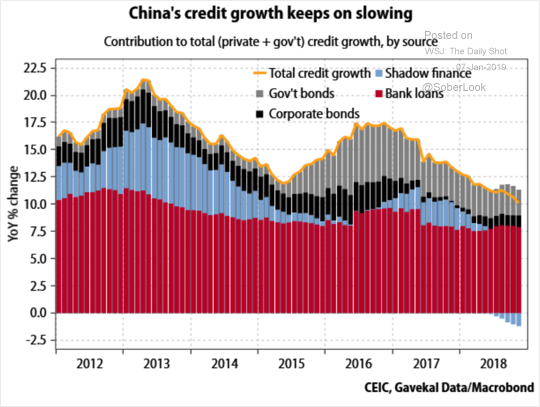

Sure the US is going to pullback but Europe might just keep falling as its export-led growth tracks a stalling China and EMs (plus is hit by Brexit). China’s most important leading indicator is not at all positive:

Note that in the past two stimulus episodes, Chinese growth did not turn around until credit had been rising for about nine months. It is still falling today.

Advertisement

Rebounding out of the Fed’s communication errors and stuck in Trump derangement syndrome, markets are today repricing for the wrong recession. It’s not coming in the US, unless it is dragged down by Europe and China first. 2019 will be another year of US out-performance amid everybody else doing worse. This has only been re-confirmed by a pausing Fed.

Likewise for today’s rebounding Australian dollar. It’s in a counter-trend rally not a change in direction. That’s the final irony here. It should be pricing the risk of an Australian recession much higher than that of a US one.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.