The AUD is still struggling through the day:

XJO is down a touch:

Bonds are well bid at the long end:

Dalian is firm:

Advertisement

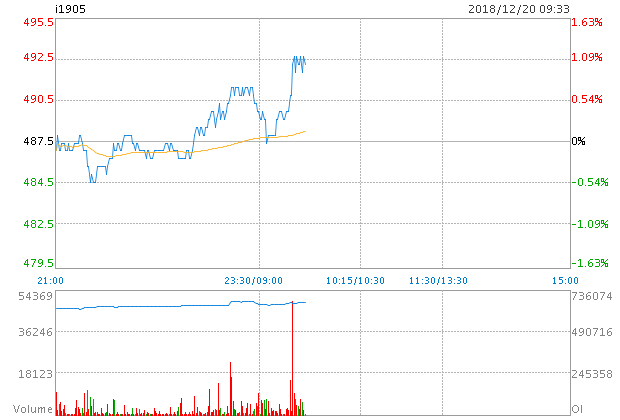

And Big Iron:

Big Gas is weak:

With Big Gold:

Advertisement

Big Banks are still under pressure other than the magical CBA which apparently lends elsehwere:

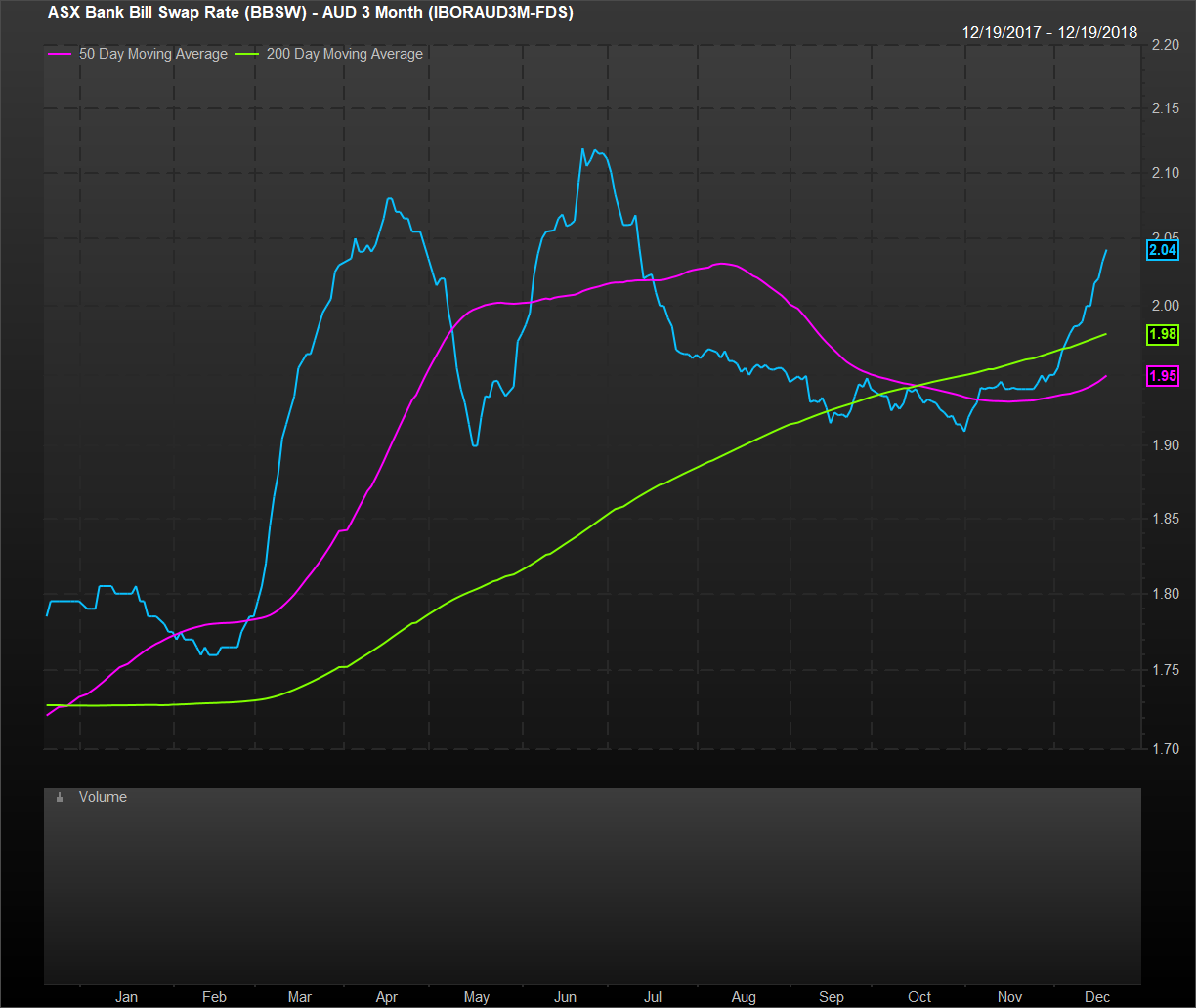

The RBA may not want to hike but mortgagees had better prepare for some more out-of-cycle mortgage rate hikes in the year. BBSW is marching higher:

Advertisement

Big Realty is weak:

The ASX has held up relative to global stocks recently thanks to miners. Whether it can continue is another question…

Advertisement