New research from Roy Morgan shows that the number of Australians who intend to retire in the next 12 months is estimated at 426,000, a 30% increase on the level seen in 2008 when it was 328,000. Meanwhile, the average gross wealth (total assets excluding owner-occupied homes) of intending retirees is $331,000, up from $237,000 since 2008. However, the property and share market slump is likely to delay retirement plans:

Negative factors like the decline in the current share market and house prices currently impacting household wealth, combined with uncertainty around the future of franking credit refunds and negative gearing, have the potential to delay retirement decisions in order for potential retirees to build up sufficient wealth…

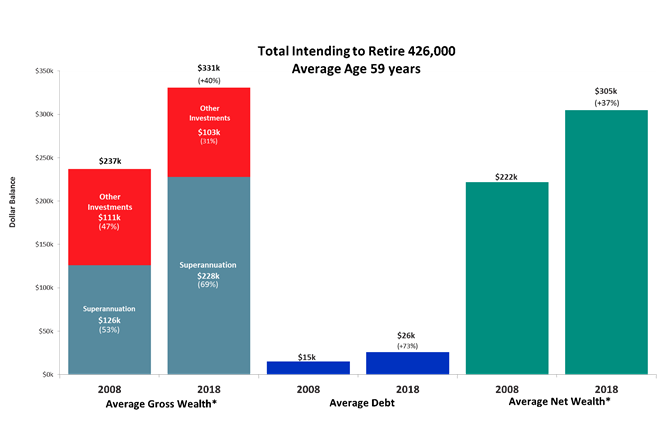

Currently the average gross wealth (total assets excluding owner-occupied homes) of intending retirees is $331k, up from $237k or 40% since 2008…

Superannuation, through its tax concessions and compulsory nature, has been the main vehicle for trying to achieve this and is having some success but is still falling well short of funding the retirement of those currently intending to retire. In the near term this shortfall is likely to continue as stock markets are facing considerable downward pressure and as a result will reduce the growth of superannuation funds.

Up to now, superannuation has been playing an increasing role in retirement funding and currently represents 69% of the gross wealth of intending retirees, up from 53% in 2008.

Although the average debt level for this group is currently only $26k, it does reduce their average net wealth to $305k, which is generally inadequate for self-funded retirement.

The overall conclusion from this is that intending retirees will be relying on government benefits for some time yet, given the fact that the Association of Superannuation Funds of Australia (ASFA) estimates that an individual would need $545k and a couple $640k for a ‘comfortable lifestyle’.

Given the very low interest rate at the moment and the level of economic uncertainty, the amount required to fund retirement is likely to rise well above these levels. This is not only likely to negatively impact the proportion that become ‘self-funded’ retirees but has the potential to delay retirement decisions…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.