The AUD is still under pressure this morning:

Bonds are consolidating after the big breakout:

XJO opened with a bang but his been sold to two year lows ever since:

Advertisement

Big Iron continues to outperform:

Big Gas is aflame:

Big Gold wants some Fed sweet talking:

Advertisement

Big Banks are still free falling except a teflon coated CBA:

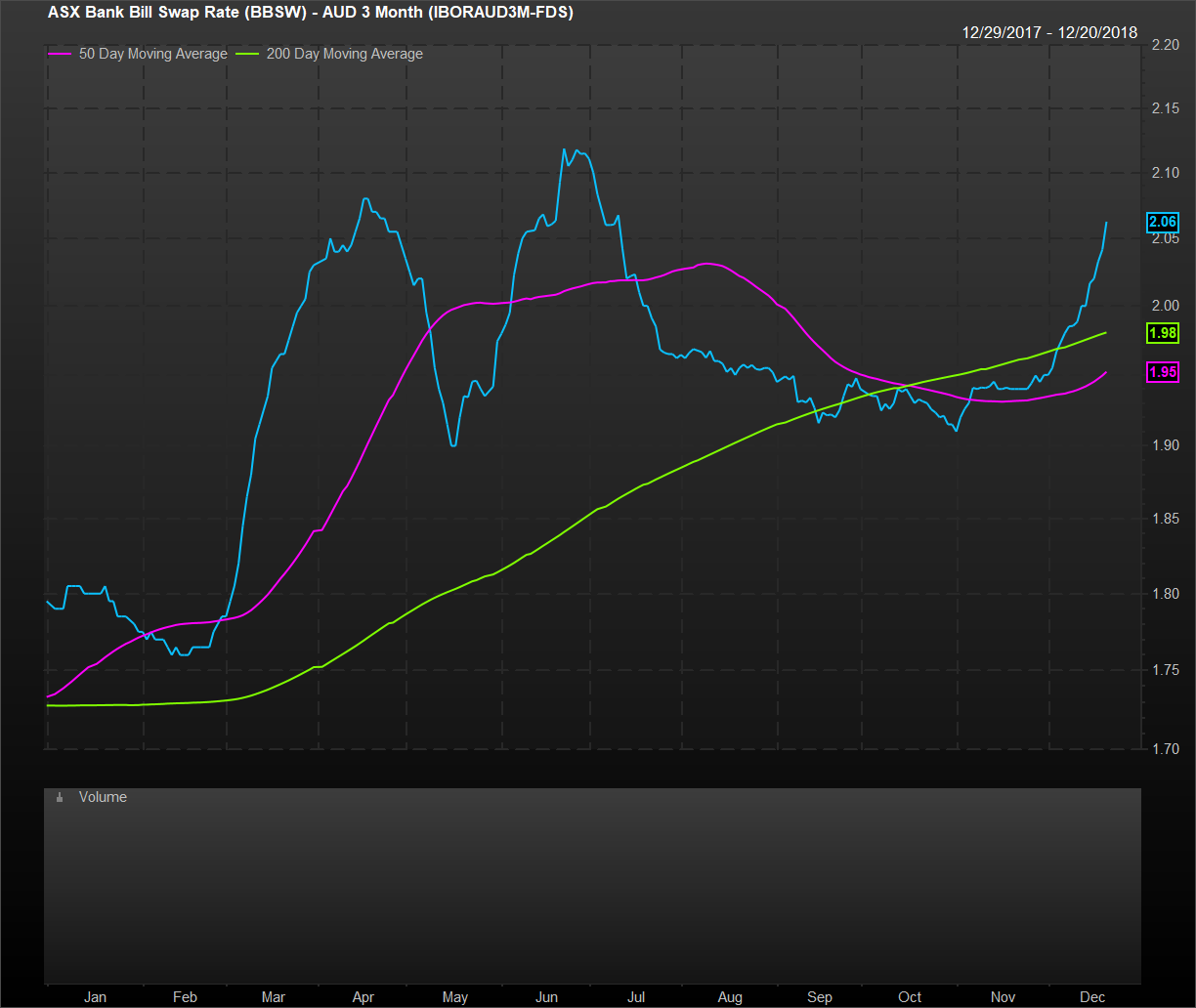

Funding costs are still targeting the moon:

Advertisement

Big Realty is breaking down all over:

Iron ore giveth and the housing bust taketh away.

Avagoodweekend.