Via the Kouk today, given he and MB are the only ones to have gotten this right:

In the wake of the September quarter national accounts, and with accumulating information on house prices, dwelling investment, the global economy and spare capacity in the labour market, I have revised my outlook for official interest rates.

For some time, I have been expecting the RBA to cut the official cash rate to 1.0 per cent, a forecast that has been wrong (clearly) given its decision to leave rates steady right through 2018.

That said, it has been a highly profitable call with the market pricing interest rate hikes when the call was made which has yielded a decent return as time has passed.

My updated profile for RBA rates is:

May 2019 – 25bp cut to 1.25%

August 2019 – 25bp cut to 1.00%

November 2019 – 25bp cut to 0.75%The risk is for rates to 0.5% in very late 2019 or in 2020

It will be driven by:

- Underlying inflation remaining below 2%

- GDP growth around 0.25 to 0.5% per quarter in 2019

- Annual wages growth stuck at 2.5% or less

- Global growth slowing towards 3%

- Labour market under-utilisation around 13 to 13.5%

There are likely to be other influences, but these are the main ones.

AUD, as a result, looks set to drop to 0.6000 – 0.6500 range.

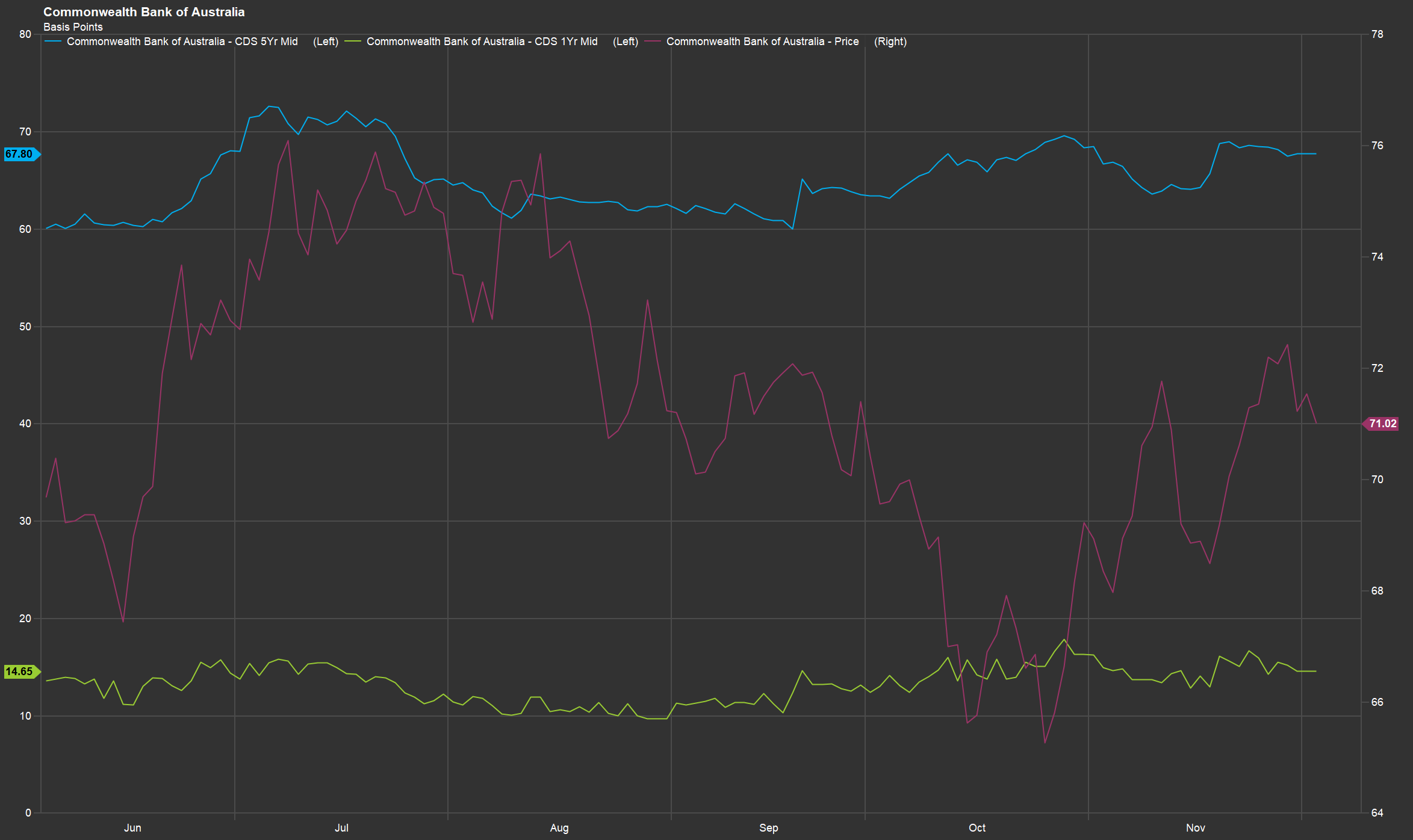

Can’t argue with that. Question is, what will it achieve? Banks will keep half to themselves as funding costs keep rising in short term:

And long:

Two mortgage rate cuts left to prevent the crash.

Good luck with that.